, which was published by the Australian Government under the CC-BY-4.0 licence on the web page https://www.transparency.gov.au/annual-reports/department-prime-minister-and-cabinet/reporting-year/2021-22-10 (copyright info), CC BY 4.0, https://commons.wikimedia.org/w/index.php?curid=118269502")

Labor’s tax plan fails low paid workers

January 30, 2024

The Albanese Government was right to change its previous position on the already legislated Stage 3 tax cuts and to seek a fairer and more equitable taxation system for all Australians. However, its proposed changes fail to deal sufficiently with the increasing tax bites into the incomes of low paid working Australians. The focus on middle Australia has diverted attention away from those who have traditionally looked to Labor to represent their interests.

On 25 January 2024, the Prime Minister, Anthony Albanese, announced the Government’s proposed amendments to the income tax package which was originally enacted under a Federal Coalition Government in 2019.

Despite earlier statements to the contrary, by both the Prime Minister and the Treasurer, the Government has moved away from a tax package that, most notably, would deliver tax cuts of up to $9,075 per year to high income earners in 2024-25 in its Stage 3 tranche of benefits.

The Government has now proposed reducing the tax cuts for high income earners in order to provide tax cuts for low and middle income taxpayers.

The Coalition went to the 2019 election with a three-stage tax policy: Stage 1 picked up and added to the tax changes of 2018-19 and was proposed to have immediate effect, Stage 2 would apply from July 2022, and Stage 3 would commence in the 2024-25 tax year. With its re-election on 18 May 2019, the Coalition was able to pass the enabling legislation later in 2019. To abandon or modify the Stage 3 tax changes will require legislative intervention.

We should be clear about the intention and effect of this three-stage tax package. The Coalition’s tax package was intended to change the distribution of income tax burdens on Australian taxpayers, with tax hikes for low income taxpayers, especially low paid workers, and tax cuts for high income taxpayers. It has had that effect.

The modus operandi of those who want to flatten our progressive income tax system is to give short term tax cuts to the low paid, the “sugar hit”, followed by permanent tax cuts for higher income earners, and then to campaign on the immediate benefits of the package. The Republicans did it in the U.S. in 2017 and in Australia it started with the Coalition’s pre-election Budget in April 2019. Stages 1 and 2 of the tax package provided the sugar hit through short term tax cuts.

Too often it is assumed that Stages 1 and 2 of the tax package have already delivered tax cuts to the low paid. But, as we see below, this is a serious error because those tax cuts were temporary and did not protect workers against bracket creep.

The Labor Government’s recent response proposes a re-balancing of the income tax burdens across the community, but it still leaves substantial tax hikes for the low paid and locks in a system that accepts the basic orientation of the Coalition’s tax package.

This paper takes as its reference point the relative income tax bites across various low to high income levels over the period 2009-10 to 2013-14. These five years represent the implementation of the Rudd and Gillard Governments tax reform measures following the May 2008 Budget that, among other objectives, sought to provide support for the living standards of low income Australians. They followed a cut in the top marginal tax rate, from 47% to 45%, introduced by the previous Coalition Government for the 2006-07 tax year.

It may be argued that the respective taxation levels in those five years, are not immutable and that we should be prepared to consider their re-alignment. However, that needs to come with a broader debate that we have not had and, in any event, for a Labor Government, consistency with previous Labor tax policies should be the reference point for current income taxation policies.

The income tax rates that were set over the five years 2009-10 to 2013-14 were set with the intention of providing meaningful income support for low income earners. The turning point for low income workers can be found in the Coalition’s controversial Budget of May 2014. Successive Budgets and the Coalition’s 2019 tax changes have reversed the earlier Labor initiatives.

The unfairness of the income tax packages, as already legislated and as proposed by Labor for amendment, is most evident in the treatment of low paid workers, such as: a full time cleaner on the lowest minimum award rate in the Cleaning Services Award; a full time worker on the lowest minimum award rate for a trade-qualified worker; and a part time worker earning half the wage of the full time trade qualified worker.

By way of comparison with these low income taxpayers, we might consider the middle and high income taxpayers at various multiples of the incomes of the cleaner: two, three, four, five and ten times the income of the cleaner.

