Market hits record high

October 1, 2024

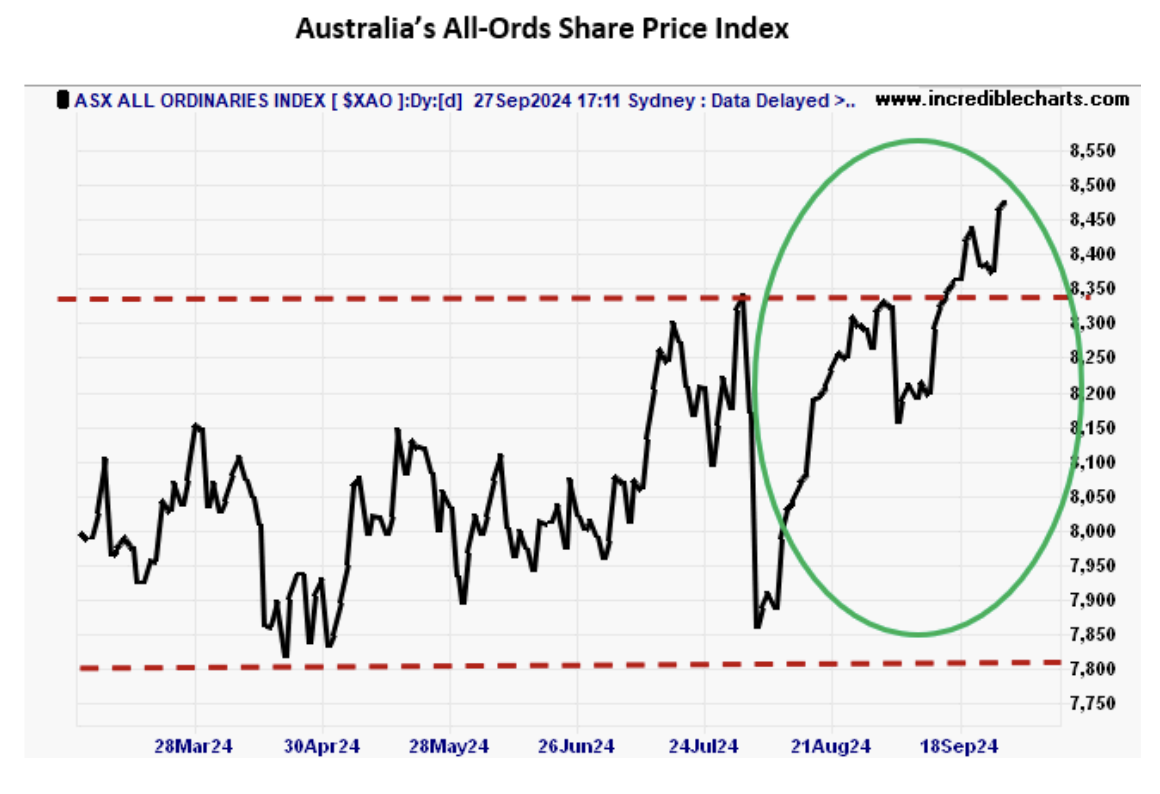

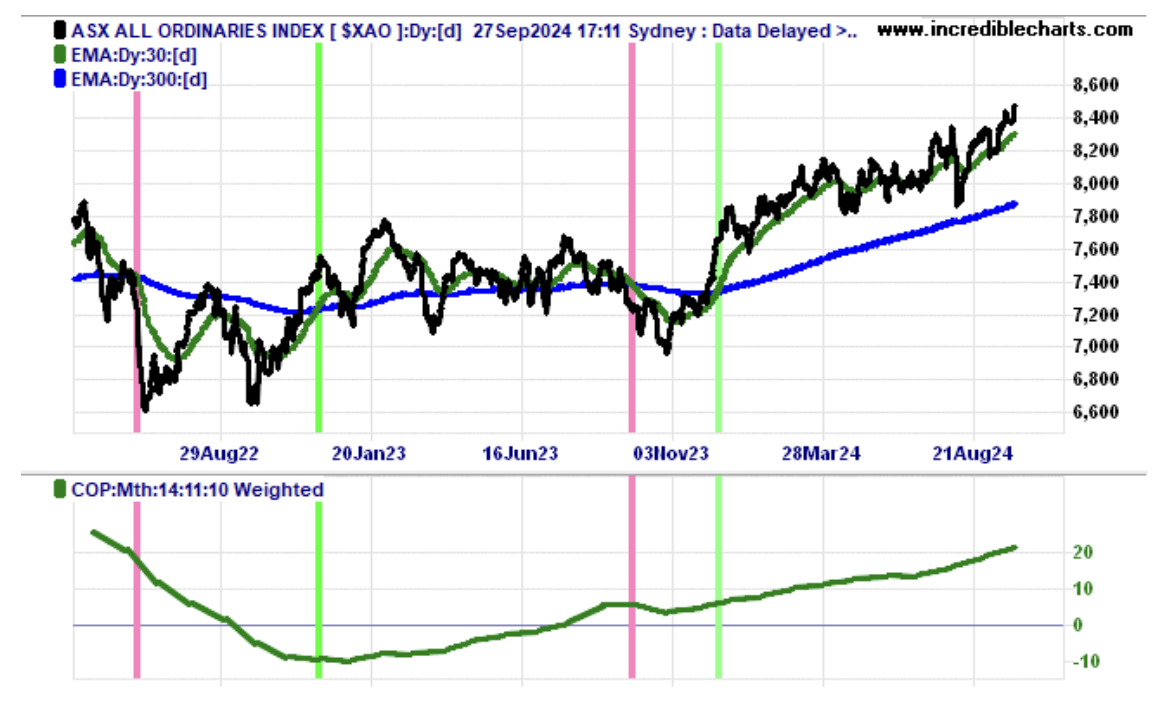

The All-Ords was in a sideways trading range between early February and early August and then dived. Since then, it has not only rebounded but escaped its former range ceiling and is now trading at a record high.

Seasonal Share Pattern

According to Shane Oliver, Head of Investment Strategy and Chief Economist at AMP Capital Investors:

