MICHAEL LAMBERT. We know about the Grants Commission but what is this thing called HFE?

April 18, 2018

You may have noticed recent press reports of some angry Premiers or Treasurers bemoaning the loss of revenue in the triannual carve up of the GST pie among the States and Territories while the winners kept their pleasure to themselves. Welcome to the wonderful world of HFE, horizontal fiscal equalisation as practised in Australia.

Like most countries, Australia has a system of allocating revenue amongst regions to try and achieve equity. In unitary Governments, this is often undertaken informally through additional payments directed at poorer regions while in federations, with national and regional governments, it is done more formally. Australia has the most formal and complete system of HFE across all federations. Also, not entirely unrelated Australia has the most significant level of VFI or Vertical Fiscal Imbalance amongst the world’s federations. VFI is an imbalance between the national and regional governments in revenue and expenditure powers. The Commonwealth raises 74% of total government revenue and spends 55% of total government expenditure while broadly the States and Territories spend 45% of total government expenditure and only raise 26% of total government revenue. This results in the Commonwealth making payments to the States and Territories to supplement their own source revenues.

Australia has an independent Commonwealth body, The Grants Commission, which assesses on a rolling three-year basis how the GST revenue, that is on-passed to the States and Territories, is distributed. The principle that underpins this distribution process is a principle of fiscal equalisation which states that each State and Territory should be placed in a position where they have the fiscal capacity to provide the same services at the same standard and at the same level of effort to raise their own source revenue and operate at the same level of efficiency. In order to assess this, the Commission assesses all revenue and expenditure of States and Territories, including all Commonwealth grants (other than a small number that are excluded from the process). The Commission takes into account any disabilities that a State may have that increase the cost of service delivery such as sparse population and diseconomies of small-scale or increase the per capita demand for services, such as a large indigenous or aged population. On the revenue, side adjustments are made for any disabilities that deflate the revenue base such as low property values. Once these disability adjusted revenues and expenditure have been calculated the distribution of GST is calculated (called the relativities) such that every State and Territory is placed in the position of equal fiscal capability. This means in theory that the benefits that a large state like NSW has with large cities and population, high property values and economies of scale in the delivery of government services that impact on higher per capita revenue and lower per capita expenditure than the national average are removed through a reduced share of GST revenue.

A key principle underlying this approach is what is termed policy neutrality which means that States and Territories should not be disadvantaged by making a higher than average revenue effort such as setting a higher tax rate or conversely advantaged by making a lower revenue effort or required to provide the same standard of services as other jurisdictions.

While most federation have some form of fiscal adjustment between States, it is not as comprehensive as practised in Australia. First, it is normal to only take account of disabilities on the revenue side, not the expenditure side. Second, Australia sets a high standard for equalising the States and Territories. It uses the standard of bringing all States and Territories to the fiscal capacity of the fiscally strongest State. That traditionally has been either NSW or Victoria but since the mining boom, it has been Western Australia. The distribution of GST is shown in the table below for 2017-18. You can see that for that year NSW received 87.7% of its population share, Western Australia received only 34.4% of its population share and at the other extreme the Northern Territory received 466% of its population share. In that year there were three what are colloquially termed donor States and five what have historically been termed claimant States and Territories. In total NSW, Victoria and Western Australia had $7.9billion of their per capita share of GST transferred to the other states and territories in order that all States and Territories are placed in the same position of fiscal capacity as Western Australia. Thus about 13% of the GST revenue is used to fiscally equalise amongst the States and Territories.

Table 1.1 2017-18 GST distribution

Relativities | Population share (per cent) | GST distributiona ($m) | GST share (per cent) | Equal per capita distribution ($m) | Difference from equal per capita distribution ($m) | |

NSW | 0.877 | 32.1 | 17 680 | 28.2 | 20 111 | -2 431 |

Vic | 0.932 | 25.3 | 14 829 | 23.6 | 15 862 | -1 033 |

Qld | 1.188 | 20.0 | 14 963 | 23.8 | 12 565 | 2 398 |

WA | 0.344 | 10.9 | 2 354 | 3.8 | 6 818 | -4 464 |

SA | 1.440 | 7.0 | 6 360 | 10.1 | 4 405 | 1 955 |

Tas | 1.805 | 2.1 | 2 403 | 3.8 | 1 328 | 1 075 |

ACT | 1.195 | 1.6 | 1 230 | 2.0 | 1 026 | 204 |

NT | 4.660 | 1.0 | 2 921 | 4.7 | 625 | 2 296 |

Total | 1.000 | 100.0 | 62 740b | 100.0 | 62 740b | na |

A State’s GST distribution is calculated according to the equation: AGSTRi=GS×(PifiPifi) where AGSTRi denotes assessed GST revenue for State i_, GS is the total pool of GST revenue, Pi is the population of State_ i and fi is the relativity for State i. b Forecast.

Source: CGC (2017a, 2017h, p. 2, 2017j).

