Time for tax reform – and this may be the moment to act

March 25, 2026

With inequality rising and budget pressures mounting, a rare political window has opened for meaningful tax reform – if the government chooses to act.

It is time for another round of tax reform to improve both equity and efficiency.

The last significant tax reform was in the last century. Despite Prime Minister Anthony Albanese’s well-known caution, the prospects for significant tax reform look brighter than in a long time.

First, a recent Senate Committee, chaired by the Greens Senator, Nick McKim, produced a report recommending the capital gains discount be reduced from 50 per cent to 33 per cent or lower. Second, a leading independent member of Parliament, Allegra Spender, has proposed reducing the capital gains discount from 50 per cent to 30 per cent and ring-fencing negative gearing so investment losses can only be offset against investment income, not wages.

Third, the Treasurer, Jim Chalmers has given several hints that he supports reform of the capital gains tax, as well as potentially other wider tax reforms. Not surprisingly, Chalmers is careful to say that it all depends upon Cabinet. However, with a huge majority in Parliament, plus support from the Greens and independents, and with two years to the next election, this budget presents the best possible opportunity to embrace tax reform.

Capital gains and negative gearing

In principle, there is no good case for taxing real capital gains at a lower rate than other forms of income. Each dollar of real capital gains raises a person’s taxable capacity just as much as a dollar of wages.

Thus, when the Hawke Government first introduced capital gains taxation, real capital gains were fully taxed and there was no discount. However, arguably calculating the amount of the real gain was too complicated and instead the Howard Government changed the system so that the nominal capital gains were discounted by 50 per cent to approximate the real gain. Such a high discount rate may have been reasonable if inflation is high – more than eight per cent – but this has not been the case for years, and a lower discount rate is therefore appropriate.

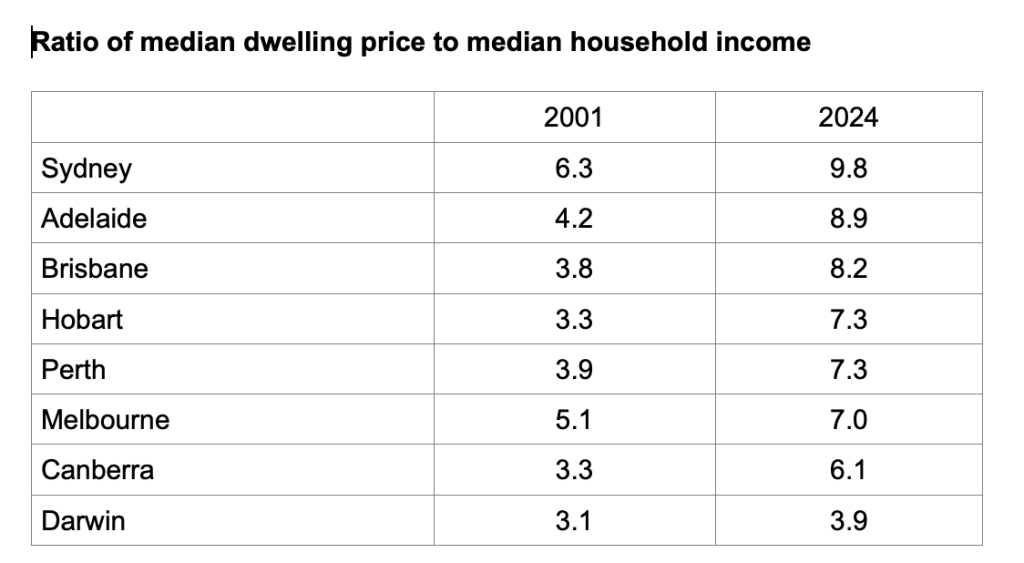

Furthermore, a major concern driving these reforms is the increase in inequality, often described as intergenerational inequity. As is shown in Table 1 below, over this century house prices have increased much faster than incomes.

This very rapid increase in dwelling prices has made it much harder for young people to become homeowners, and home ownership among young families is falling. For example, in 1971 home ownership among 30-34 year-olds was 64 per cent, but 50 years later in 2021 home ownership was only 50 per cent for people of the same age group. For 25-29 year-olds home ownership dropped from 50 per cent to 36 per cent.

Home ownership accounts for more than half of household wealth in Australia, and so this relatively rapid increase in dwelling prices has also meant that household wealth has increased much faster than incomes in recent years. In addition, this wealth is very unevenly distributed.

