The cost of living crisis is really a housing crisis

August 9, 2024

The evidence shows that the only households whose living costs have risen faster than their incomes are those homeowners with a mortgage. For the other two thirds of households, their incomes have risen faster than their living costs. Policy should therefore focus on why mortgage costs have risen so dramatically.

The cost of living crisis is often attributed to an excessively high rate of inflation as typically measured by the consumer price index (CPI). More accurately it is assumed that living standards must have fallen because the rate of price increase has exceeded the rate of wage increase.

On this measure, real wages have fallen by as much as 18.5 per cent since the December quarter 2019 (see Table 1). While at the same time, the authorities consider that they cannot allow wages to catch up quickly if we want to bring inflation down.

Table 1

Comparison of wage and price increases between December 2019 and Mar 2024

However, if we really want to understand what is driving the cost of living crisis it is more productive to examine what is driving the increase in the CPI and how general that increase is.

In fact, the increase in the CPI mainly reflects the increase in house prices and if they are excluded then CPI has only increased by 4.6 per cent in the more than four years since the December quarter 2019. This is much less than the 18.4 per cent increase in the CPI over the same period when house prices are included (see Table 1).

Furthermore, as Table 1 shows, while real wages (as conventionally measured) have fallen since December 2019, if the price of new dwellings purchased by owner-occupiers is excluded from the CPI, then real wages have increased by 7.6 per cent (see Table 1).

But this measure of real wages is also flawed as the ABS measure of the CPI only includes the increase in house prices and does not include the impact of interest rate movements. It is not only the rise in house prices, however, that affects the cost of living; the rise in interest payments imposes another unavoidable additional cost on homeowners with a mortgage. So we need to consider the impact of the rise in interest rates on the cost of living as well.

In this regard in an earlier article, The cost of living and housing affordability, (June 25), I reported modelling by Ben Phillips at the ANU which showed that over the two years to August 2023 the cost of living for homeowners with a mortgage had increased by 17.5 per cent. This was much more than for renters and outright owners whose cost of living increased by 10.8 per cent and 11.7 per cent respectively.

A more recent update of this analysis by Phillips and Matthew Gray, projects that after allowing for the tax cuts, over the five years from December 2019 to December 2024, the living standards of mortgaged households will have fallen by 5.6 per cent. In contrast, the living standards of renters will have increased by 2.9 per cent, while the living standards of outright homeowners will have increased by 8.5 per cent.

To sum up, the evidence clearly shows that it is the cost of servicing mortgages which is fundamental to the cost of living crisis. Without this increase in mortgage costs there would be no cost of living crisis. This article therefore explores the impact of rising mortgage costs on the cost of living and why the cost of servicing a mortgage has increased so much.

The rise in mortgage costs

Obviously, mortgage costs depend upon the size of the mortgage that has to be serviced and consequently the amount of principal and interest that is paid on that mortgage each month.

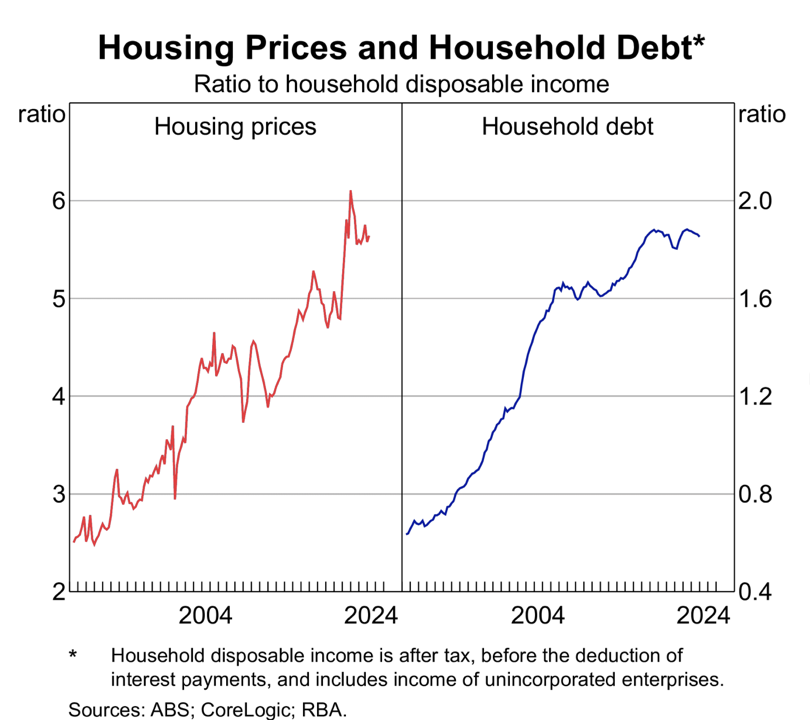

First, the size of a mortgage that has to be serviced depends upon the price of the dwelling, and over the last forty years housing prices have more than doubled relative to incomes from around 2½ per cent to around 5¾ per cent of household disposable income (see Chart 1).

