DAVID LEITCH. We crunch the numbers and find costs of Labor's emissions target are not that big. RenewEconomy May 3 2019

May 4, 2019

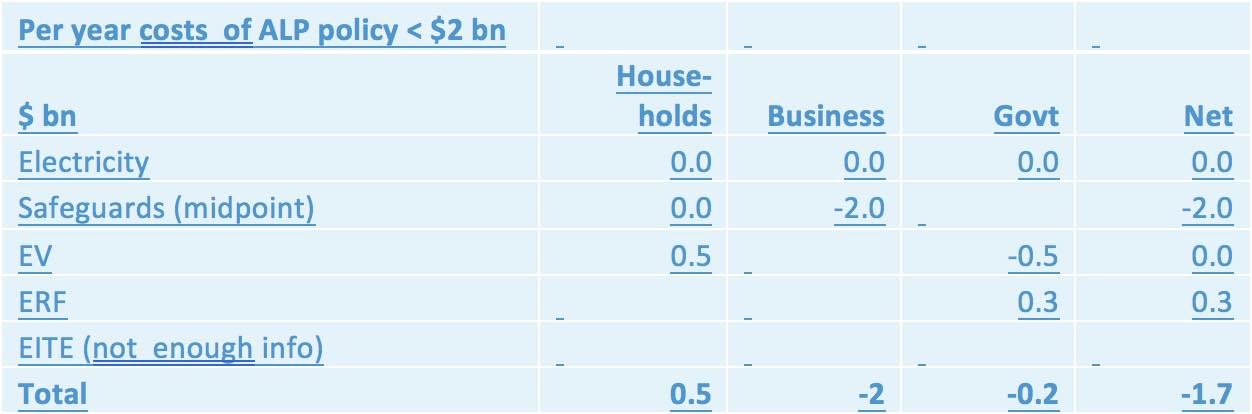

ITK has looked at Labors emissions reduction target the 45% cut from 2005 levels by 2030 and we estimate the community wide costs to be less than $2 billion per year, as summarized in Figure 1.

We estimate the electricity policy a 50% share of renewables by 2030 to havezero or close to zeronet cost to anyone, and that is government, business and households combined.

We see the Safeguard Mechanism policy, based on the scant details released to date, to affect impacted business by at most $3 billion per year but actually probably less than $1 billion per year. And for every 1 million electric vehicles there is lost fuel tax levy of$0.5 billion, however taxpayers avoid paying that $0.5 billion, so the community cost is zero.

In addition, changes to the Emissions Reductions fund [ERF] via announced policy that shifts the burden to the emitter and effectively makes it part of the broader safeguard scheme will save the Government about $3.2 billion over ten years ($320 million per year).

Figure 1 Estimated annual costs of ALP carbon policy. Source ITK, NDERV

In summary, we see the government as losing about $0.3 billion per year (fuel tax offset by ERF) and taxpayers losing $1 billion to $3 billion from safeguards less $0.5 billion fuel tax saved.

We dont do any fancy dancy long term global economic modelling coming out of the rear end of a black box.

Coalitions focus on carbon policy costs shows it still doesnt get it. It operates in a moral vacuum

The ALP has refused to put an explicit number on the costs of its decarbonization plan. In this note with one exception, we ignore the very substantive point about the costs of inaction or Australias relative costs and just focus on some illustrative numbers.The exception is around relative costs. Regular readers will note that ITK has been focusing on Chinas carbon emissions and its coal generators.

Whatever the cost to wealthy Australia of reducing emissions, the costs to relatively poor China, even more coal dependent, will be far greater. And of course the costs to oil producing countries are also going to be large.

