International comparisons of monetary policy

September 25, 2024

Much of the expert commentary on Australia’s monetary policy settings is guided by what is happening in other countries. However, monetary tightening can have a markedly different impact in different countries, and while Australia appears to have been more cautious, so far it seems to have managed well.

A brief history of recent monetary policy in the Anglophone countries

At the height of the COVID epidemic in 2021, the interest rates charged by central banks fell to extraordinarily low levels. For example, in Australia, the UK, and the US policy rates all fell to 0.1%. Canada and New Zealand were a little higher, at 0.3% and 0.4% respectively, while the European Central Bank’s policy rate was an extraordinarily low -0.5%.

But supply restrictions, partly caused by the war in Ukraine, and the general easing of fiscal and monetary conditions, resulted in inflation taking off, with consumer price increases in 2022 averaging 6.6% in Australia, 6.8% in Canada, 7.2% in New Zealand, 9.1% in the UK, and 8.0% in the US. Peak inflation rates were even higher, with Australia, for example, peaking at 7.8% for the four quarters ending in December 2022.

Not surprisingly therefore, monetary conditions were tightened everywhere and interest rates increased. The Reserve Bank has, however, been criticised because the rise in interest rates started earlier in all other comparable countries and went higher as well. In the last quarter of 2023, for example, the Reserve Bank cash rate reached 4.35%, compared to 5.0% in Canada, 5.5% in New Zealand, 5.3% in the UK, and 5.4% in the US.

Now all these countries have started to lower their interest rates, except for Australia. However, the RBA governor is warning us not to expect an interest rate cut before next year, while on the other hand financial markets and some economists, including me, think that there should be a cut in December.

In sum, other countries have apparently been quicker to tighten and raise their interest rates and by more, and also quicker again to start relaxing their monetary policies and cutting their interest rates.

An international comparison of interest rates

But before rushing to judgment that the RBA has been too timid, we need to appreciate that for institutional reasons the impact of official interest rate variations can differ significantly between countries.

The critical difference is that the proportion of loans at variable and fixed interest rates varies substantially between countries. Where most loans have variable interest rates, monetary policy will have shorter lags and a larger impact. Whereas when most loans have fixed interest rates, then borrowers are unaffected by interest rate changes until the fixed term of the loan runs out which could be in a few years.

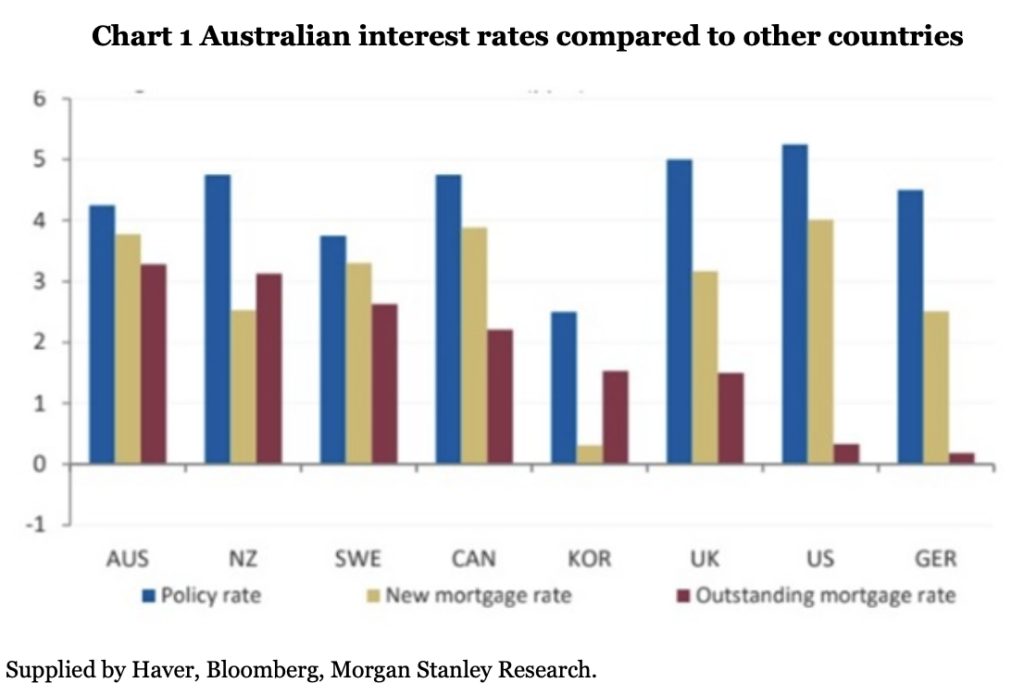

The chart below, produced by Ian Verrender of the ABC, shows that the policy rate, depicted by the blue bar, is lower for Australia than for New Zealand, Canada, the UK, the US and Germany. However, Australia is right up with the highest interest rates for new mortgages, as depicted by the yellow bar. But what is most important is the red bar which shows the interest rate on all outstanding mortgages, and this shows Australia has had the highest interest rates overall despite lower official rates.

Results achieved

In short, comparing what is happening to official interest rates in different countries does not tell us a lot. Rather we should focus on their impact on the economy – are the changes in interest rates achieving the desired balance between bringing inflation down while maintaining employment?

When we compare the Australian record with say, the US, the Australian authorities, both the RBA and the government, seem to have done quite well. True, the US has got inflation back down to 2.5%, while the Australian inflation rate for the four quarters ending in June was 3.8%. But forecasts for the monthly CPI by economists at the Commonwealth Bank and Westpac are that consumer prices will only have increased by 2.7% over the 12 months ending in August, and we are certainly getting inflation down.

Furthermore, Australia has been significantly more successful in maintaining employment than the US. The proportion of Americans in a job is still lower than it was before the pandemic, whereas in Australia there is a record proportion of people in a job, about 1.4 percentage points higher than pre-COVID.

Similarly, Australia has done better than the other Anglophone countries in keeping unemployment down. In Canada, the unemployment rate has risen to 6.6%, and to 4.4% in the UK compared to 4.1% in Australia.

Conclusion

Monetary policy tightening has been of much the same order in Australia as in other comparable countries, and the results in terms of inflation and employment have been at least as good.

But that said, all the other countries have moved to cut their interest rates, and it seems that Australia should do that too. Much of the recent increase in employment has been in government-funded jobs such as childcare and residential aged care, but these are one-off increases and are unlikely to continue. So, to preserve the balance between employment and inflation increases the RBA needs to act soon to cut interest rates – if not at its next meeting, then in December.