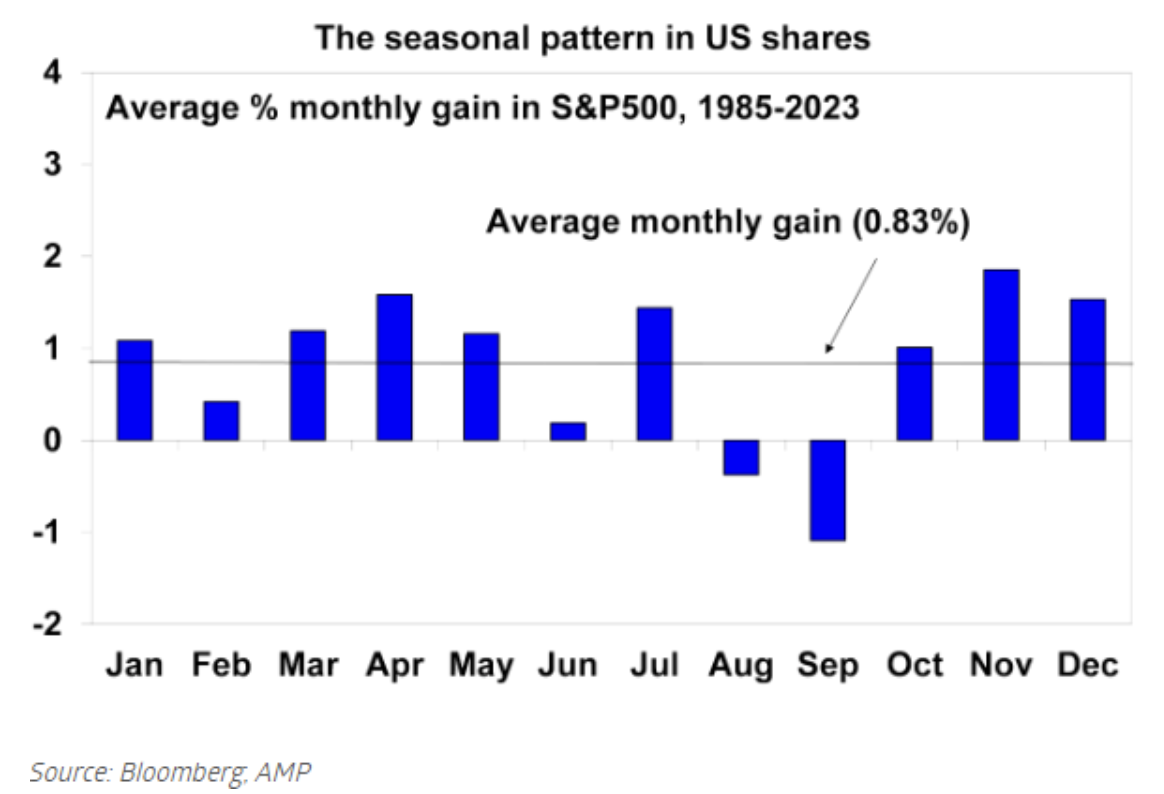

“The ‘seasonality’ of sharemarkets can provide useful insights, but monthly patterns in shares are far from foolproof.

• Historically, US shares have performed better from October to May each year, although the pattern is changing.

• Sharemarket seasonality is due to ebbs and flows in demand for shares at different times for the year, such as the New Year and in June.

• Investors should not rely on sharemarket seasonality as a basis to invest.”