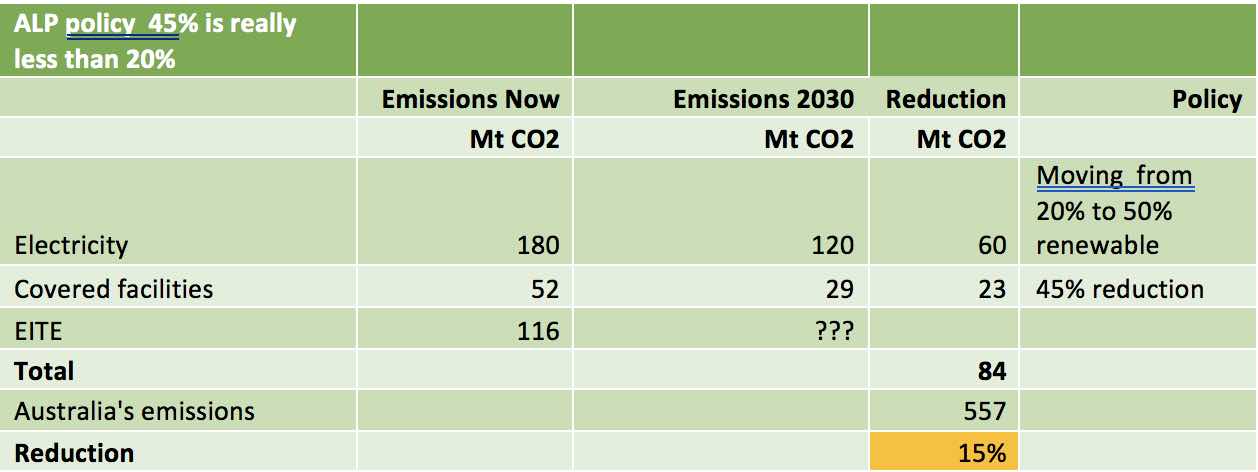

Emissions policy will need to be (much) tighter than the ALP has announced to get to 45% reduction

Recall this table from our previous note. I think of this as the 45% + 50% = 20% table and the real message is that EITE industries cant escape for ever. But.

Figure 2 Only 20-30 mt of abatement required. Source: ITK

Figure 2 suggests that abatement of only 20-30 million tonnes will be required under the policy announcements so far under the Safeguards scheme outside of electricity. For details of how this estimate is obtained see:Adding up ALP carbon policy

Expanding a little.

Electricity 50% renewables: zero cost to Govt under NEG, zero cost under Reverse auctions, arguably zero cost to consumers

ALP policy is for 50% renewable electricity by 2030. So the biggest carbon emitters in the country, namely AGL and the QLD Government-owned generators, arent, as I understand it, subject to the Safeguard Mechanism.

The roughly 8 GW of variable renewable energy [VRE] ie wind and solar that is coming online to 2020 will lead to significant emissions reduction. As such the incremental cost of that is zero.

Most industry studies, I would argue, show an overwhelming consensus that find that the required price ie LCOE, or LRMC of new wind and solar is lower than that of new coal or gas.

High coal prices at least in NSW together with ongoing capex means, in my opinion, that the annual cash cost, expressed in $/MWh of existing coal generators is close to the LCOE of new wind or solar.

And those coal plants, together with existing hydro, Snowy 2 and gas have the flexibility to supply the balancing load out to 2030.

So my take is that the cost to business, as a working assumption, and at current coal prices, of a 50% renewable target is zero or close enough to is to not be worth arguing the toss.

We think that if the ALP wins the election its chances of getting a NEG through lower house will be strong. In the upper house nothing is certain, but the mandate will be very clear.

IF, IF the ALP wins the election the anti climate change minority in the Coalition will see their standing reduced.

The moderates will be emboldened and so the Coalitions opposition to a NEG in the Senate may be less. Lets face it the dominant clique in the Coalition was a minority in terms of numbers of members. They just held the reins.

However the ALP also or alternatively, its still not clear to me, intends to put $10 bn into the CEFC which Mark Butler has said he expects will be used to run reverse auctions.

ALP announcements and policy suggest the remaining task will be via either the NEG or the CEFC. If its done under an NEG there is no cost to Govt.

The CEFC could either directly equity fund new investment or it could provide price guarantees (via reverse auctions). It seems clear to me that reverse auctions provide a more hands off approach but its easier to calculate the numbers using direct investment.

Lets assume that new wind and solar projects cost $1.7 m/MW (equally weighted average of wind and solar in 2019 prices) and lets assume away MLF (marginal loss factors). Finally, projects are 40% equity and 60% debt.

These assumptions lead to a conclusion that the CEFC could own 15 GW of additional VRE (wind and solar) and produce 20% of the NEMs current output

Figure 3 Impact of CEFC receiving $10 bn on generation. Source: ITK

We think that if the CEFC is providing a revenue guarantee in the form of a contract for differences [CFD] then possibly even more investment can be supported. This would be on the basis that the CEFC would have to reserve for the value at risk [VAR].

The VAR is only a fraction, say 10-20% of the value of the project and represents say the biggest difference that might reasonably be expected between the contracted price under a reverse auction and the market price.

On the simple assumptions that 1 TWh ofrenewables reduces emissions by 1 mt then the CEFC investment could reduce emissions by 40 mt. There is no cost to the Government as a return on equity is obtained.