Stage 3 of the income tax package will operate from the 2024-25 tax year. From July 2024 the minimum wage rates to which I have referred will be adjusted by the Fair Work Commission, following its annual wage review. In the following sections it is assumed that a 4% increase will be awarded, an increase that is likely to be around the inflation rate since the Commission’s 2023 decision. Another percentage would increase or reduce the tax bites described, but they would be marginal by reference to the tax bite changes since the earlier reference period.

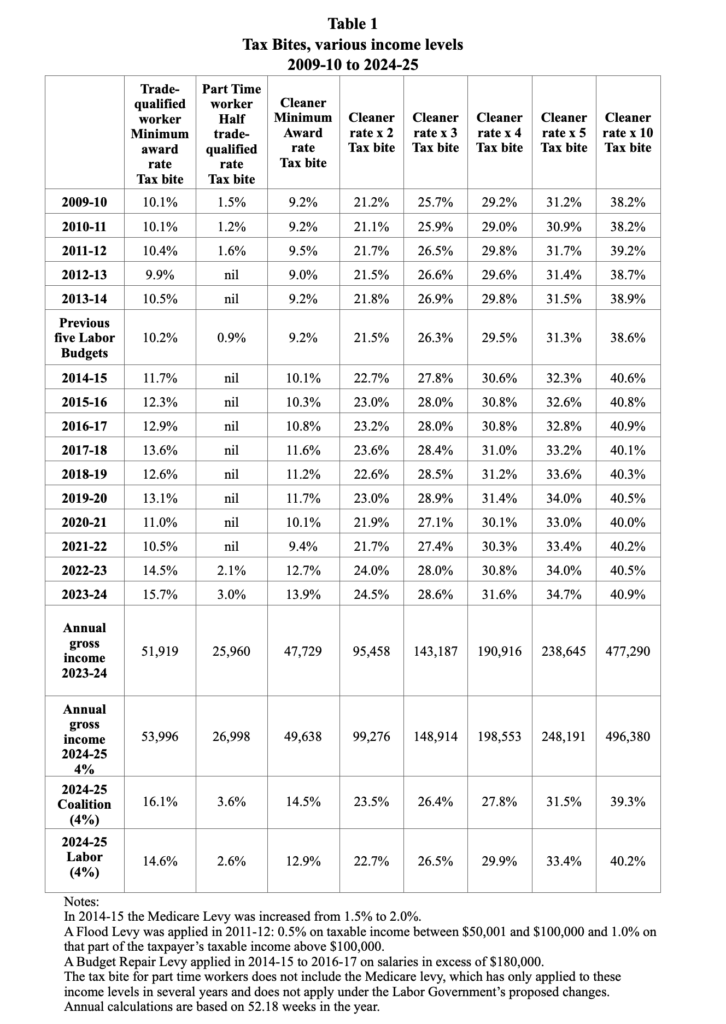

Table 1 sets out the tax bites of these various income groups over the fifteen years 2009-10 to 2024-25, together with some further relevant information. I have described in some detail the basis for this kind of analysis and the relevant data in a December 2023 briefing paper for Catholic Social Services Victoria, arguing that the tax package provides tax cuts for the rich and tax hikes for the poor.

The last two rows of Table 1 provide illustrations of the differences between the Coalition’s enacted legislation and the Labor Government’s proposals. As widely reported, the point at which Labor’s proposals become less advantageous to taxpayers is at $146,400 per year.

For the low paid workers in Table 1, the Labor proposals will deliver substantial benefits compared to those already enacted. The trade-qualified (or equivalent) worker, the lowest paid cleaner, and the worker on double the rate of that cleaner, would each receive $15.41 per week under Labor’s proposed changes.

Having regard to the changes in the tax bites over the past decade these tax cuts are fully justified.

Yet, we can see from Table 1 that more changes are needed if low paid workers are to recover the tax benefits lost during the past decade.

In order to better compare the tax bites over the years we should take into account the fact that the Medicare levy increase, from 1.5% to 2.0% in 2014-15, increased the tax bite. As it was a policy-based decision it should be excluded from calculations of tax bites based on bracket creep, and on the departure of Labor’s current proposals from the income tax policies of the Rudd and Gillard Governments.

