Is China heading for some kind of ‘currency crisis’?

April 4, 2024

In the short term, no. But over the medium- to longer-term, the possibility of a Chinese ‘currency crisis’ – by which I mean an abrupt fall in the value of the renminbi against other currencies, prompted by large capital outflows, and possibly entailing large falls in the values of other Chinese assets – cannot be dismissed.

According to the People's Bank of China, China pursues “a managed floating exchange rate regime based on market supply and demand with reference to a basket of currencies”. It’s a system similar in many ways to the ‘crawling peg’ which Australia maintained between November 1976 and December 1983.

In principle, maintaining a fixed or quasi-fixed exchange rate regime requires a credible and fairly stable relationship between a country’s foreign exchange reserves and some measure of its domestic money supply.

In a currency board system such as Hong Kong’s, this is mandated by law. In other less rigid systems, central banks have a degree of discretion as to how strictly they seek to maintain a relationship between their FX reserve holdings and the domestic money supply. The extent of that discretion will depend partly on the ‘credibility’ of the central bank concerned – which is in turn largely a function of its ‘track record’ in maintaining the exchange rate close to its declared or targeted value – and partly on the condition of the country’s balance of payments. In particular, the central bank of a country running persistent current account surpluses – or one running current account deficits which are routinely and comfortably financed by foreign direct investment inflows – will have more latitude in departing from a strict relationship between foreign exchange reserves and the domestic money supply, than the central bank of a country running persistently large current account deficits which are financed by foreign borrowings.

For most of the past forty years China has been in the former category. Although it incurred current account deficits on occasion during the 1980s, it hasn’t since 1993. Its current account surplus has averaged almost 3% of GDP since then, peaking at 9.9% of GDP in 2007. On top of that, China has attracted inward foreign direct and portfolio investment averaging 1.6% of GDP annually since 2010. Together with its current account surplus, that’s been more than enough to fund China’s significant capital outflows – on Belt and Road projects and other investments – that have resulted in China becoming a significant net creditor, with overseas assets exceeding overseas liabilities by almost US$2.9 trillion (equivalent to 65% of GDP) by 2023.

China has also been willing, since its last bout of financial instability in 2015-16 (when the Shanghai stock market dropped by 49% in just over six months, and China’s FX reserves fell by almost US$500 billion), to impose increasingly stringent controls on capital outflows.

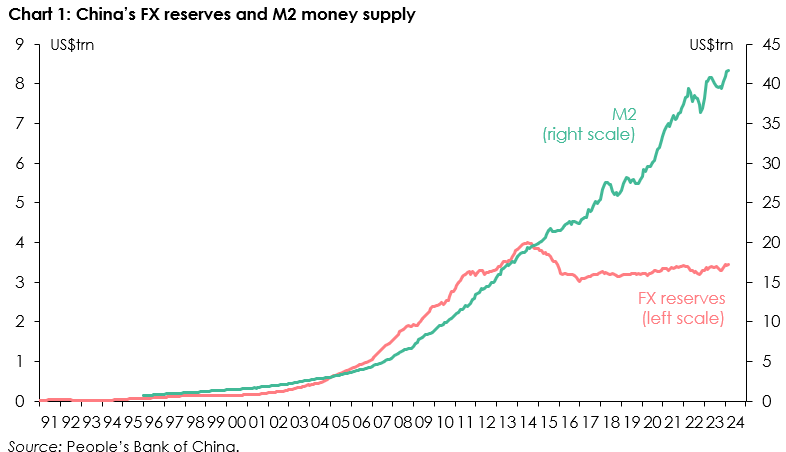

Hence China has been able to ‘get away’ with a significant departure from the almost linear relationship it had maintained between the PBoC’s FX reserves and the M2 measure of China’s domestic money supply (as shown in Chart 1).

However, it may not be able to do so as readily over the remainder of this decade.

