MICHAEL KEATING. Retirement Incomes Review: Part 2

December 2, 2019

The Governments independent Review of the retirement incomes system has identified four criteria against which that system should be judged: adequacy, equity, sustainability and cohesion. Yesterday I reviewed the performance of the Australian retirement income system against the criteria of adequacy. This article completes the review against the other three criteria.

Equity

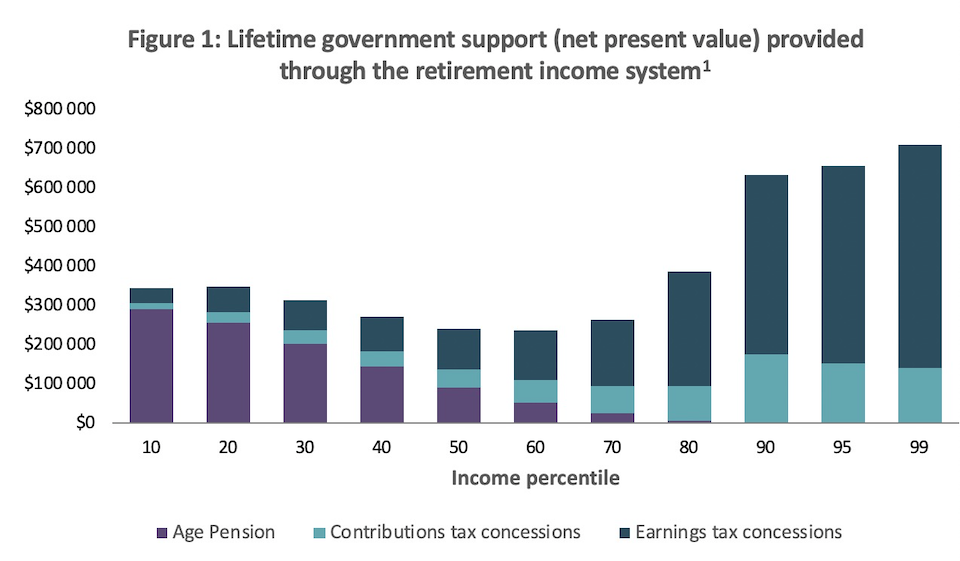

The chart below, from the Reviews Consultation paper, purports to show the income support provided by the government over each recipients lifetime for each decile of retirees. As can be seen that assistance is fairly evenly spread across the first four quintiles in the income distribution, but the upper income quintile, and especially the top decile, are shown as getting distinctly more government assistance.

As can also be seen, the flat-rate, means-tested age pension is the reason for the even distribution of government support across the first four quintiles of the income distribution.

In fact, Australias pension system is exceptionally highly targeted. Australia spends twelve times as much on the poorest 20 per cent of the population as on the richest, a ratio close to six times the OECD average, and Australia redistributes more to low income retirees than any other country.

On the other hand, as is shown in the chart, it is often objected that the assistance provided through the tax system to superannuation saving unfairly favours high income earners. However, the estimate of this tax assistance in the chart is based on a comparison with the tax people would have paid if their superannuation contributions and the earnings on their superannuation savings had been taxed at their full marginal income tax rate.

In recent years the Government has moved to cap the amounts of superannuation that can attract a lower rate of tax, and this has significantly limited the assistance to people with the greatest superannuation balances and/or the amounts that they can contribute at a lower rate of tax. A further tightening of such limits would be possible if it were desired to reduce the tax concessions to these high-income people.

However, it is arguable that it would be better if superannuation were taxed not when it is being accumulated, but when it is being drawn down in retirement or on death. If the tax concessions are measured against such an expenditure benchmark, then other modelling suggests that they would be about the same value across the income distribution and are not unfair.

In short, it is debatable whether any further changes should be made to the taxation of superannuation contributions and earnings pre-retirement in Australia.

It is, however, arguable that there is another major inequity in Australias retirement income system because of the exclusion of the value of the of the retirees home when applying the age-pension means-test. The home is often the most valuable asset, and as noted in yesterdays article there is a considerable difference in the adequacy of retirement incomes depending on whether or not the retiree owns their home.