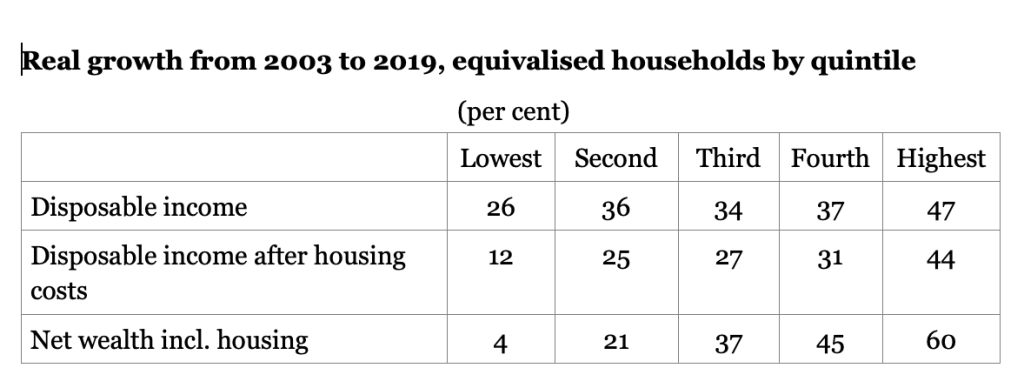

As can be seen from Table 2 below, over the period from 2003 to 2019, the increase in disposable income was not that different between the five quintiles in the income distribution; indeed, for the three middle quintiles the rate of income increase was almost the same. By contrast, the increase in wealth is much more different between the five quintiles, and the inequality of wealth has increased much more than for incomes.

Now nearly half of all national wealth (46-50 per cent) is held by the top 10 per cent of households, while the wealthiest 1 per cent of Australians own approximately one-quarter of the country’s total wealth. In contrast, the bottom 40 per cent of the population – nearly 11 million people – collectively hold less wealth than the country’s 48 billionaires.

A common justification for taxing capital gains more heavily and limiting the interest deductions from negative gearing to investment income is that this will reduce investor demand for housing and thus make it easier for young people to buy their first home. But the evidence does not really support this proposition. Instead, the reason for the high increase in dwelling prices is the limited supply. Chalmers recognises that and in his pre-budget speech last week he said that “Building better and faster is a key focus of our work with the States and private sector.”

Nevertheless, even if these changes to capital gains and negative gearing will not fix the housing crisis, there are still good equity reasons for making them. In addition, with wealth becoming so unevenly distributed, surely it is time to consider reintroducing death duties again. After all, taxing inherited wealth is surely equitable and is unlikely to have any negative impact on incentives. Certainly, there is no evidence that Australia’s economic performance improved after death duties were removed.

Resource taxation The oil crisis caused by the Iran war has led to a huge increase in energy prices generally and consequently resource company profits. These profits represent an economic rent, being far more than the return on capital necessary to sustain investment.

Not surprisingly, therefore, there have been increased demands to reform and/or increase the taxes on energy exports or resource rents.

Furthermore, the resource companies operating in Australia are often foreign owned and have a history of evading Australian taxes. According to the 2023 Budget Paper: “To date not a single LNG project has paid any PRRT, and many are not expected to pay significant amounts until the 2030s.” While Australia Institute research found that the gas export industry doesn’t even pay royalties on more than half of its exports.

It has become public knowledge that the Treasury is developing options for increased taxation of gas exports. According to Ken Henry, a former Treasury Secretary and a tax expert, if “a federal tax on fossil fuel exports [was set at the same rate as the current trading price for carbon credits - $38 per tonne – it] could raise $40billion a year in revenue and push gas prices lower.” I agree with Henry, that “should be child’s play now”.

But apart from taxing the excess profits/rents from fossil fuel exports there is a strong case for introducing a carbon tax more generally. Such a tax could raise significant additional revenue and would accelerate the switch to renewable energy, which is a key objective of Australia’s industrial policy, as well as costing the budget a lot less than the present subsidies to encourage the switch to renewable energy.

According to Ross Garnaut and Rod Sims, two top economists at the Superpower Institute, if the carbon tax were equivalent to the European carbon price, then this tax would raise more than $100 billion in its first year. The price of renewable energy would not change, and so those who can access renewable energy would be no worse off. But even if compensation were paid to those households and businesses who cannot access renewable energy, the net amount raised by a carbon tax would be substantial and would accelerate our take-up of renewable energy and future development.

But unfortunately, I will be surprised if in the middle of an oil crisis the Albanese Government has the courage to introduce a carbon tax in this year’s budget, notwithstanding its merits.

Lower personal taxes? Traditionally at least part of the additional revenue raised from tax reform has been used to compensate the “losers” by reducing income taxes a bit. No doubt there will be such pressures again this time if significant tax reform is a feature of this budget. There are, however, other higher priorities.

Australia is a comparatively low-tax country, and we are experiencing difficulties in adequately funding government services. Among 17 advanced OECD countries, only the US and Switzerland have a lower ratio of total tax revenue to GDP than Australia, and the only reason why the US raises less is because it has a much bigger budget deficit and relies more on foreign borrowings – a risky strategy.

Also, according to both the Treasury and the Reserve Bank our economy is operating at full capacity and that means the priority should be to reduce the budget deficit rather than add to household demand.

Indeed, if the budget deficit is not reduced, inflation is likely to be higher and the pressure to further increase interest rates will be substantially more intense. Such an interest rate increase would result in many households most feeling cost of living pressures being financially worse off, notwithstanding the small reduction in their income tax payments.

We need to – and should – raise more tax revenue if we want to preserve our democracy and stop the polarisation in response to increased inequality that is such a problem in many other advanced economies.