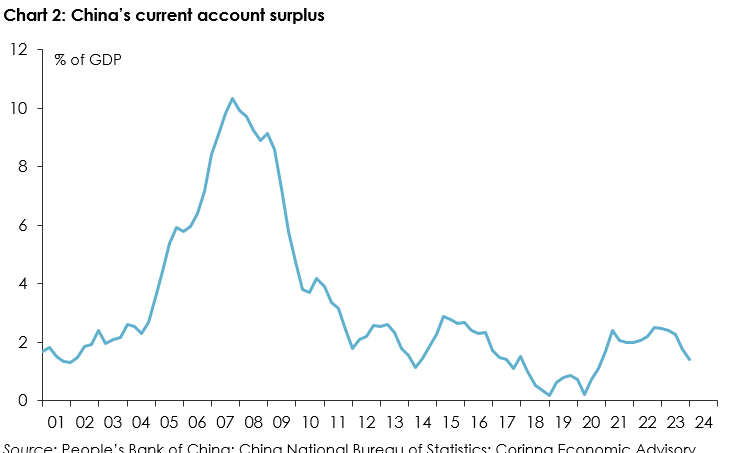

First, China’s current account surplus is shrinking – from a peak of almost 10% of GDP in 2007, to just 1.4% of GDP in 2023, after widening temporarily during the Covid pandemic (see Chart 2).

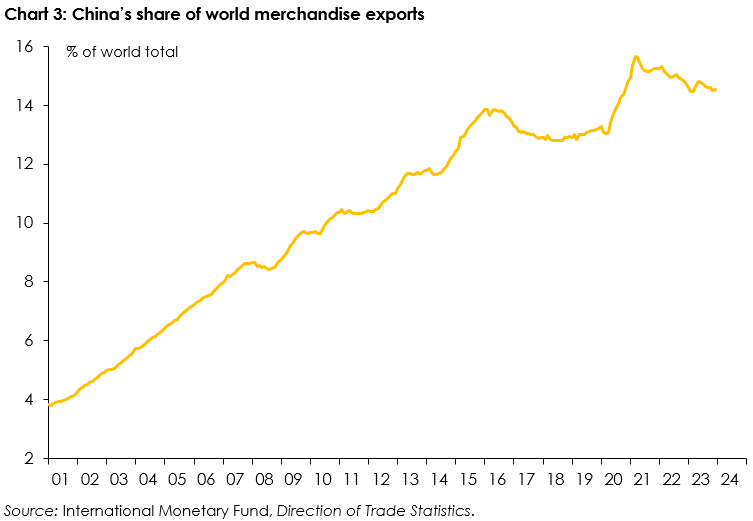

Although some of China’s exporters – in particular of electric vehicles and renewable energy generation equipment – are achieving substantial successes, in total China’s exports of goods have ‘flatlined’ since the beginning of 2022, and China’s share of total world merchandise exports has fallen by more than a percentage point from its peak in early 2021 (Chart 3).

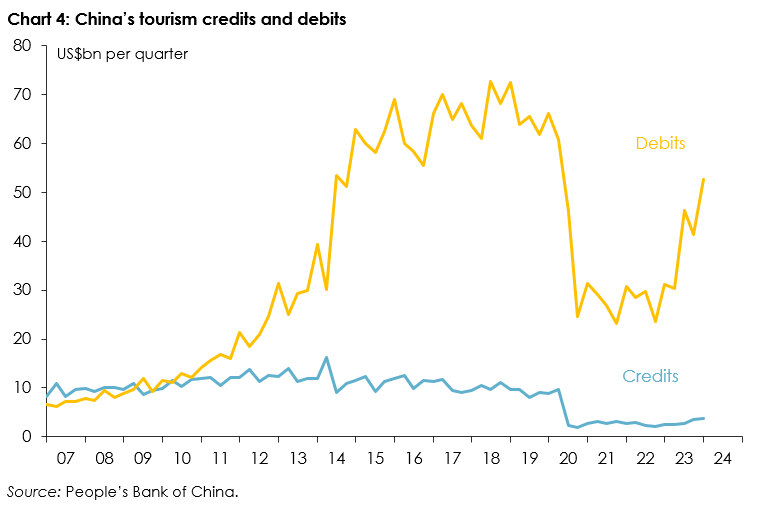

China’s services deficit is also widening. This largely reflects the divergent trends in tourism, with Chinese tourists again flocking to overseas destinations, as they did before Covid: but far fewer foreigners are visiting China than before the pandemic (Chart 4).