He goes onto say:

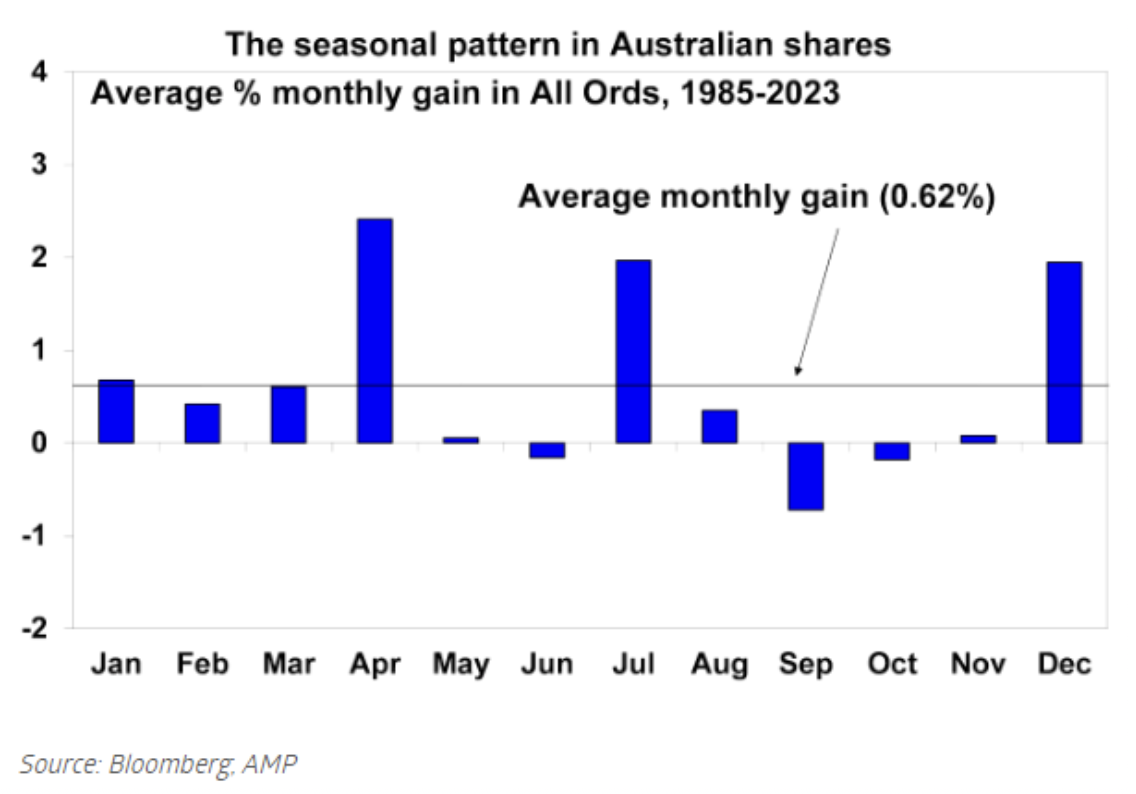

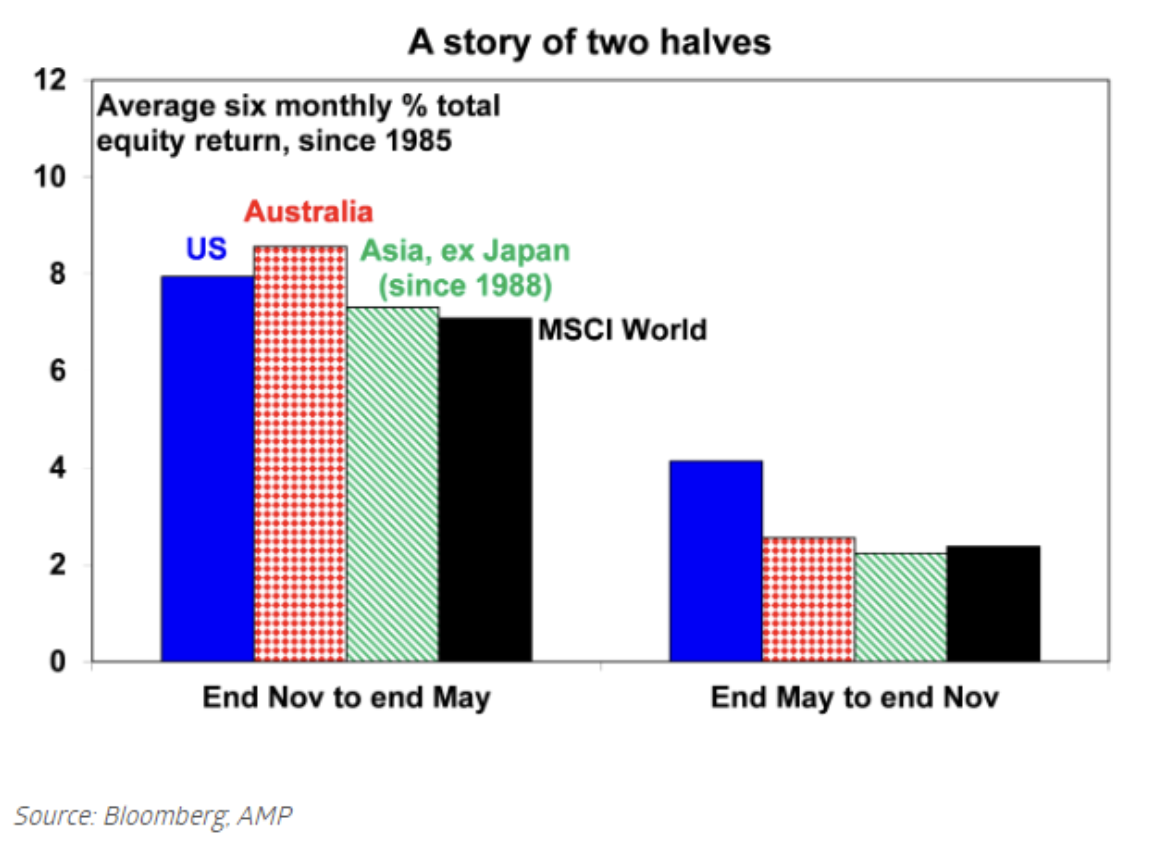

“Consistent with the influence of US shares on global shares, this seasonal pattern is also discernible in other countries. The seasonal pattern for the Australian stock market is shown in the next chart. In the Australian market, April, July, and December have tended to be the strongest months of the year, according to AMP analysis.”

Sell in May and go away until St Leger’s Day

According to Shane:

“As a result of these monthly trends identified above, AMP’s experience is that a typical pattern through the year has been for stocks to strengthen from around October/November until around May (or July in Australia’s case) of the next year and they have then tended to weaken into September.

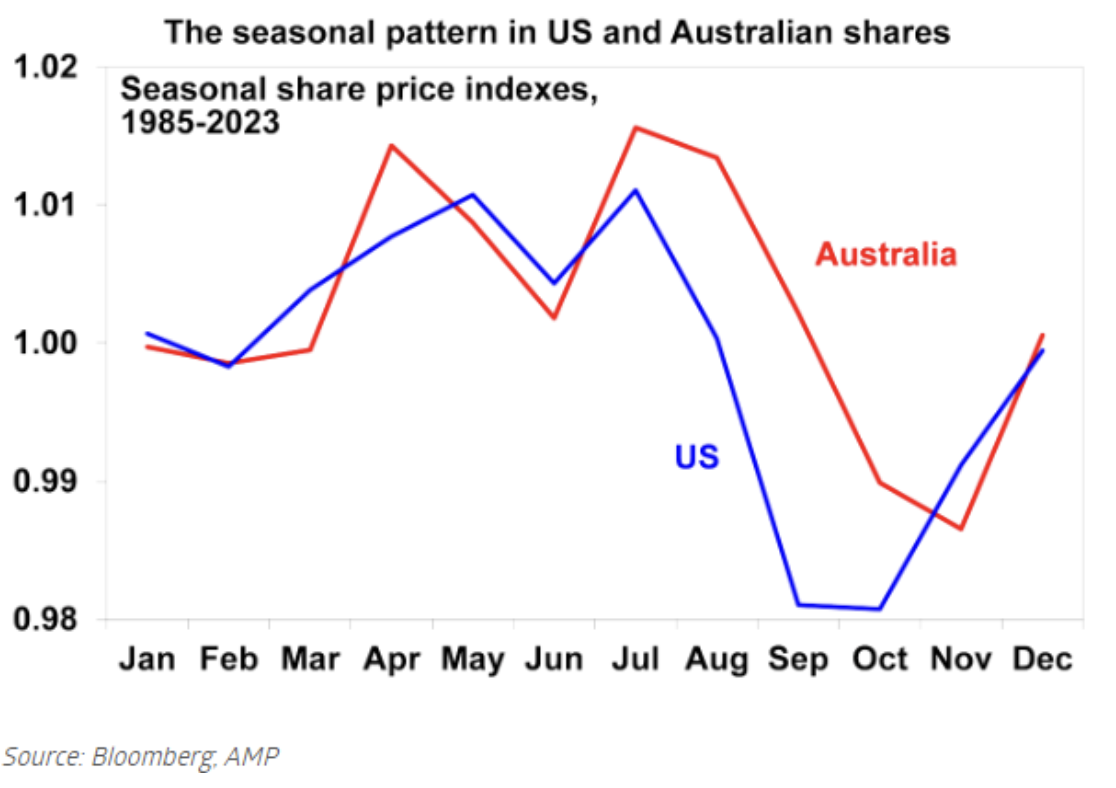

This seasonal pattern can be seen in the following chart which shows an index for US and Australian shares and the historical month-to-month pattern of share prices after the longer-term fundamentally driven trend has been removed.”

“Breaking the year into two six-month periods also reflects this historic pattern. Since 1985, the average total return (i.e., from price gains and dividends) from US shares from end November to end May has been 90% more than from end May to end November. Globally and in Australia and Asia it has been three or more times bigger, according to AMP analysis.

“While the US influence may play a role in the continuation of this seasonal pattern in shares, the old saying in its full form of “sell in May and go away, buy again on St Leger’s Day” has its origins in the UK as St Leger’s Day is a UK horse race in September.”

“So, seasonal patterns have weakened slightly over time. Seasonal influences can also be overwhelmed when contrary fundamental influences [such as market or company factors] are strong, so they don’t apply in all years.

