Economic outlook – will 2024 be a hard, soft or no landing?

December 22, 2023

On the Australian economy, bulls and bears cannot both be right. 2024 will decide the fate of both economies and markets, a hard, soft or no landing.

Global Outlook

Bulls argue that the worst is over since the back of inflation has been broken. While elevated interest rates will not fall until next year, they have peaked notwithstanding some central bank still warning of possible further rate rises.

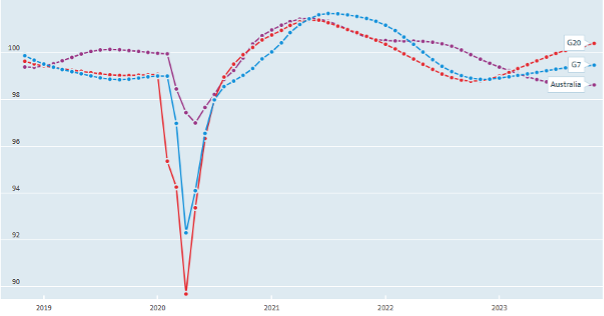

But the recent rise in the US Federal Reserve Bank’s net assets which has injected liquidity into financial markets confirms that its hawkish stance is over. Moreover, leading economic indicators for major economies point to the recession risk having passed, except for Australia. See next chart. Either there will be no economic landing or just a soft one.

OECD Composite Leading Economic Indicators for G20, G7 and Australia

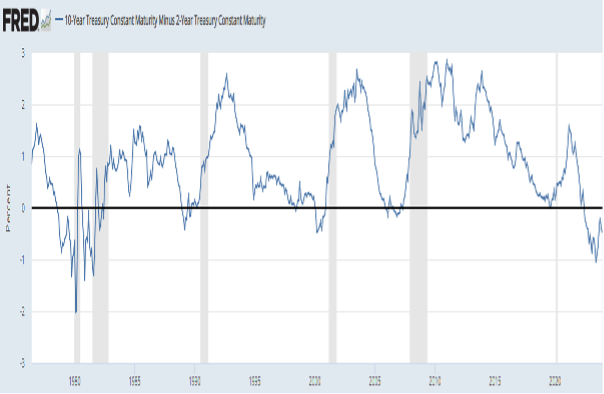

Bears say an inverse yield curve, whereby the ten-year treasury bond yield is lower than the two-year yield, has never been wrong in predicting an economic recession. Furthermore, when the yield curve starts un-inverting – as is happening now – a recession is imminent.

Also, the sharp increase in all interest rates over the past two years means shares like bonds and commercial property must undergo a price adjustment. Bears warn this is the lull before a storm.

US Yield Curve Inversion Always Precedes an Economic Recession (Grey Bars)

Also, oil price spikes are normally followed by recessions. Oil prices are up sharply since April 2020.

Australian Outlook

In Australia, the Bull argument is that the economy has remained resilient notwithstanding continued business and consumer gloom about the future. Annual consumer price inflation has almost halved since it peaked at 8.4% last year. This bodes well for interest rates falling in 2024.

Unemployment remains historically low, thanks to continued labour shortages because of migration halting and baby boomers taking early retirement during the pandemic. Households in Australia still have $183 trillion of excess savings accumulated during lockdowns to help withstand any temporary economic hardship in the first half of 2024.

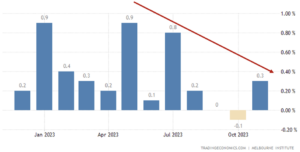

The Melbourne Institute’s Monthly Inflation Gauge

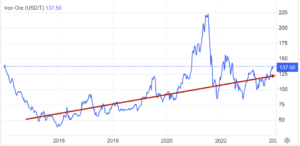

Stage 3 tax cuts from July 1st 2024 will boost household disposable income by $31 billion in 2024/25 and much more thereafter. Iron ore prices remain high and coal prices are above their historic average. immigration is quickly filling skill shortages that arose when the border closed during the Covid epidemic. This has stopped any wages/prices spiral while allowing businesses to pass on higher wage, material, and utility costs in higher prices.

Business investment is soaring in both mining and non-mining sectors. Also, credit is not overly tight and interest rates are simply returning to what they were before the onset of secular stagnation in 2012. Mortgage arrears and defaults are no higher than before the pandemic.

Iron Ore Prices (USD/Tonne)

Economists got 2023 wrong when their consensus forecast was for a global and local recession. They will be wrong again in 2024 because their economic models do not take account of the huge changes in technology, especially artificial intelligence, which will turbocharge productivity, investment and prosperity.

The transition from fossil fuels to renewables reaffirmed by the recent COP28 Conference will advantage Australia with its abundance of sun, wind, and critical minerals. That is why the share market has taken off. This is not just a Santa Rally, but the start of the next secular bull market. So, says the Bulls.

The Bear case for Australia is that the interest rate hike has been one of the sharpest and fastest in Australia’s history leaving many mortgagors, both household and businesses, struggling to survive. This will result in a rise in mortgage arrears and defaults in the new year.

More generally living standards have fallen to an extent not seen since the great depression of the 1930s. Real household disposable incomes recorded their eighth consecutive quarterly decline falling 6.6% over the past year. High inflation, interest rate hikes and tax bracket creep (together with the end of the LMITO benefit) were the main causes of living standards falling.

Household Real Disposable Income and Consumption Per Capita (Quarterly Data, Mar 2000 - Sept 2023)

After accounting for population growth, Australia’s real GDP shrank 0.5% on a per capita basis in the September quarter. Given that it also shrank 0.1% in the June quarter, Australia is now a “per capita recession”, two quarters of negative growth per head of population. Since real GDP growth has been slowing since the start of 2022 a full recession whereby real GDP itself declines is on the cards in the first half of 2024.

High interest rates, lower immigration, fewer infrastructure projects, a faltering Chinese economy, and shrinking household disposable incomes will grind the Australian economy to a standstill. Corporate earnings and hence share prices will dive. Don’t be fooled by the present market hype. So, says the Bears.

Who is right?

Bulls and bears cannot both be right. 2024 will decide the fate of both economies and markets, a hard, soft or no landing.

If present positive investor sentiment wins out it will be the second year that economic crystal balls got it wrong. Normally, tight monetary policy (especially if combined with higher oil prices and lower living standards) triggers a recession after a lag. So, if that does not happen this time economic theory will be turned on its head.