Additionally, and perhaps surprisingly given that China is (as noted earlier) a significant international creditor, it runs a large and growing deficit on primary income (that is, income earned on China’s investment abroad, minus income paid on foreign investment in China). Over the past four years this deficit has averaged US$136bn per annum, almost exactly the same as China’s deficit on trade in services, and equivalent to about ¾% of China’s GDP. This suggests that a lot of China’s overseas investments have (to date) been relatively unprofitable.

All of this suggests that it’s not impossible that China’s current account could swing into deficit at some point during the remainder of this decade.

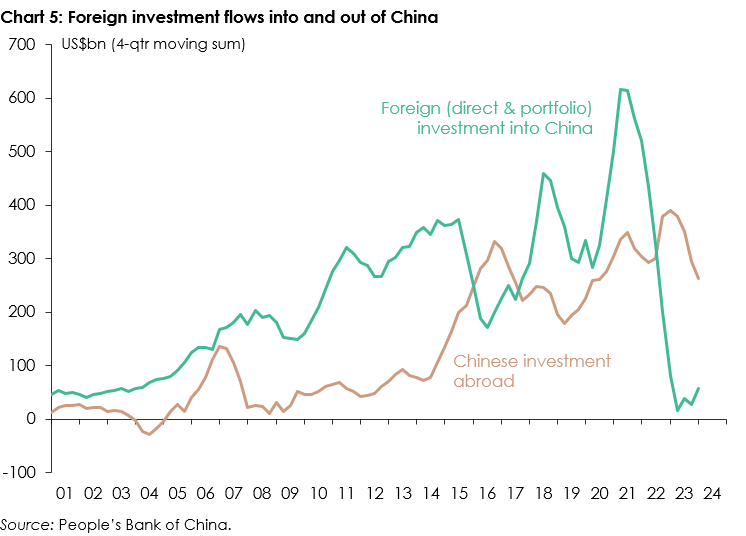

Second, foreign investment inflows into China have almost completely dried up. Net foreign direct and portfolio investment into China last year totalled just $57 billion, the lowest number since 2002, and down from an average of over US$400 billion per annum in the five years to 2022 (Chart 5).

This trend appears to be the result of conscious decisions by multi-national companies and institutional (portfolio) investors to reduce their exposure to China, for a combination of strategic, commercial and political reasons.

Chinese foreign direct investment abroad has also slowed, albeit by less than foreign direct investment into China, at least in part because of more stringent scrutiny of Chinese investments (especially by state-owned enterprises) in Western economies. And Chinese outward portfolio investment has been encouraged by the largest positive interest rate spread between the US and China since 2001 (for most of the period between 2001 and 2022, that spread was negative, ie Chinese interest rates were higher than US interest rates).

If these trends were to continue, China’s shrinking current account surplus may be more than offset by growing net private capital outflows.

And that would become an even bigger problem if China’s current account balance were to swing into deficit, as well it could if total exports continue to decline and imports were to recover from their recent relatively depressed levels (reflecting subdued domestic demand).

Indeed, such a development, were it to be anticipated (without it actually occurring, or before it did) could encourage additional capital outflow, including through unofficial channels (what is known to economists as ‘capital flight’), which could in turn be sufficiently large to make an anticipated renminbi depreciation a self-fulfilling prophecy.