Seasonal patterns certainly shouldn’t dominate an investor’s strategy. However, they nevertheless provide a reasonable guide to the monthly rhythm of markets that investors should ideally be aware of.”

For Shane Oliver’s full analysis visit the ASX site.

Market Drivers

For a concise analysis of what drove the previous week’s global and local financial markets read the “Bassanese Bites” column each Monday.

It is written by David Bassanese, Chief Economist, BetaShares.

Trend Analysis

Australia’s Market

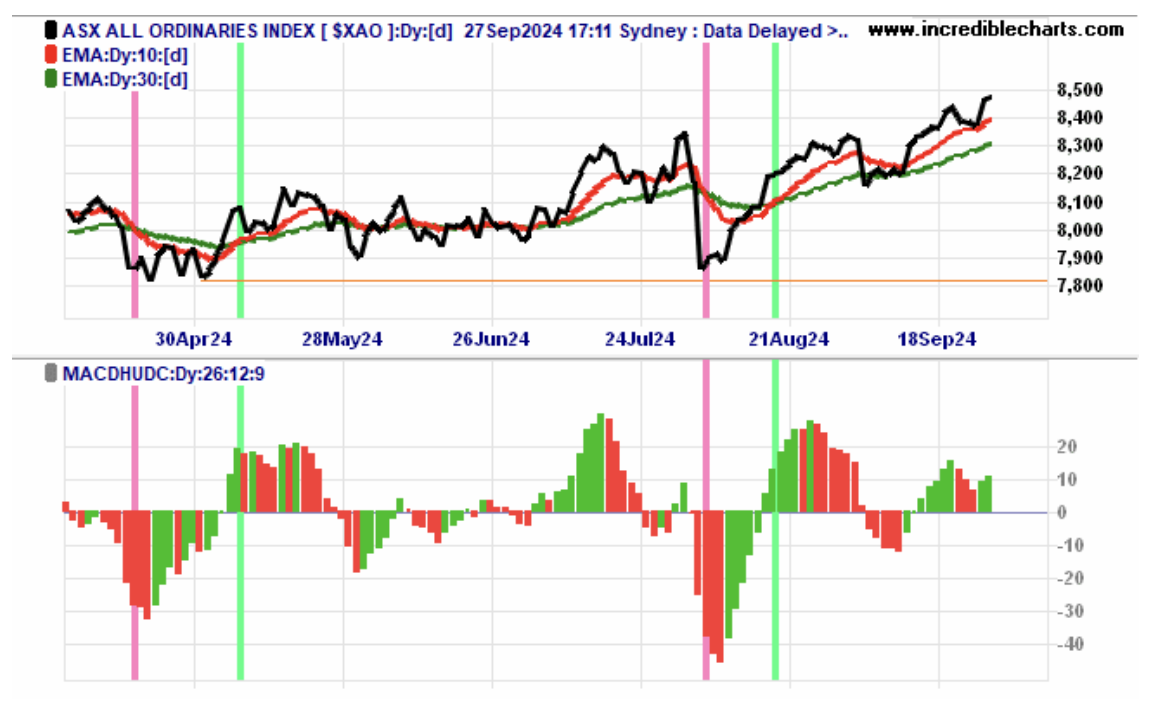

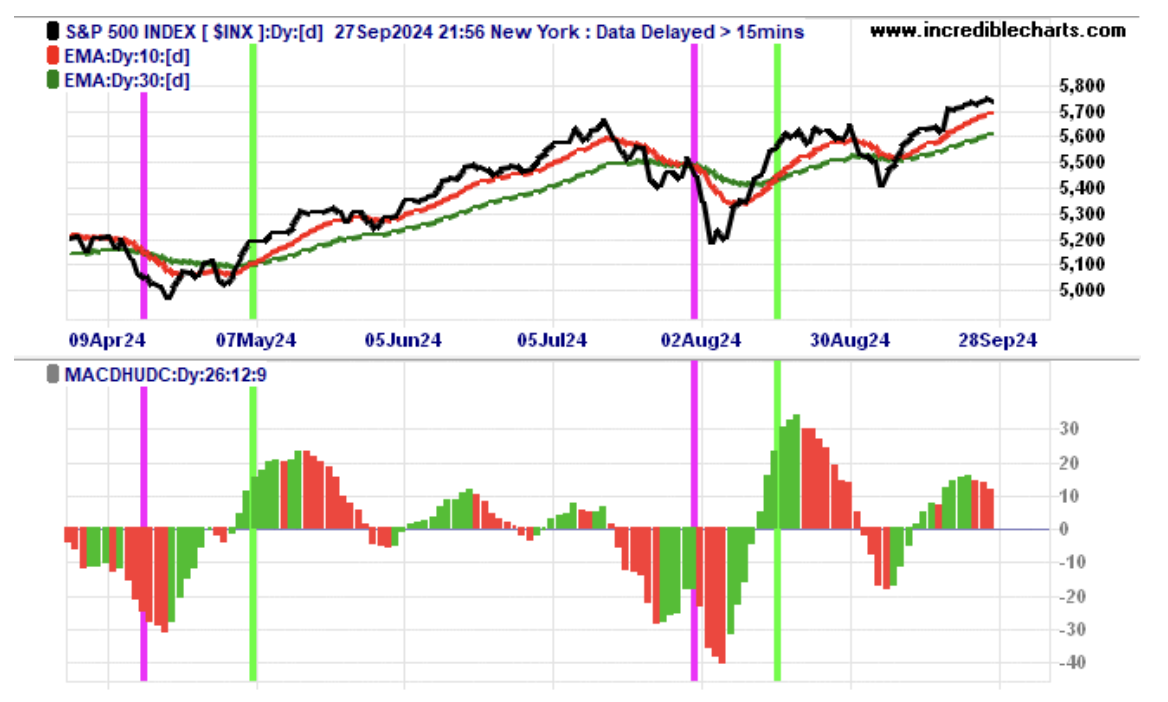

Short-to-medium-term trend analysis shows the All-Ords index went bearish on 6 August when its red 10-day trend line plunging below its green 30-day one. It then went bullish again on the 19 August and has remained so. The All-Ords price momentum as measured by the MACD has been positive for the past eleven trading days. See Chart below.

