The cost of living and housing affordability

June 25, 2024

The cost-of-living crisis mainly reflects a decline in housing affordability. A consequence is that this crisis is much worse for middle-income people, who are typically middle-aged, and who are most likely to have a substantial mortgage.

The opinion polls tell us that cost-of-living pressures are the number one political issue. This is the obvious reason why the Liberals under Dutton are rising in the polls, and Labor is losing ground electorally.

Furthermore, while many of us readers of Pearls & Irritations feel that Dutton has made a complete fool of himself over climate change, we need to remember that in the latest Resolve Poll, 54 per cent selected keeping the cost of living low as the most important issue, while just 7 per cent selected the environment and climate change.

So what would Dutton do?

For the first two years of his leadership Dutton was distinguished by having no policies of his own – just criticisms of the Government. But in his Budget reply speech last month, Dutton seized on Labor’s climate change and migration policies as being responsible for the increase in the cost of energy and housing respectively.

What Dutton would like us all to believe is that by walking away from renewable energy and reducing migration, energy prices and housing costs would come down and that would in turn solve the cost-of-living crisis.

Dutton’s alternative nuclear energy source, if and when it ever arrives, has been subject to much expert criticism elsewhere and will not be further explored here. But what this article will do is explore the facts relating to the cost of living, where and why it has risen and who has been most affected.

The contribution of energy and housing costs to increased living costs

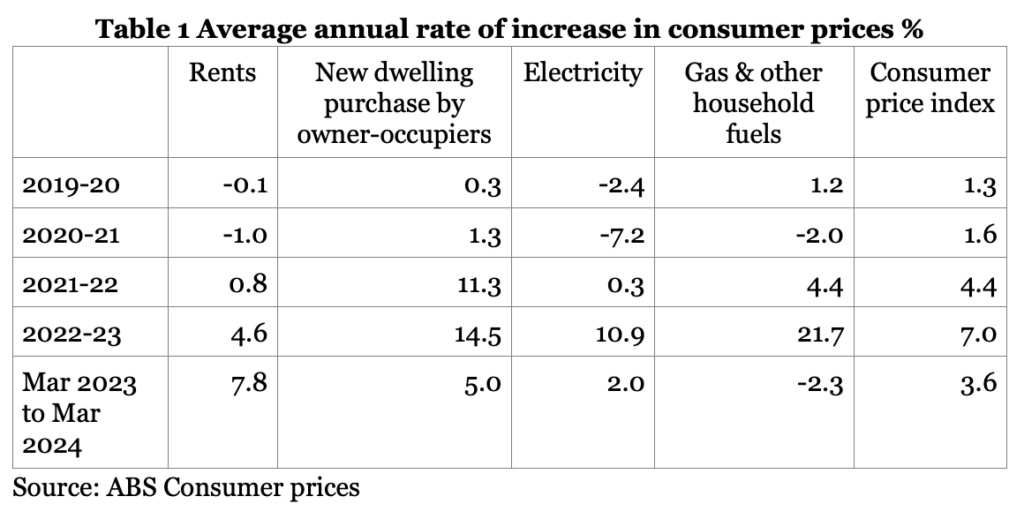

In Table 1 below the increase in energy and housing costs is compared with the overall increase in consumer prices for all goods and services consumed by households.

First, despite Dutton’s protestations, energy prices have not been a major driver of increased living costs. In fact, expenditure on energy only accounts for 2 per cent of Australian household consumption. Furthermore, as Table 1 shows the cost of both electricity and gas only spiked in one year – 2022-23 – and has made little difference to the cost of living since. The obvious reason for this spike was the Ukraine war and there is no reason to change from Labor’s targets to increase the use of renewable energy, which will not only benefit the climate, but is cheaper as well.

What has principally driven the increase in the consumer price index (CPI) has been the increase in rents and the price of new dwellings which have increased much faster than prices more generally (see Table 1); noting that interest rates are excluded from the CPI. Furthermore, after allowing for mortgage costs, housing costs typically absorb a third or more of the total household budget for a majority of households.

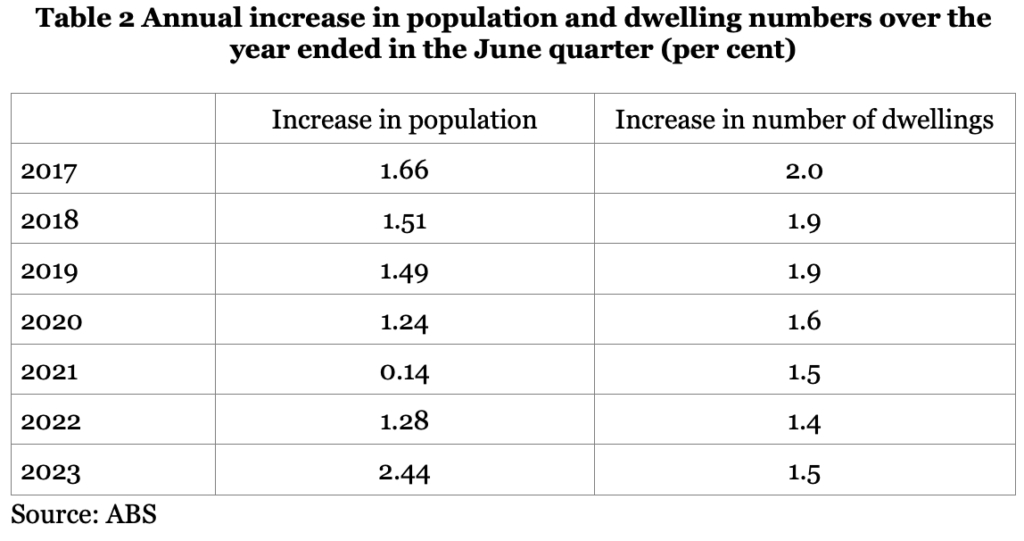

But as I explained in an earlier article the evidence does not suggest that the increase in housing prices has been driven by population growth. Instead, for every year between 2017 and 2022 the increase in population was less than the increase in the number of dwellings (see Table 2).