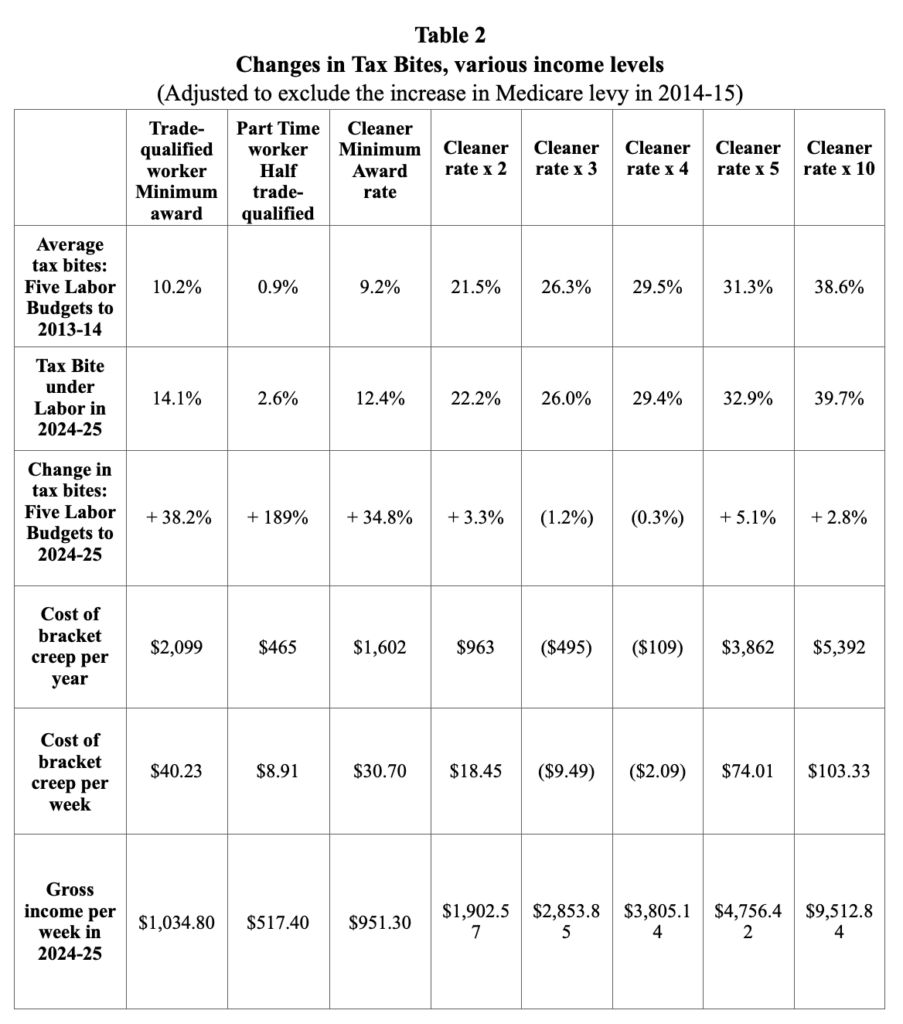

Table 2 enables a comparison between the income tax legacy of those earlier years and Labor’s proposed modifications to a decade of tax changes by successive Coalition Governments.

Table 2 demonstrates the substantial losses that low paid to middle income workers have suffered as a result of bracket creep, even after Labor’s current proposals for the tax system.

The trade-qualified worker would still be $40.23 per week worse off as a result of bracket creep since 2013-14. The cleaner on the lowest award rate for that occupation would $30.70 per week worse off. These are substantial amounts for low paid workers, especially when seen in comparison with the Government’s proposals that would deliver tax cuts of $15.41 per week in 2024-25 (on the assumption of a 4% increase in award wages).

The loss suffered by the part time worker as set out in Table 2 tells only part of the story. For the decade from 2012-13 this worker paid no income tax, but under Labor’s proposal this worker would pay $13.45 per week in income tax.

The worker on double the wage of the cleaner would be $18.45 per week worse off as a result of bracket creep, but in a relatively better position than the lower paid workers. It represents 1.0% of gross income.

Table 2 demonstrates that taxpayers receiving three or four times the cleaner’s wage (at $148,914 and $198,552, respectively per year) are treated very differently to low paid workers. Under Labor’s proposals they are not prejudiced by bracket creep since the earlier five-year period.