The All-Ords dark green Coppock (COP) momentum indicator bottomed at the end of December 2022 and thereafter trended up into positive territory where it has advanced following some hesitation in September – October 2023.

In the past whenever the Coppock turned up in negative territory it signalled the end of an Australian bear market. Only end of month readings are meaningful since the Coppock is a monthly based index.

America’s Market

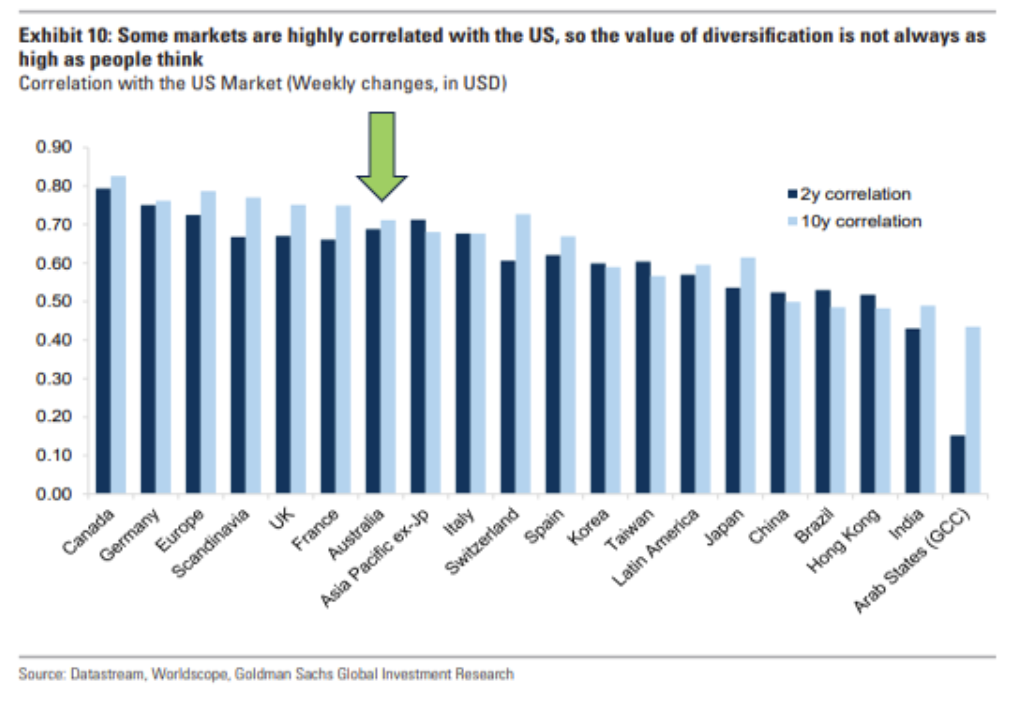

The Australian All-Ords index is highly correlated to the American S&P 500 index as shown by the following chart. About 70% of the All-Ords movements mirror the S&P500, meaning only 30% are caused by local or foreign events not impacting the USA. Hence the importance of tracking what is happening on Wall Street’s stock exchange.

Its MACD momentum indicator has been positive for the past eleven trading days.