Restricting migration is therefore unlikely to result in lower housing prices. Rather the problem is on the supply side. We need to increase the availability of land for new dwellings, especially by increasing the density closer to the city centres where people most want to live. Also construction costs are rising too fast, but reducing migration risks making that problem worse.

In sum, apart from being bad policies in their own right, Dutton’s energy and migration policies are unlikely to have any noticeable impact on the rate of increase in living costs. Instead, we must continue to rely mainly on monetary policy by the Reserve Bank to achieve that reduction.

Which households are being most impacted by rising living costs?

Given the political significance of the cost-of-living crisis, it is also of some interest to explore more closely who is being most disadvantaged by the rising costs of living.

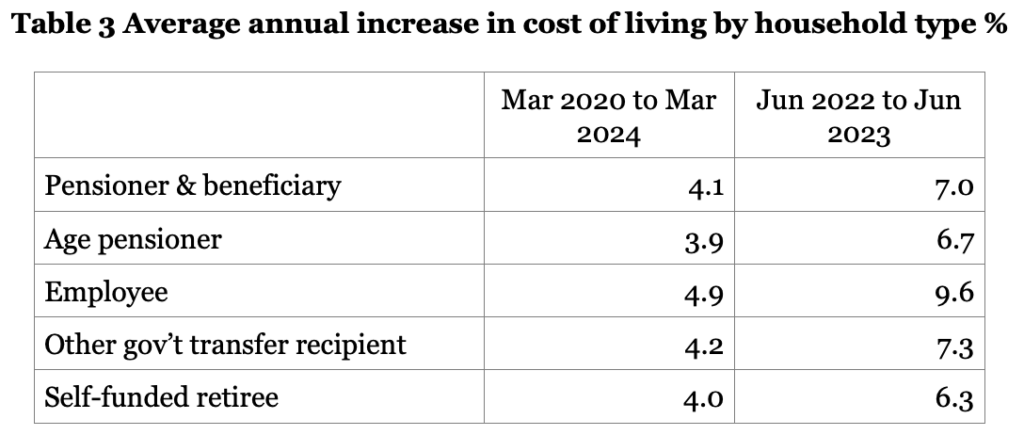

The ABS has provided data showing the increase in living costs for five different types of households as reproduced in Table 3 below for the total period since the covid outbreak and also for the peak year 2022-23.

What stands out is that over the last four years since Covid the increase in the cost of living has been much the same for different household types except those headed by employees. The major reason for this is that employees are much more likely to be servicing a mortgage, whereas the other household types are either renting or have paid off their mortgage.

Furthermore, the biggest difference in the rise in living costs was 2022-23 when interest rates were increasing most rapidly, while pensioners and beneficiaries typically had their support indexed by the consumer price index and self-funded retirees benefited from the increase in interest rates.

Thus what differentiates the increase in living costs for different types of households is most significantly whether or not they have a mortgage, and particularly how recently they bought their first home.

Using ABS data, modelling reported last August by Ben Phillips at the ANU found that:

“Homeowners with a mortgage turn out to have experienced a very large increase over the past two years of 17.5% - much more than renters who have had an average increase of ‘just’ 10.8%, and outright owners who’ve had 11.7%. First homebuyers who bought within the past three years faced the biggest living cost increase of 20.5%. Those who bought within the past three years but were ‘changeover’ buyers had an increase of 18.4%.”

As Phillips further notes “Younger Australians (under 35) are more likely to rent rather than mortgage. As a result, their living costs increased by ‘only’ 13.1% over the past two years, whereas the living costs of older Australians (aged 50-64) increased by 15.1%.”

Most recently, Phillips and Matthew Gray have updated this analysis and compared the increase in living costs between 2019 (pre-covid) and December 2024 for five different income quintiles, ranging from top to bottom. Their estimates necessarily include projections that take account of the income tax changes and changes in government payments that begin in July. They find that “Overall living standards were 0.6% lower in December 2023 than in December 2019, [but] this year they are expected to climb to be 1.3% higher than in December 2019.” Still not much improvement, and much less than the progress that Australians have come to expect.

Furthermore, there has been quite a bit of difference between the experience of different quintiles. The living standards of the lowest quintile of households are expected to grow by 3.5% over the five years, and the highest quintile’s living standard to grow by 2.7 per cent.

By contrast, the living standard of the second-lowest quintile barely grew, and the living standards of the middle and upper-middle quintiles actually fell and were lower in early 2024 than they had been in 2019. Where these middle-income earners living standards fell, it was because they had mortgages.

Thus, Phillips and Grey found that: “The living standards of mortgaged households fell by 5.6% between 2019 and December 2024. In contrast, the living standards of renters climbed by 2.9%, while the living standards of owners climbed 8.5%.”

Conclusion

Clearly the critical factor in determining whether living standards have actually fallen is whether or not there is a recent mortgage.

Young people under 35 mostly don’t have a mortgage – they can’t afford it – but that then means that their living standard is unlikely to be actually less than it was pre-covid. Similarly, older homeowners who have fully paid off their mortgage are not experiencing a lower living standard. But middle-income, middle-aged households with a substantial mortgage are experiencing the brunt of the cost-of-living crisis.

This poses difficult challenges for policy, which will be discussed in a follow-up article.