Taxpayers on five and ten times the cleaner’s wage are prejudiced by bracket creep under Labor’s proposals. However, for the taxpayer at five times the cleaner’s wage the shortfall is only 1.6% of total income and for the taxpayer at ten times the cleaner’s wage the shortfall is 1.1%. These are small relative losses compared to those facing low income workers.

Conclusion

This analysis is based on an assessment of the income tax regime introduced by the Rudd and Gillard Governments. There can be debate about the precise levels of the starting points for the analysis of bracket creep and the extent of the departure from the equitable distribution of income tax burdens envisaged by those Governments. However, any differences will be marginal; and we have to do the best we can in calculating the impact that bracket creep has had on taxpayers over the last decade or so.

Changes in income tax rates over the decade 2014-15 to 2024-25 have negated the very substantial tax legacy of the Rudd and Gillard Governments.

It is clear, however, that the Labor Government is not fully addressing the impact that bracket creep has had on low paid workers. On 26 January 2024, the Treasurer claimed in a press conference “We are returning bracket creep where it matters most and where it hurts the most, which is in middle Australia.”

But this middle Australia is not low income Australia, where bracket creep has reduced living standards, where the Government’s response is lacking, and where the tax bite on low incomes will continue to grow. The tax bite on the cleaner’s income in 2024-25 is estimated to be 12.9%. If that income increases by 10% over the following three years, for example, we know, using the ATO’s tax calculator, that the tax bite will increase to 14.0%. The inequity of the past decade will become baked in unless the situation is exposed and some action is taken.

The impact that increasing tax bites have had on the living standards of the low paid have been ignored in the legislative changes of the past decade, save for the sugar hits to which I referred to earlier. They were short term changes designed to sell a tax package that would, over time, bring about a substantial change in the level of income tax paid by low paid workers and other low income taxpayers.

It is also clear, that the Government is now intent on shoring up the arguments for its current proposals and does not want to advocate any further changes. Having stated until very recently that the Stage 3 changes would be left untouched, it might have exhausted its political capital. It is unlikely to admit that more is needed to help the low paid.

What can be done? The Government needs the support of the Senate for these changes. The Greens, at least, are against the changes because they do not go far enough in re-balancing the interests of low and high income taxpayers.

Re-balancing becomes difficult if it involves changes to taxation thresholds and marginal tax rates, both of which are in the Labor proposals.

An appropriate amendment to target the situation of the low paid would be an increase in Low Income Tax Offset (LITO). LITO and the Low and Middle Income Tax Offset (LMITO) were used from 2018-19 to 2021-2 to deliver the temporary tax cuts described earlier. Their impact on tax bites can be seen in Table 1. LMITO was abandoned at the end of 2021-22. Under Stage 3, LITO, at $700 per year, is to be phased out over incomes to $66,666 per year. In 2024-25, with a 4% increase in wages, the trade-qualified worker would receive offsets of $190.06, and the cleaner $255.43.

In 2021-22 LITO provided a maximum of $700 per year while LMITO provided a maximum of $675 per year for annual incomes up to $48,000 and a maximum of $1,500 per year for incomes over $48,000 per year. If these tax offsets we were to apply in 2024-25, the trade-qualified worker would receive a tax offset of $1,690.06 per year, or $32.39 per week, and the cleaner would receive $1,755.43 per year, or $33.64 per week. One option for assisting the low paid would be to combine similar payments into a revised LITO, with the maximum amount being phased out over incomes to, perhaps, $100,000.

Obviously, this kind of change would come at a very considerable cost and consideration would need to be given to its phased introduction.

The research and the debate needed for this kind of change can only occur if there is a better understanding of the economic circumstances of low paid workers and their families and of the impact that increasing tax bites have had on them. The Government must play an active role in this process.

The Albanese Government was right to change its previous position on the already legislated Stage 3 tax cuts and to seek a fairer and more equitable taxation system for all Australians. However, its proposed changes fail to deal sufficiently with the increasing tax bites into the incomes of low paid working Australians and with the deleterious effects that those changes have had on their living standards. Unless further changes are made to support the low paid through the income taxation system the valuable taxation legacies of the Rudd and Gillard Governments in support of low income earners will be lost.