Can we rely on Treasury’s latest net migration forecasts?

January 23, 2026

Treasury’s Net Overseas Migration forecasts don’t match current visa settings and trends. Migration may fall less than predicted – and stay higher for longer.

In December 2025, Treasury decided to hold its pre-election Net Overseas Migration (NOM) forecast unchanged at 260,000 in 2025-26; 225,000 in 2026-27 and 235,000 long-term. It has also provided some more details on these forecasts in its December 2025 Population Statement. But can we rely on these forecasts or was Treasury under pressure to leave these effectively unchanged?

NOM in 2024-25 fell to 305,600 after peaking at 538,340 in 2022-23 and 429,160 in 2023-24. It fell well below levels being suggested by various parts of right-wing media and think tanks, but was above the initial Treasury Budget forecast for 2024-25 of 260,000. There is zero chance it will rebound to the levels right wing media and think tanks insist on suggesting (i.e. up to 550,000 in 2025). But will it now bottom-out at around current levels or will it fall significantly further as Treasury is forecasting, particularly for the long-term?

Treasury says in its December 2025 statement that:

“NOM is forecast to decline further in 2025–26 and 2026–27, driven by fewer migrant arrivals and an increase in migrant departures. However, departures are expected to be lower than in the 2024 Statement as migrants on temporary visas are departing at lower rates than experienced in the past”.

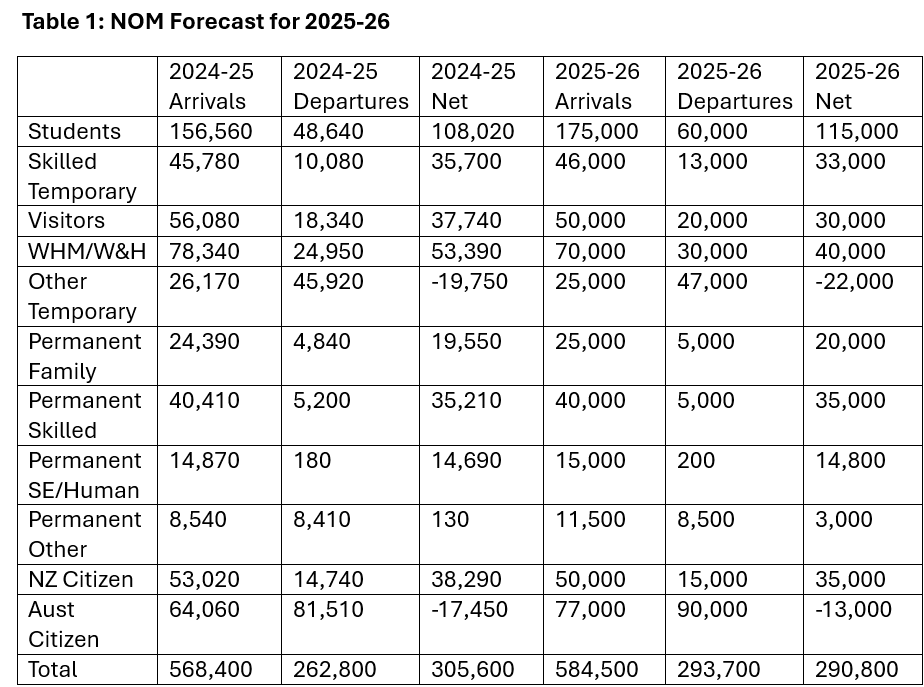

That effectively means Treasury is forecasting NOM arrivals to also be lower than it forecast in its 2024 population statement. Compared to NOM in 2024-25, Treasury is now expecting NOM arrivals to fall in 2025-26 by 10,000 and then fall again in 2026-27 by another 5,000; and NOM departures to increase by 45,000 in 2025-26 and by another 25,000 in 2026-27.

Treasury’s forecast decline in NOM arrivals in 2025-26 and again in 2026-27 would need to take place against the background of three new measures that will add to NOM arrivals.

First, the Government has announced a 25,000 increase in the student planning level for 2026 compared to 2025. As the planning level relates only to students doing higher education or VET courses, a large portion of the 25,000 will likely add to NOM student arrivals (including students who have already arrived, initially to do a shorter course).

Moreover, the 25,000 does not include dependents many of whom will also be counted in NOM student arrivals. Dependents usually add another 15 per cent to primary student applicants (or around an additional 3,750).

Possibly triggered by the higher planning level, offshore student applications in the first five months of 2025-26 were around 5,000 higher than in the same five months of 2024-25. The decline in offshore student applications Treasury has been relying on appears to have ceased. While offshore student grants were lower in the first five months of 2025-26, providers will do all they can to meet the higher allocations they have been given and will press the Government on timely visa processing. The industry will also press the Government to again increase the planning level in 2027.

Second, arrivals under the new Pacific Engagement and Tuvalu Visas will start in 2025-26. These are permanent resident visas that for no logical reason are not counted in the formal permanent migration program. These visas operate on a lottery basis and are heavily over-subscribed so it is likely the full yearly allocation of 3,280 places will be delivered and the majority will start arriving from 2025-26.

