ALAN AUSTIN. Which party runs the economy better and how do we know? Part one.

November 25, 2019

The claim that the Coalition manages the economy better than Labor has never been valid. Yet the myth endures. Bizarrely, it seems to become more firmly believed as the evidence disproving it accumulates. So what is the reality? And how did the falsehood become so widely accepted?

Origins of the myth

The simple answer to the latter question is that powerful institutions have distorted Labors record since the early 1970s. Writing on the Whitlam years, 1972 -1975, the late social commentator Donald Horne claimed that virtually all the mainstream “news” about Gough Whitlams Labor Government was either distorted or false. On the economy, Horne said the media not only failed to report Australias rising inflation and unemployment in the context of a severe global recession, they failed to acknowledge that global recession at all.

Yes, inflation rose through the Whitlam years to peak at 15.4% in 1975 (World Bank Databank figures). The news media ran scathing attacks regarding this. But that was mild compared with elsewhere. The 1973 Arab oil embargo and OPECs huge oil price hike sent inflation soaring worldwide. It reached 16.0% in 1975 in the United Kingdom, exceeded 22.0% in Singapore, Japan, Mexico, and South Korea and went above 25.0% in Portugal, Greece and the Philippines. It hit 39.7% in Israel, 40.5% in Indonesia, 77.2% in Uruguay and 504% in Chile. Australia actually did quite well. Seldom was it ever recalled that in 1952, inflation went above 22% for two quarters in Robert Menzies third year as Liberal prime minister.

Successes ignored

Many of the impressive advances under Whitlam were either ignored or falsified. The budget surplus delivered in June 1973, after seven frenetic months of Labor reforms, was a healthy $348 million. The surplus a year later, at June 1974, was $1,150 million, the highest on record to that point, notwithstanding considerable outlays on a range of costly reforms. The budget outcome in June 1975 was yet another surplus, bestowing on Gough Whitlam the honour Peter Costello would love to have boasted of never having brought in a budget deficit. (The outcome of the 1975-76 budget, realised seven months after Whitlams dismissal, was a deficit of $1,499 million.)

Most outcomes during the Whitlam period were creditable, given the global challenges. But any downturn was depicted by the media as the result of Labors incompetence rather than of the inexorable impact of external forces.

The misreporting was so stark and so destructive that Donald Horne suggested that if Gough Whitlam had walked across Lake Burley Griffin, the newspapers next day would have declared: “PM Fails To Swim Canberra Lake”.

Deterioration under the Coalition

Throughout the Fraser years, the mild downturns under the previous Labor administration continued to be highlighted as evidence that Labor cannot run an economy. The fact that several indicators jobs, inflation, interest rates, GDP growth worsened considerably during the Fraser years was seldom reported accurately.

Interest rates, for example, peaked at 10.38% during the Whitlam years, which was cause for furious damnation by the anti-Labor forces at the time. Then, six years into the Fraser administration, inflation rose to 12%, then above 13.0%, staying at or above 12.0% until the hapless Coalition was replaced by the Hawke Government in March 1983. This was not reported fairly. The opposite, in fact, was implied if not stated. Despite the evidence of the data, the myth was bolstered and the 1983 election was largely fought on economic competence. Malcolm Fraser declared confidently in a campaign speech in February 1983:

Australia must have a government of prudent managers with stability, and a vision of the future, not the spend, spend, spend philosophy of Labor. No one wants a return to the chaos and insecurity of the Whitlam years.

Labors reforms

Throughout the Hawke years, the media reinforced the mantra that Labor was the party of inflation and unemployment. Eventually, however, Keating restructured the economy, opened it to global competition, and virtually all the key economic indicators rose impressively through the global rankings.

After Labor had “snapped the stick of inflation”, as Keating put it, the inflation and unemployment mantra was laid to rest. But it was soon replaced by the new mantra, equally false, that Labor was the party of high interest rates. In virtually every speech as party leader from around 1988 onwards, John Howard asserted that “interest rates will always be lower under the Coalition.”

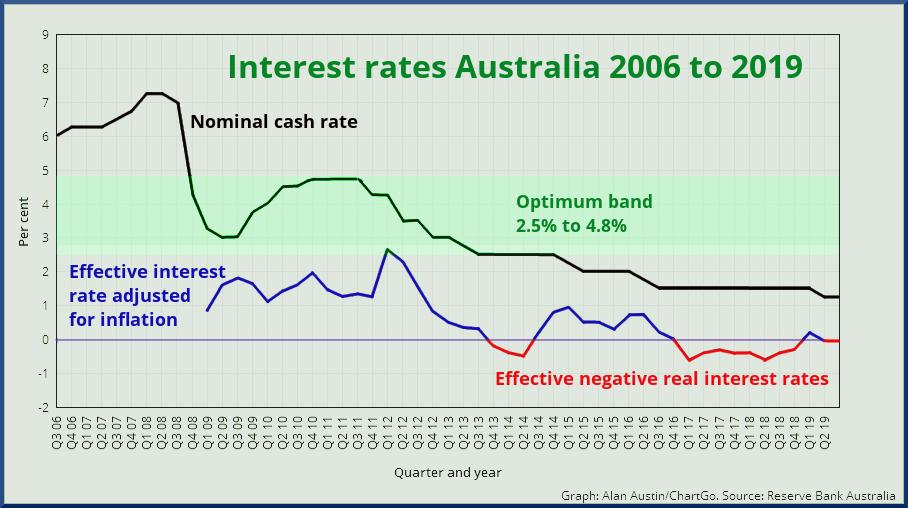

That served the Coalition well throughout the Howard years and the early Rudd period; until Labor proved through the global financial crisis (GFC) that it could indeed manage interest rates for the times. Only two economies succeeded in keeping interest rates in the band of comfort between 2.5% and 4.8% Australia and Mexico.

With the interest rates mantra also dead, the next false narrative was debt and deficits, based also on reporting those outcomes in Australia without reference to global events, notably the GFC. That also should have been put to rest now the Coalition has doubled all gross debt accumulated by all previous governments since 1854. But it hasnt.

Why does this matter?

Research has shown that economic management is the critical issue in determining federal election outcomes. Roy Morgan polling on election issues has found that: the economy and things economic [were] the biggest single theme to emerge. Economic Issues … were mentioned by 38% of Australians as the most important problems facingAustralia.

Climate change came second at 8.1%, followed by the political system at 8.0%. Other issues, including the personalities of party leaders, were of lesser importance.

If this is so, then perceptions of economic management many of which are entirely false are impacting the wellbeing of all Australians.

Which side really manages the economy better and how can we know?

See part 2, tomorrow.

Alan Austinis an Australian freelance journalist now living near Nmes in the Southof France. His special interests are the news media, religious affairs and economicand social issues which impact the disadvantaged.