AI, productivity and the long stall in living standards

February 20, 2026

Artificial intelligence may offer the best chance to lift stagnant productivity and living standards – but without deliberate policy choices, its benefits will be uneven and limited.

As we are constantly reminded, the number one political issue in Australia today is the cost of living as people struggle to meet their expectations for their living standards.

In fact, it is not so much that living standards are falling, but just that they are no longer rising, as we had come to expect over the 60 years or so following the Second World War. And the reason, of course, is that ever since the Global Financial Crisis around 2008, productivity growth has slowed to a crawl.

So the critical question is what is going to happen to productivity, and what can the government do to accelerate productivity growth. The Government has said that its focus in the next budget will be on productivity, and it has received many suggestions about how to increase productivity, including at its Economic Reform Roundtable some six months ago.

As I have written previously many of these suggestions have merit, but it is doubtful that they will make much difference to the rate of productivity growth. Even in the heyday of microeconomic reform in late 1980s and 1990s, the productivity gains from those reforms were almost entirely one-off gains, and they never added up to anything like the present shortfall in the continuing rate of productivity growth.

Instead, through history it is the impact of major new technological breakthroughs that has been overwhelmingly responsible for productivity growth. Indeed, if government policies could make much difference to the rate of productivity growth then we would expect to see more difference between the experience of different countries.