Third, arrivals under the new two year stay MATES visa for young Indian professionals will also start in 2025-26. These provide for 3,000 places for primary applicants plus dependents. Given the professional record required for this visa, most of the primary applicants will be older than students. They are more likely to have a spouse and possibly children. It is quite likely around 5,000 people overall will arrive annually under this new visa. They also have the option to apply to extend their stay on another type of visa.

Skilled temporary visa grants set a new all-time record for the September quarter in 2025-26 at 35,895. That trend is likely to continue for the rest of the financial year given the job vacancy index remains at elevated levels. Onshore applications for this visa continue to increase very strongly.

While it is likely there will be a further decline in NOM arrivals under the visitor category due to earlier policy changes, and some easing in working holiday maker arrivals given the extraordinary level in 2024-25, this is unlikely to make up for the additional arrivals under the above three new measures as well as the strong skilled temporary visa grants.

Overall, temporary and permanent NOM arrivals in 2025-26 are likely to be higher than in 2024-25 rather than lower as Treasury is forecasting.

NOM departures will likely rise again in 2025-26 due to the large volume of temporary entrants in Australia whose visas will be expiring. But as Treasury points out, temporary entrants are making every effort to extend their stay such that there is now a record number of onshore applicants on bridging visas (over 400,000).

As always, student visa policy will be the key.

There are around 100,000 students on bridging visas waiting on a decision on their onshore application. Over 45,000 students have appealed refusal of an onshore student application. In the first five months of 2025-26, an astonishing 63,987 students applied for temporary graduate visas compared to 31,541 in the first five months of 2024-25. That was after 94,499 students secured temporary graduate visas in 2024-25; a level that is likely to be exceeded in 2025-26 as there will be another surge in temporary graduate applications in the first quarter of 2026.

In 2024-25, over 12,000 students directly secured permanent visas and another 13,000 secured temporary skilled and working holiday visas. While student NOM departures are likely to increase in 2025-26, these trends suggest they will not increase significantly.

In 2024-25, 30,782 temporary graduate visa holders directly secured permanent residence. Another 15,479 temporary graduate visa holders secured employer sponsored skilled temporary visas in 2024-25. That was a major increase on the 3,000 to 4,000 temporary graduates who had previously been securing these in recent years.

That re-confirms the intention of temporary graduates to try and extend stay. Departures of temporary graduates may increase in 2025-26 but only to a limited degree.

It is also likely departures of NOM visitors, skilled temporary entrants and working holiday-makers will rise again in 2025-26 simply because of the volume of such visa holders currently in Australia whose visas will expire in 2025-26 as well as the tightening of policy on visitors. But the strength of the labour market will again limit the increase as these visa holders will continue to look for ways to extend stay and Australian employers will continue to offer them job opportunities that encourages that.

Treasury is right to forecast the NOM contribution of NZ citizens will remain strong in 2025-26 at around 35,000. This is the function of Australia’s relatively stronger labour market as well as a key policy change to provide NZ citizens with a direct pathway to Australian citizenship without first securing a permanent resident visa (the change effectively increased the size of permanent migration).

Treasury is also likely to be right about the NOM contribution of Australian citizens falling to a slightly smaller negative (i.e. not as many Australian citizens leaving and more returning compared to 2024-25 given global uncertainties and Australia’s strong labour market).

On my calculations, that gives a NOM outcome in 2025-26 (see Table 1) of around 290,000 (plus or minus 10,000). That would represent a decline of around 15,000 on the outcome for 2024-25 due to a 16,000 increase in NOM arrivals and a 31,000 increase in NOM departures. But the overall NOM outcome in 2025-26 may be around 30,000 higher than Treasury’s forecast of 260,000. We will have a better idea of this once the data on students for December 2025 and January 2026 and skilled temporary entrants and working holiday-makers for the December quarter is published.

But what about the long-term which is far more important?

Treasury continues to argue that NOM will return to the pre-Covid average of around 225,000 to 235,000. That would appear to assume that policy settings will overall be much the same as pre-Covid. There is little evidence to support that assumption unless Treasury thinks future governments will significantly tighten policy (but hasn’t said so).

Compared to the situation pre-Covid, current policy is:

- tighter for VET and ELICOS sector students but more expansionary for the much larger higher education sector;

- significantly more expansive for skilled temporary entrants and working holiday-makers although processing times have blown out;

- slightly tighter for temporary graduates but not enough to prevent a massive increase in the stock of these visa holders;

- significantly tighter for visitors seeking to extend stay;

- much more expansive for permanent residents (especially after removing NZ citizens from having to secure a permanent residence visa) but not so expansive as to prevent development of a rapidly growing backlog of permanent resident applications that will at some stage have to be addressed (as will the huge bridging visa backlog); and

- significantly more expansive for NZ citizens.

Overall, current policy settings are materially more expansionary than prior to Covid, suggesting Treasury’s long-term NOM forecast of 225,000 to 235,000 is too low, possibly by as much as 50,000 in a normal labour market. Treasury would do well to ensure ministers are aware of this, particularly before the government issues its next Inter-Generational Report for 2026.