The history of the arrangement is interesting. When the federation was established in 1901 there was not a formal mechanism in place like now but an expectation by the smaller States that they would be fairly treated. As a result, the Commonwealth made grants to try to provide reasonable equity between the States. After Western Australia voted to secede from the Federation by a two thirds majority, the Commonwealth established the Grants Commission in 1933 as a way of placating Western Australia which was seeking special assistance because of what it claimed was a lower capacity to raise revenue than other states and higher costs because of a small population dispersed over a large area and a relatively large indigenous population. Initially, the process involved select States and Territories been able to apply to be considered as claimants who were then assessed by the Commission which could recommend financial assistance be paid. This assistance was paid by the Commonwealth. In the late 1970s, when I joined the NSW Treasury, the Commonwealth had the inspiration to change the rules of the game from that of the Commonwealth paying for the equalisation payments to making the States and Territories themselves pay for it by establishing what is now a zero-sum game, that is the winners pay the losers. The first application of the new approach occurred in 1981. This led to an elaborate process of submissions by all States and Territories to the Commission and the Commission being conducted on inspections of State facilities. The inspections involved locating and escorting the Commission around the worst and most disadvantaged prisons, schools and hospitals. It was a fascinating if disturbing experience.

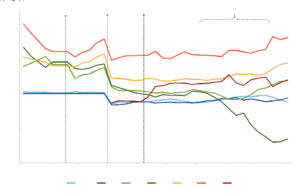

In 2000 the GST was introduced and allocated to the States and Territories with a corresponding reduction in Commonwealth payments to the States and Territories. Hence now the allocation of GST revenue formed the means for achieving fiscal equalisation. The history of the relativities is presented in the figure below, noting that a relativity of 1 means achieving your per capita share of GST while a relativity above 1 means getting more than your per capita share. NSW and Victoria have consistently got less than a per capita share, Queensland has dipped above and below the line, while Western Australia spectacularly went from being above to well below 1, setting the record for the lowest relativity at 0.34 in 2017-18. The Northern Territory, South Australia and Tasmania have continuously received well above per capita GST payments. The Northern Territory is not shown in the figure because its relativity is so much higher than the other jurisdictions, between 4 and 6, that is it gets between 4 and 6 times its per capita share of GST.

The relativities are reset on a rolling three-year basis and those for 2018-19 have being released. NSW has declined from 0.88 to 0.86, Victoria has gone from 0.93 to 0.99, a boost of $1.8billion per annum and Western Australia has increased from 0.34 to 0.47, a boost of $1billion per annum, the latter reflecting the lagged decline in mining revenue.

Despite Western Australia being the beneficiary of the system for decades and being compensated by the Commonwealth with infrastructure grants during the mining boom for its reduced relativity, it has persistently sought to have the system changed. Its preferred approach was to either exclude or discount the level of fiscal equalisation of mining revenue. In response in May 2017 the Commonwealth Treasurer issued a terms of reference to the Productivity Commission to undertake a review of HFE. This is the second review of the subject commissioned by a Commonwealth Treasurer in the last five years. The first was undertaken by the trio of Nick Greiner, John Brumby and Bruce Carter and issued a report in October 2012. The report supported the principle of fiscal equalisation as equitable but suggested that the level of vertical fiscal imbalance should be reduced so that the States and Territories could have a greater level of self-funding, that GST revenue be distributed on an equal per capita basis and that the Commonwealth provide top up funding to the weaker States and Territories. This was in some ways a return to the pre-1933 system. Not surprisingly the Commonwealth did not act on the report.

The Productivity Commission issued a draft report in October 2017 and will be presenting its final report in late May 2018, just after the Commonwealth budget. In summary the draft report concludes that:

- The fundamental principle of fiscal equalisation to achieve fiscal equity between the States and Territories is valid

- There is little evidence that fiscal equalisation has negative economic or efficiency effects though it can discourage major tax restructuring by the States and Territories

- The standard of equalising to that of the fiscally strongest State is excessive and it would be better to equalise to a suitable lower standard such as that of the average of States and Territories.

- The Commonwealth, in consultation with the States and Territories, should prepare a revised statement of the objectives of HFE and at the same time should seek to commence reforms of the federation, starter with greater clarity of the roles and responsibilities of the levels of government.

- The Grants Commission, in the meantime, should be directed to simplify and make more transparent the process of fiscal equalisation

- The Commonwealth should prepare clear guidelines for any exclusion of Commonwealth payments to the States and Territories from the equalisation process

Given the zero-sum nature of the equalisation process for the States and Territories and the lack of skin by the Commonwealth in the game it is extremely unlikely that there will be any meaningful reform to emerge, including the suggestion of a more fundamental look at reform of the federation.

Michael Lambert is a former Secretary of NSW Treasury, for his sins was involved in the HFE process and is a non-executive director and senior adviser on health economics at the Sax Institute.