The more important part of the 50% renewable policy might be the $5 billoin infrastructure fund. ITK had always assumed that fund would be used for electricity transmission, but more recent announcements suggest that the ultimate destination is gas.

At this stage Ill just point out that the leverage to decarbonization of speeding up electricity transmission development is far greater than investing in gas.

Or, to put it another way, the NEM wont easily get to 50% renewable without significant transmission investment and Federal Government support and investment could greatly assist that process.

No cost to Government of safeguards tightening

The Safeguards mechanism, that is how the baselines for Australias large, non exempt, non electricity sector, emitters will be tightened have yet to be worked out.

As figure 1 above shows ITK estimates there will only be about 20-30 mt of abatement required under this policy depending on whats exempt etc.

Most of us envisage four ways this obligation could be satisfied.

-

Change processes to reduce carbon emissions. This is the long hard road that everyone will have to travel over time;

-

Buy permits overseas at some cost.

-

Buy ACCUS. ACCUs are currently trading at $16.50. ITK is not a fan of ACCUs but certainly wed expect the price to go up to be comparable to international carbon credit prices over time.

-

Buy electricity permits from electricity producers who have overachieved. This requires the electricity sector to be linked to the Safeguard scheme. No detail on whether or how this might be achieved has yet been released. But we think its an obvious way to proceed.

Safeguards cost to business likely to be at most $3 bn per year

Our conclusion is that after excluding electricity andEITE business at most there is 20 mt of reduction required under 45% reduction using the expanded Safeguards scheme. But for the sake of illustrate we also show a 50 mt reduction in facilities covered by Safeguards.

Figure 4 Estimating safeguards cost to business. Source: ITK

EITE business are defined to have no net relative cost

By definition a business falling into EITE category doesnt pay any more than the global average for its sector. Therefore by definition it suffers no global disadvantage. So there is no net cost.

Of course, Australia has a lot of these businesss but thats the reality of climate change.

We also have great potential to build new business in traditional industries like mining (nickel, cobalt, lithium, graphite) but also to export energy, to provide software to energy companies, to grow into energy intensive businesses again like data storage but using what will be in ten years time globally cheap renewable energy.

Emissions Reductions Fund [ERF]

This fund had $2.55 bn allocated to it of which $2.3 bn is committed and $0.4 b has actually been spent. The Coalition has committed a further $2 bn if re-elected.

Of the $2.3 bn committed (and payable over ten years) we understand that many of the winning bidders are unable to fulfil their contracts, perhaps as much as 50%.

ALP policy is to switch this fund from a taxpayer funder to emitter pays model, in our view effectively making it part of the safeguards mechanism. On that basis we estimate that under ALP policy the Federal Govt would avoid about $3.2 bn over ten years of payments.

| Savings from killing the ERF | |||

| $bn | In operation | Post election | Total |

| Tranche | 1 | 2 | |

| Announced | 2.6 | 2.0 | 4.6 |

| Committed | 2.6 | 2.6 | |

| Allocated | 2.3 | 2.3 | |

| Savings from switching to emitter burden | |||

| Unallocated | 0.3 | 2.0 | 2.3 |

| Expected to fail | 0.9 | 0.9 | |

| Avoidable cost | 3.2 |

Figure 5Avoided Govt spending under ALP policy. Source NDVER, ITK

EV policy: Every 1 million electric cars is 3 mt annual CO2 saved and $0.5 bn fuel tax lost

Electric vehicle policy could at most drive down emissions by 25 mt (50% of all light vehicle kms travelled), recalling that total transport emissions are 100 mt and car emissions are about 50 mt.

Costs of the EV rollout to the Federal Government are mainly a reduction of fuel tax excise received. Of course fuel tax excise is more or less another carbon tax, one broadly accepted by the community, but lets not go there.

For every 1 mm evs sold there is about 2.5 mt per year of carbon saved and $0.6 bn of lost fuel tax revenue . This makes for expensive abatement.

A road tax, or various other policies could eventually recover this cost, although one suspects that the 120 year old car business might be about to undergo various other changes in the next decade that could eventually impact taxes.

Figure 6 Impact on fuel excise, carbon of every 1 mn EVs

The CO2 savings are from petrol/diesel emissions avoided and assume that the electricity is carbon free.

David Leitch is a regular contributor toRenew Economy. He is principal at ITK, specialising in analysis of electricity, gas and decarbonisation drawn from 33 years experience in stockbroking research & analysis for UBS, JPMorgan and predecessor firms.

On this basis we think we could say that the Government will actually improve its budget position. It gets rid of the ERF and incurs a minor loss of fuel tax.

v