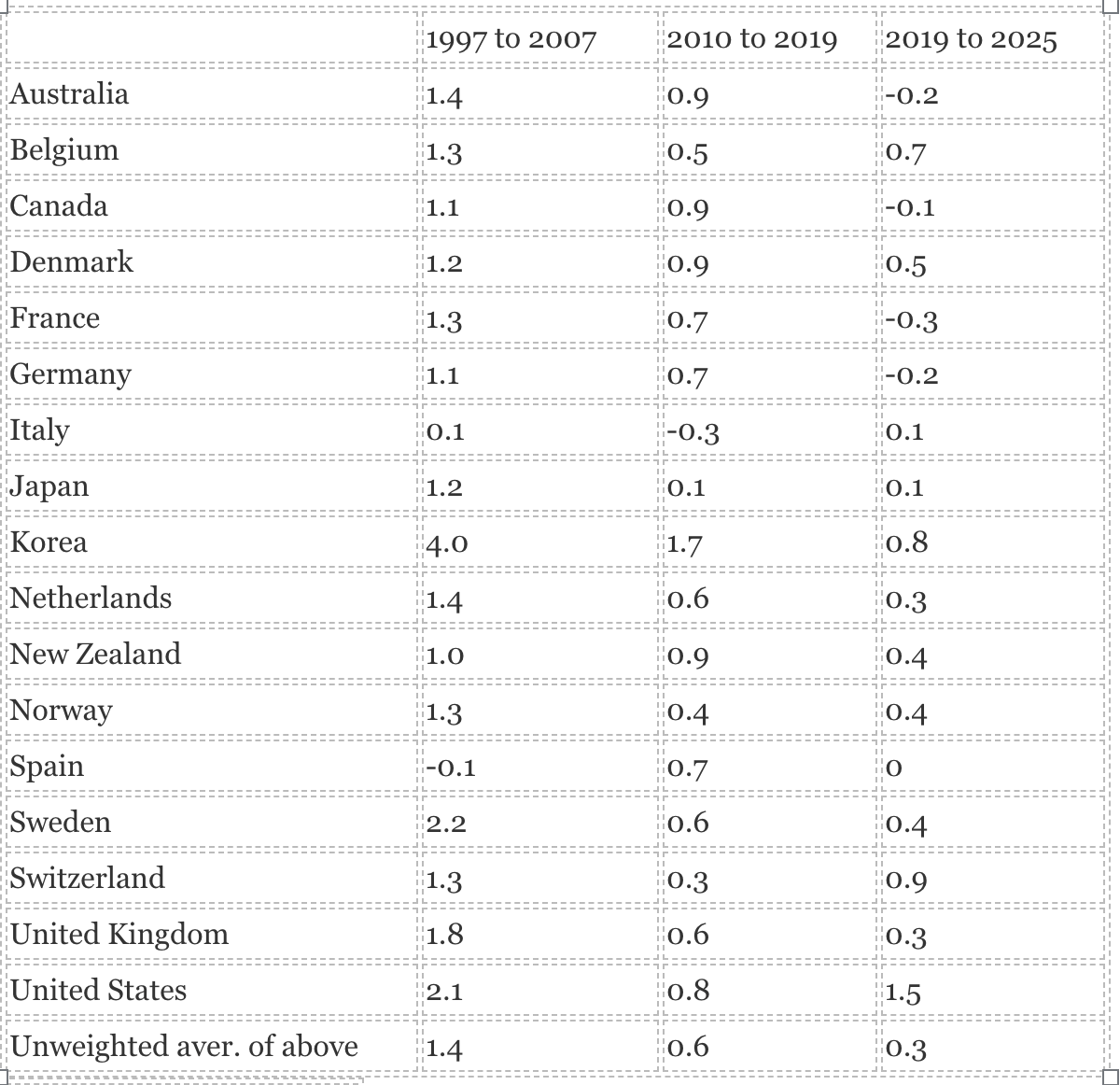

As Table 1 shows, however, the slowdown in productivity growth has affected all the developed economies to much the same extent. Australia’s lower rate of productivity growth in the 2010s and stagnation since the Covid pandemic is typical of almost all other developed economies.

The one exception is the United States where productivity growth has been significantly stronger than anywhere else since 2019. It seems likely that this relatively favourable US productivity growth reflects its technological leadership. Furthermore, the most plausible explanation for this faster US productivity growth is that it reflects the impact of AI where the US, along with China, is leading the world.

Consistent with this hypothesis, two questions follow: how much will AI lift productivity, and how much will it damage employment?

Table 1 Labour Productivity Growth

Average annual percentage change

The likely impact of AI on productivity and employment

The main impact of AI is likely to be on white-collar jobs involving access to information and its management, and record keeping. For example, one of the industries most affected will be healthcare where services will significantly improve through more personalised medicine, disease diagnosis, and drug development.

Record keeping in services such as accounting and auditing and paralegal services will also be significantly facilitated. Similarly, the administrative burden on teachers could be substantially reduced, allowing them to spend more time interacting directly with their students, while government planning approvals could be accelerated to the benefit of all concerned.

But the impact on overall productivity and employment is much less certain at this stage.

At one end of the spectrum of views, Kristalina Georgieva, the Head of the IMF, very recently warned that AI is “hitting the labour market like a tsunami”. Jamie Dimon, head of America’s biggest bank similarly forecast that it would soon need fewer employees. While the head of a major AI company, Anthropic, has predicted that the technology his company is developing could wipe out “half of all entry-level white-collar jobs”.

On the other hand, the evidence does not show that AI has had much impact on either productivity or aggregate employment so far. As stated the main impact is likely to be on white collar jobs, but an analysis by the Economist of employment changes since the second half of 2022 across more than 100 large white-collar occupations in America found that employment has risen by 4 per cent.

However, this increase in white collar jobs may be because it typically takes time for firms to invest in the necessary complementary assets and make other changes needed to take full advantage of a new technology. Indeed, the history of technological change shows that major new technologies only slowly diffuse from being at the cutting edge to general use in all relevant industries.

The latest McKinsey Global Survey – released three months ago – found: “While AI tools are now commonplace, most organisations have not yet embedded them deeply enough into their workflows and processes to realise material enterprise-level benefits”.

Most interestingly, a survey of the literature reported by the Brookings Institute last year found that at the firm level AI is associated with firm growth, increased employment, and heightened innovation, particularly in product development. Firms that are leading the way in AI development have experienced roughly 2 per cent additional sales growth each year, although that sales increase is not immediate and takes two or three years to trickle down.

For these firms that are most successful, employment growth tends to match the increase in sales growth so that productivity has not moved much over a decade of increasing AI investments. Instead, the benefits of AI seem to be coming from increased product innovation, ranging from improved products to breakthrough innovations such as Moderna’s exceptionally rapid creation of a vaccine against COVID-19.

This literature survey also found that investments in AI are associated with major changes in firms’ labour composition and organisation. “AI-investing firms increasingly seek more educated and technically skilled employees and alter their internal hierarchies”.

Finally, the relative growth in sales and employment by the firms that have most successfully introduced AI has resulted in some increase in industry concentration in favour of larger firms, which have extensive proprietary data and more resources to invest in bespoke AI models.

AI seems to be contributing to increased industry concentration and a more skill-biased labour market but has done little to increase productivity and raise living standards.

Looking ahead, as Nobel Prize winners, Daron Acemoglu and Simon Johnson, said recently whether machines “destroy or create jobs all depends upon how we deploy them, and on who makes those choices.”

Most importantly, rather than designing and deploying AI only with automation in mind, governments have a role in tapping its immense potential to make workers more productive by changing the nature of their work.