Australia leads the world on rooftop solar, now it needs to catch up with how to manage it

August 9, 2025

It is an irony of no small significance that Australia, while leading the world in per capita uptake of rooftop solar, finds itself in 2025 well behind the pace on how best to manage this huge and valuable resource as part of a modern, increasingly renewables-powered grid.

As a major new report from Energy Catalyst and CSIRO this week reminds us, Australian homes and businesses are expected to have installed around 55 gigawatts (GW) of rooftop solar by 2035, generating roughly 70 terawatt-hours (TWh) of power.

In this context, the nation’s main grid, the NEM, is expected to regularly experience time windows where most of its power is flowing “upstream” from the distribution system, while minimum operational demand continues towards zero in several regions.

By 2050, operations on the NEM — once a one-way street from power generation plants to consumers via transmission lines and distribution networks — will be predominantly bidirectional, with about 115 GW of capacity and 100 TWh of generation provided by distributed PV.

By this stage, the report tells us, the script is flipped, with centralised energy resources taking on the role of providing back-up and balancing services to a vast network of distribution-connected energy resources – rooftop solar, home batteries, electric vehicles, hot water systems.

But to get to this point from where we are at now, in mid-2025, requires some thinking outside the grid.

To this end, Energy Catalyst and the CSIRO have collaborated with AEMO and industry and global experts on a reference set of five integrated reports to help identify where we need to be by 2035 if we want to achieve our 2050 climate and renewable energy commitments.

It follows an earlier report prepared for the federal government, which we reported on last month. See: Who is going to control and manage household solar, batteries and EVs? It needs a rethink of the power system.

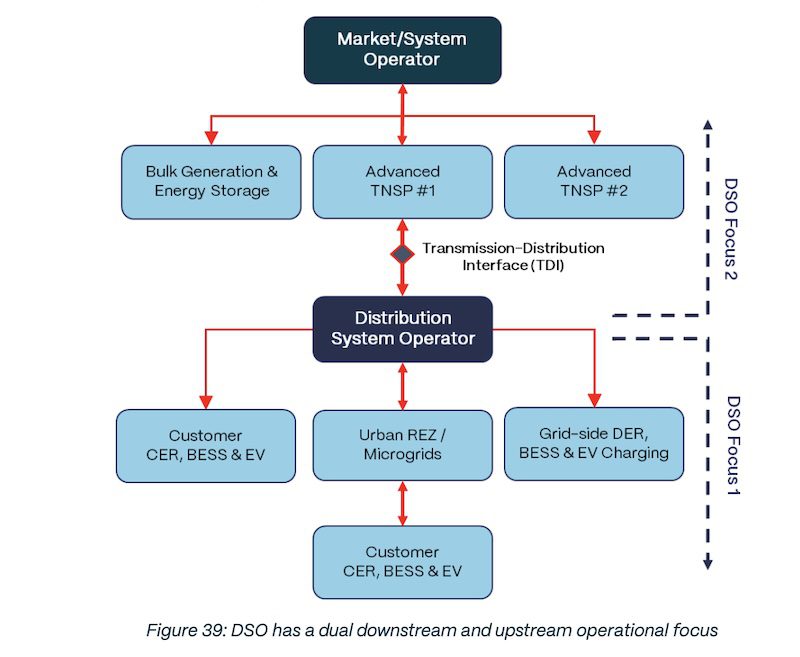

Report number 4 takes a deep dive into the concept of the Distribution System Operator: a new key player in the modern electricity market hierarchy sitting somewhere between AEMO and the distribution network.

It will be tasked with facilitating “the mutually beneficial participation of millions of distributed resources as an integral part of the future grid".

Energy Catalyst and CSIRO are not re-inventing the wheel. DSOs already exist and are being implemented with some success in electricity markets in the UK. Rather, the report makes a detailed study of global precedents and attempts to tailor them to the peculiarities of the NEM.

According to the report, while varying terminology is used across different jurisdictions, there is a “general convergence” on five functional responsibilities that a DSO would have in a high-consumer energy resources (CER), or distributed energy resources, context.

The first is Active System Management, or to manage the safe, reliable and efficient operation of a two-way power flow to ensure the continuous supply of electricity to, between and from customers.

The second role would be to use a “spectrum” of market mechanisms to value, incentivise, procure and operationally co-ordinate energy, flexibility and other system services from CER/DER and flexible loads. Examples range from tariffs, to contracts, to market signals.

Thirdly, a DSO would have to perform long-term distribution system planning, the report says, working in collaboration with the relevant distribution and transmission network companies, as well as with AEMO, as an integral part of whole-system planning.

A fourth task is to enable enhanced network visibility, real-time monitoring and rapid response to dynamic conditions, including fault prediction and network performance optimisation. This would include facilitating better understanding of customer behaviour and usage patterns and to engage customers in mutually beneficial initiatives.

Finally, a DSO would be need to actively collaborate with AEMO and relevant TNSPs to enable operational visibility, support relevant data exchanges, align operational and market interactions, and coordinate longer-term system planning.

Of course, the 245-page report goes into much more deeply technical detail on all of these things a DSO might be expected to do, with plenty of real-life references and case studies to back it all up.

On the why, however, the report is more succinct.

“Australia’s power systems are undergoing an unprecedented structural transformation, driven by accelerating decarbonisation and the explosive growth of CER/DER,” it says.

“The recommendations derived from this analysis underscore the need to rethink key aspects of the 21st century power system as a foundation for developing future-facing capabilities like DSO … models.

“Doing so is neither academic nor abstract: achieving secure, affordable and sustainable electricity for the longer-term will depend on it.”

Republished from Renew Economy, 7 August 2025

The views expressed in this article may or may not reflect those of Pearls and Irritations.