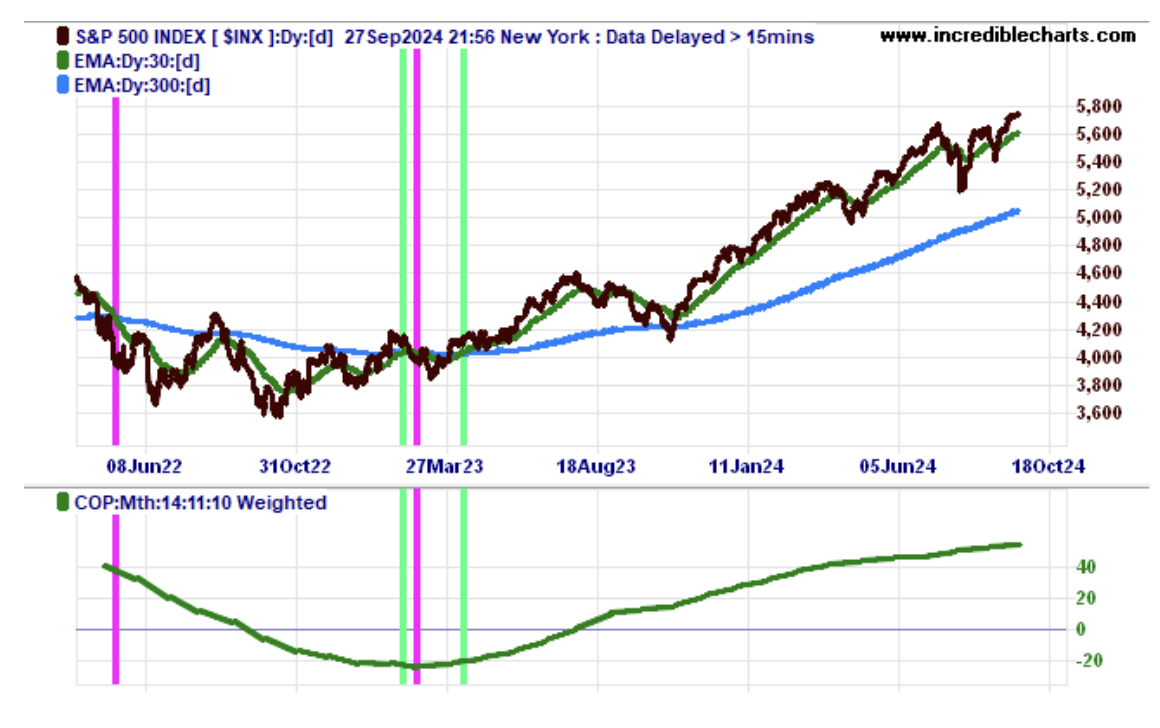

The dark green S&P 500 Coppock (COP) momentum indicator turned up at the end of March 2023 and thereafter has continued rising and remains strongly positive.