On the other hand, nonhome owners can have around $210,000 more in assets than a home owner before their pension is affected by the assets means test, in recognition that they do not benefit from the exemption of the family home from the assets test. They may also be eligible for Commonwealth Rent Assistance.

Nevertheless, the Grattan Institute has argued that the equity of Australias retirement income system would be further improved if the pension means-test were amended to incorporate the value of any home above a threshold of, say, $500,000.

Such a change might also reduce the present disincentive for retirees to downsize because the transfer of real estate assets for additional financial assets can reduce their net incomes under the present pension means-test. In that case, reducing any present disincentive to downsizing by retirees could then benefit both them and the community.

Sustainability

In Australia general taxation funds a flat-rate, means-tested age pension. As a consequence, in 2015 its cost at 4.3 per cent of GDP was less than for almost any other advanced western democracy, and not much more than half the average OECD cost in 2015 of 8 per cent.

There is also less risk of a blow-out in Australian superannuation costs, as Australias superannuation is an accumulation system. By comparison, in many other countries, their retirement incomes systems pay a defined-benefit that represents a fixed proportion of the retirees pre-retirement income, and is fully indexed thereafter.

This means that in other countries, employers and/or the government bear all the financial risks if pensions have to rise to maintain these defined benefits. That is the main reason why the sustainability of other countries retirement income systems is often doubted. Whereas in Australia, all these financial risks relating to superannuation savings are borne by the individual beneficiary, and the cost of superannuation is fixed at the contribution rate and cannot blow-out.

There are also concerns about the risks to the Australian Governments budget from an ageing population. According to the ABS mid projection, over the next eleven years, the proportion of people aged 65 and over will increase by 2.7 percentage points from 17.8 per cent to 20.5 per cent in 2030.

However, offsetting this increase in the number of aged Australians is the fact that they are working longer. In addition, the proportion of full age pensioners is also declining; falling over the last twenty years from over 80 per cent to around 68 per cent.

On balance, the Parliamentary Budget Office projects that spending on the age pension will not increase but will remain steady at 2.4 per cent of GDP over the next decade.

In sum, I think that Australias retirement income system is eminently sustainable. The understandable fears in many other countries about the future sustainability of their retirement income systems are misplaced here.

Cohesion

The principle concern about the cohesion of the retirement incomes system is whether the various forms of withdrawal of assistance and their interaction with the tax system might create unacceptable disincentives to work and/or save for retirement.

Although such disincentives are theoretically possible, my reading of the empirical literature is that they are not significant, or least not sufficiently important to outweigh the other advantages of means testing.

Conclusion

In my view there is not a lot that needs changing in Australias retirement incomes system.

The key priorities for the Review are to:

- Consider whether or not present policies will lead to Australia achieving the 70 per cent replacement income benchmark for most retirees,

- Consider ways to improve the availability and take-up of annuities by retirees, and

- Support a substantial increase in rental assistance.

There are also some equity issues relating to the taxation of superannuation contributions and earnings, and whether homes should be included in the age pension means test. I have argued that these concerns are debateable, and it would be useful for the Review to consider them further.

Beyond these key issues, however, I doubt that there is a case for much change. Australias retirement income system, unlike that of many other countries, looks to eminently sustainable financially. Nor is there a problem with the cohesion of the system.

As the Reviews Consultation paper demonstrates, Australias retirement incomes system is different from all other countries, and I would argue that it is distinctly better.

Footnote

1 Calculations assume that individuals commence work in 2018-19 at age 27 and work until age 67, with a predicted life expectancy of 92. Accumulated superannuation benefits are invested in an account based pension and individuals are assumed to draw down their assets at current age based minimum drawdown rates. The level of tax assistance and Age Pension entitlements are discounted by nominal gross domestic product (around 5 per cent per annum) to give a net present value in 2018-19 dollars. Annual incomes are calculated for each percentile based on the distribution of earners at each single year of age. Assumes no non-concessional contributions.

Michael Keating is a former Head of the Departments of Prime Minister & Cabinet, Finance, and Employment & Industrial Relations. He is presently a Visiting Fellow at the Australian National University.