That is what happened between 2013 and 2015. Although China’s current account surplus widened (from US$148 billion in 2013 to $293 billion in 2015), direct and portfolio investment flows turned around from a net inflow of $165 billion in 2013 to a net outflow of $143 billion in 2014; and then although that net outflow slowed to just $2 billion in 2015, other net investment flows swung from a $72 billion inflow in 2013 to a net outflow of $279 billion in 2014 and then $434 billion in 2015. The renminbi fell by almost 6% against the US dollar during this period – but would almost certainly have fallen by a lot more had the People’s Bank of China not spent nearly US$500 billion of its foreign exchange reserves supporting the currency (intervention which was accompanied by other forms of ‘suasion’ that are more readily available to the ‘Chinese authorities’ than to their counterparts in most other countries).

In one sense China is more vulnerable to such developments now than it was then, because (as shown in Chart 1) the ‘overhang’ of domestic money relative to the stock of foreign exchange reserves is so much greater than at that time. As an IMF Working Paper published in March 2019 noted, “a large pool of [renminbi]-denominated savings is held by residents … and there are insufficient domestic assets in which to invest … Chinese residents’ demand for foreign assets is suppressed by [capital controls] and even a small fraction of households switching to foreign assets could lead to sizeable capital outflows”. This paper also noted that “residents exhibit herding behaviour in response to shocks” and that “Chinese residents are not used to regular two-way movements in the exchange rate and hence their expectations are more sensitive to signals of change”.

An increase in the demand for foreign assets could be prompted by any one or more of a number of factors, but prominent among them might be a deterioration in the credit quality of banks (who are directly or indirectly the repository of most Chinese residents’ savings).

Officially, that’s not a problem: the most recent Supervisory Statistics of the Banking and Insurance Sectors put the non-performing loan ratio of the commercial banks at 1.59% at the end of 2023, the lowest in nine years. But, as _The Economist_ reported recently, a new banking regulator, the National Administration of Financial Regulation appears to be taking a tougher line with banks seeking, as they have typically done, to conceal their bad loans in ‘asset management companies’ which purchase impaired assets from banks using loans provided by the same banks. Since it was established in May last year, the NAFR has fined more than 20 banks (including one of the ‘big five’, the Agricultural Bank of China) for improper handling of bad loans. Given the ongoing deterioration in China's property development sector, now into its fourth year, further revelations of loan losses seem extremely likely.

In the event that the revelation of large loan losses at Chinese banks resulted in depositors seeking to withdraw their savings en masse, the authorities could draw upon the People’s Bank of China’s still-substantial pile of reserves in order to recapitalise the banks, as they have done on previous occasions (in the late 1990s, and again in 2006).

But there are two important points to note about the efficacy of such a strategy in contemporary circumstances.

First, the PBoC’s reserves are much smaller relative to the size of China’s banking system than they were on those earlier occasions when they were called upon to assist with the recapitalisation task. As of February 2024, the PBoC’s reserves were equivalent to just over 1% of total bank deposits, compared with around 2½% at the time of China’s last financial crisis in 2015, and 3½% in 2006.

Second, large as the PBoC’s reserves are in absolute terms (at almost US$3½ trillion), each US dollar that is used to recapitalise banks is a dollar that can’t be used to support the renminbi in the face of large capital outflows, if they were to eventuate. The Chinese authorities could be forced to choose between supporting the banking system and supporting the currency – in which case the first would likely take precedence.

To be sure, China is not in the same position as Thailand, Indonesia, Korea, Malaysia and the Philippines were in the lead-up to the Asian financial crisis of 1996-97. It hasn’t been running large current account deficits, and financing them with borrowings in foreign currencies by banks or corporates. According to China’s State Administration of Foreign Exchange, 47% of China’s external debt at the end of 2023 was in foreign currencies, amounting to the equivalent of 10% of China’s GDP. And, as noted earlier, that’s more than outweighed by China’s external assets.

But as Japan experienced in 1998 (when the Japanese stock market fell by almost 25% in six months, and the yen dropped by some 15% against the US dollar), creditor nations can also experience financial crises. It’s not a foregone conclusion, but the probability of China experiencing some form of banking and currency crisis in the next five or so years isn’t zero, and it’s rising.