Chart 1

Furthermore, as Chart 1 also shows, the rise in housing prices has been matched by an increase in household debt which over the same forty-year period has risen from around 0.55 per cent of household disposable income to around 1.75 per cent. In fact, in proportionate terms, the debt ratio has more than tripled, significantly faster than the increase in ratio of housing prices to disposable income.

But as Chart 1 shows, the increase in house prices and debt relative to household incomes has been fairly steady over the forty years. That therefore begs the question of why it is only in the last couple years of years that we have a cost of living crisis.

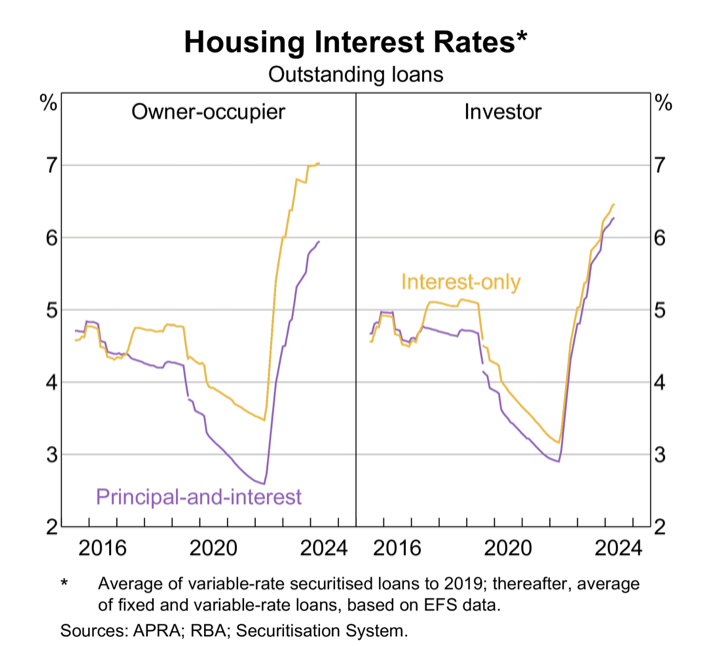

And of course, the answer to this question is the rise in mortgage interest rates which as Chart 2 shows for owner-occupiers have increased around 3.6 per cent to 7 per cent in the last two years. Furthermore, what matters most to owners with a mortgage is their monthly repayments, including both principal and interest and these repayments have increased proportionately with the increase in interest rates (see Chart 2). Chart 2

The impact of rising mortgage costs on living standards

For a household with a mortgage of $600,000 this increase in interest rates would have increased their monthly loan costs by $1300 in the last two years. This is huge.

For example, it would represent a 14 per cent loss relative to the disposable income of a typical dual-income household each earning the median wage for males and females respectively, the husband working full-time and the wife three days a week. By comparison, their real wages excluding the impact of rising house prices are about the same today as they were when interest rates first started to rise in May 2022 (see Table 1).

In other words, the so-called cost of living crisis is very much a housing crisis. Furthermore, while the results reported are for a $600,000 mortgage, which is fairly common, there are many households in the capital cities with substantially bigger mortgages than that. So many households would have experienced a significantly larger drop in their disposable income after allowing for their housing than the 14 per cent reported here.

What should be the policy response?

The alleged cost of living crisis is the number one political issue, but if the cost of housing for mortgagees is the main, or even the only reason for an insupportable cost of living, then what should be the policy response.

A big part of the answer to reducing mortgage costs is to achieve a reduction in interest rates. But interest rates are not controlled by the government and will only come down as inflation comes down.

Of course, the other factor pushing up mortgage costs is the increase in housing prices, thus increasing the size of the loan to be serviced. And here there is scope for policy action.

According to Dutton, the way forward is to allow would-be homeowners to draw down on their superannuation and thus be able to afford to pay for a home and service the loan.

The problem however is that all the evidence is that the increase in the price of housing reflects a shortage of supply, and the fact that this supply is very inelastic – that is the supply does not readily respond to an increase in demand because of local government zoning restrictions.

Unless these restrictions can be changed, increasing demand by allowing people to draw down on their superannuation will not make more houses available. Instead, it will just increase the price of housing even further and faster.

Realistically if we want to make housing more affordable then we must increase the supply. Furthermore, the supply of dwellings must be increased where people want to live, and that means increasing the density of housing in the middle and inner suburbs of our major cities. The supply of housing is much less of a constraint in rural areas, but that is matched by a lack of demand because that is not where the jobs are and where most people therefore want to live.

Thankfully the Minns Labor Government in NSW has grasped the nettle and is seeking to increase the density of housing in Sydney. But it would help if the NSW government got more help from the Federal Government, and also if the Federal Government increased dramatically its support for public housing.

Without this support, for increased housing density it will be difficult to increase the supply where it is wanted. And unless that housing supply is increased the cost of living crisis will continue for mortgagees, even after interest rates eventually decline.