Multinational tax integrity and tax avoidance by the fossil fuel industry: Part 1

November 16, 2022

This is the first instalment of a two-part series based on our recent submission to the Australian Government regarding tax transparency and the fossil fuel industry. The first part examines Australia’s global fossil fuel transnational corporations’ problems and tax practices. The second part provides recommendations for minimising their tax avoidance practices.

In Australia, the fossil fuel industry is big business. Between 2005 and 2020, Australian coal export revenues totalled more than $643 billion. Over the same period, gas exports generated $287 billion, and petroleum exports more than $166 billion. In 2021-22, Australia’s resources and energy export earnings surged to a record high of $425 billion and will be significantly higher next year due to current record prices for coal, oil and gas. Despite the eye-watering sums involved, most companies have been paying little or no income tax due to the cosy tax relationships these firms continue to enjoy with state and federal governments.

As a percentage of GDP, since the Federation, the mining and resources sectors have rarely contributed more than 10 per cent of total revenue, while the coal industry has rarely contributed more than 4 per cent. Currently, the coal industry directly employs around 37,000 people. The oil and gas industry currently contributes around 3 per cent of Australia’s GDP and around 13 per cent of total exports, directly employing about 17,000 people. Even though the Australian Resources and Energy Employer Association claims the Australian resources industry employs over 1 million people.

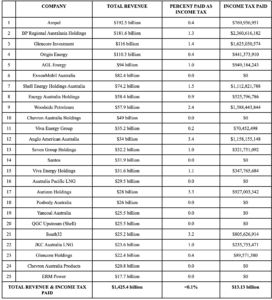

Given the enormous sums of money generated by the industry and the extent to which it engages in public relations messaging to Australians about its value to the country, most of us would imagine it is not being subsidised. Nothing could be further from the truth. The fossil fuel industry receives massive direct and indirect subsidies from Australian governments: more than $70 billion in direct subsidies alone between 2015 and 2021. As can be seen from the table below derived from Australian Tax Office data, this is more than five times the income tax revenue taken by the Federal Government from twenty-five fossil fuel and energy companies between 2013 and 2021, whose collective revenue was more than $1.4 trillion.

Estimates of the combined annual costs of fossil fuel subsidies and the negative social and environmental externalities produced by carbon pollution range from around $18 billion to $39 billion in current Australian dollars. Because the greenhouse gas emissions produced by Australia’s fossil export emissions are around three times higher than the country’s domestic emissions, totalling around 5.5 per cent of the annual global burden, the negative externalities produced by Australia’s fossil export emissions are also around three times higher. However, Australian governments refuse to commit to phasing out coal, oil and gas production and continue to approve massive coal and gas expansion projects that will further contribute to climate disruption.

Current levels of taxation and subsidies, combined with the social and environmental externalities of fossil fuel production and use, and the fact that the energy and resource companies involved are 86 per cent foreign-owned, undoubtedly demonstrate that the financial gains to the Australian people from the industry are not as significant as the industry and its political backers claim.

A recent Australian Treasury paper provides several examples of accounting and tax practices used to minimise or even eliminate the amount of corporate tax paid by fossil fuel transnationals in the Australian context. Many of these practices have been in place for decades, including:

- thin capitalisation rules and generous government deductions;

- corporations claiming massive payments for intangibles and royalties in foreign countries;

- corporations using accrual accounting techniques to minimise tax rates on profits;

- corporations shifting income to tax havens,

- corporate entities in one jurisdiction lending money at a higher interest rate to subsidiary entities operating in other jurisdictions (i.e. transfer pricing),

- corporations claiming inflated expenses in foreign countries (e.g. marketing, intellectual property and head office expenses).

The Australian Taxation Office (ATO) recently published the Corporate Tax Transparency Report (CTTR) for the 2020-2021 financial year. The report, published annually using income tax and Petroleum Resources Rent Tax data, stands out as one of the more transparent government tax documents.

However, these disclosures do nothing more than highlight the lack of tax paid by the vast majority of fossil fuel companies.

Twenty-five fossil fuel & energy companies not paying their fair share of tax, 2013-2021

Source: Australian Tax Office (3 November 2022)

Research conducted by Market Forces using publicly available ATO tax data has revealed that 73 of the 134 fossil fuel companies identified by the ATO in FY2021 paid no income tax, despite a total income of $164 billion in Australia. The table below provides details of the total revenue and income tax paid by twenty-five fossil fuel and energy companies between 2013 and 2021, based on ATO data. These twenty-five companies disclosed revenue of about $1,425 billion and paid an average of less than 1 per cent income tax on that revenue. Nine of those companies paid zero income tax over that period.

Australians have become increasingly aware of this issue. Nevertheless, how is it that transnational fossil fuel cartels have been enabled to engage in widespread tax avoidance while making super profits from public resources that belong to all Australians? Their ability to avoid paying income tax has been enabled by government legislation that: a) permits corporations to establish offshore tax havens into which they can funnel revenue, b) allows foreign-owned and located corporations to engage in transfer pricing to their Australian subsidiaries, and c) encourages the grandfathering of tax losses for an indefinite period.

One of the most significant areas in which transnational corporations have exercised influence over government regulation concerns national and sub-national tax systems. That influence has enabled a range of tax avoidance measures to flourish that cost the Australian Government tens of billions of dollars of tax revenue it could otherwise use for a wide range of practical social purposes.

A growing body of international research has documented how transnationals and their legal and accounting advisors engineer the law and regulatory structures to their advantage. Elected officials routinely support legislation that advantages the interests of business and industry over that of the general public. The primary ways business and industrial elites gain and maintain their influence over political and bureaucratic elites are through lobbying, political donations, and revolving door appointments between Government and industry.

Necessary prerequisites for minimising undue corporate influence are a government bureaucracy transparent to democratic scrutiny and elected officials who are prevented from forming self-interested relationships with business and industry. In the absence of wide-ranging integrity reforms, more piecemeal approaches focused on tax reform would go some way to redressing the current imbalances and improprieties in how tax is levied on fossil fuel transnationals.

What is of most concern is that the most significant enablers of global tax abuse are the rich countries at the heart of the global economy and their dependencies. It is not widely known that just four countries, i.e. the United Kingdom and its ‘independent’ territory of the Cayman Islands, the United States, Netherlands and Luxembourg, account for 47 per cent of countries’ tax losses, whereas lower-income countries are responsible for only 2 per cent.

It is, therefore, incumbent on the incoming Labor Government to begin the task of reforming Australia’s taxation system to prevent these kinds of abuses. It could begin by closing the many loopholes in how the Petroleum Resources Rent Tax is levied and asking two of its closest allies why it is that their governments not only tolerate but enable global tax avoidance

In the second part of this story, we will provide recommendations about how the Australian Government can minimise transnational corporations’ massive tax avoidance practices.