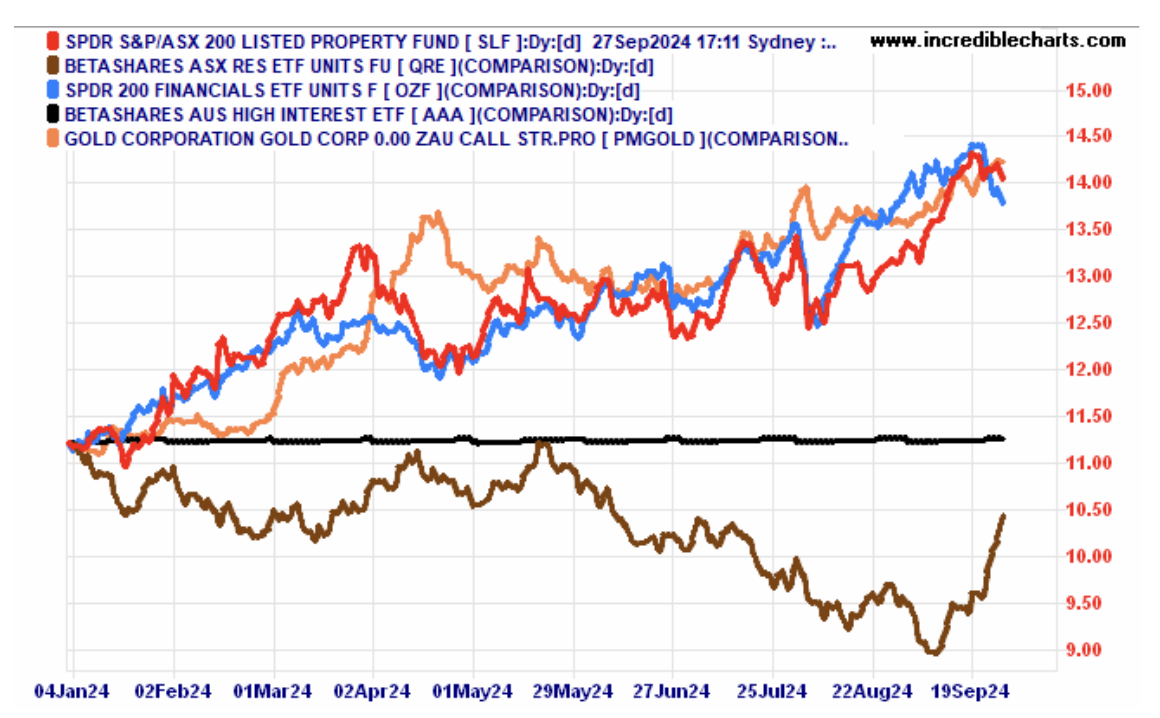

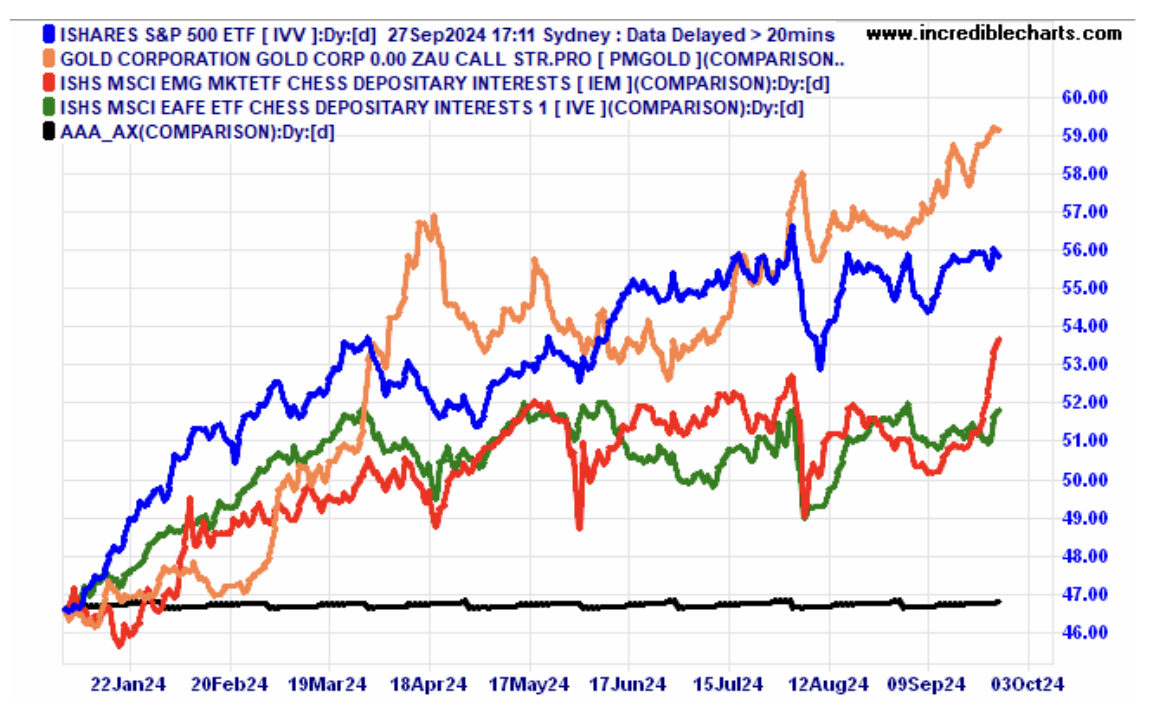

Each month I produce “Rotation” charts showing how a selection of ASX-listed local and global sector funds have performed relative to each other over the previous nine months. This period is widely used for gauging an asset class’s medium-term price momentum. Here are the latest results for the nine months to now.

The black straight line in each chart represents Cash (AAA.ax) whose price is unmoved by market sentiment. Note that Gold (PMGOLD.ax) is a defensive asset that tends to rise when equities fall. For this reason, gold along with cash and investment grade bonds reduces downside risk in investment portfolios.

Local Assets

Within Australia, all sectors except Resources (QRE.ax) remain positive with Gold (PM GOLD.ax) marginally overtaking Property (SLF.ax) and Finance (OZF.ax).

Resources were worn down by China’s collapsed property and infrastructure sectors and the West’s efforts to block its exports and hinder its technological progress. If America and its allies succeed in hobbling China’s economic ambitions, it will be bad for Australia because it is our biggest export market by far.

Recent efforts by China’s central bank and government to stimulate its moribund economy has given hope to our resources sector which is now rebounding though is still in negative price momentum over the medium term.

Global Assets

Globally, all sectors remain positive with Gold (PM GOLD.ax) overtaking the US Market (IVV.ax) followed by Emerging Markets (IEM.ax) with Developed Markets outside the USA (IVE.ax) last.

Economists keep predicting that US investors will rotate out of overvalued US stocks to better value non-US stocks, but that has still to happen. Analysts are also saying the disparity between growth and value stock and large and small cap stocks is at an extreme suggesting smart money will move to value and small cap stocks. There are signs that this rotation has begun.

What my models say

I do not forecast markets because soothsayers normally get it wrong. Nor do I give investment advice. Instead, I gauge the market’s present trend and momentum to let it speak for himself.

My technical models show:

- On short-to-medium-term trend analysis both the Australia’s All-Ords index and America’s S&P 500 index are bullish again.

- On medium-to-long-term trend analysis both the Australian and US markets remain bullish.

- The Coppock momentum indicators of both markets are positive. They turned up in negative territory early last year signalling the previous bear market was over.

- Using comparative momentum analysis of five major asset classes locally and the same number globally, the finance sector is doing best in Australia and gold bullion is the best performer internationally.

As always this is market analysis, not forecasting let alone trading or investment advice. Market pullbacks are stock price index falls of up to 10% and corrections are falls of between 10% and 20% from a market peak. A crash is when the fall exceeds 20%.