Private health insurance: and the rort goes on

October 10, 2023

Theres a government review of health insurance. Heres why you havent heard of it and what needs to change.

In the dying months of the Abbott-Turnbull-Morrison era, a set of research projects was commissioned from the consultancy firms favoured so highly by that government. The full cost is unclear, but its in excess of $5 million.

The job: to tell the government what it wanted to hear.

Private health insurance, said Tony Abbott, is in our DNA. The Liberals were never going to accept a review that said it was a bad idea, not worth the money, inequitable, inefficient. Its all those things, but dont expect to hear it from them.

Most of the money went to Finity Consulting, whose websitenotes that it works for 30 of the 35 health insurers in Australia. Our reputation is built on delivering timely, relevant and actionable insights, and advice to help our clients achieve their specific objectives, the website says.

This is not an independent, frank-and-fearless outfit. Its part of the industry these papers were supposed to investigate. As such, it was fully in tune with the Morrison governments aim to increase insurance uptake and to pivot the health system further toward the private sector. The same can be said of Ernst and Young, one of the Big Four consultancy firms that was contracted to produce one of the five reports involved.

The government could have contracted genuinely independent academic institutes to do this work, but that would have risked getting answers they didnt want.

Those papers landed on Greg Hunts desk shortly before the government in which he was Health Minister was booted out of office. The incoming Labor minister, Mark Butler, had to deal with them. As a minister in a government that doesnt want to spend money, major changes to hospital funding are not practical. But the ALP remains highly sceptical about the value of private insurance, so his options were limited. Binning the reports would upset the insurance lobby and Butler is not ready for a fight. So his options were limited.

The result was a short consultation period that few outside the industrys biggest players knew about. No submissions have appeared on the Health Departments website. The Australian Medical Association and the Australian Private Hospitals Association, have released theirs.

The reports looked at three main issues:

- The governments rebate on premiums;

- Lifetime Health Cover, which penalises people who dont join up when young;

- The Medicare Levy Surcharge, which makes higher-income earners pay more tax if they dont have health insurance.

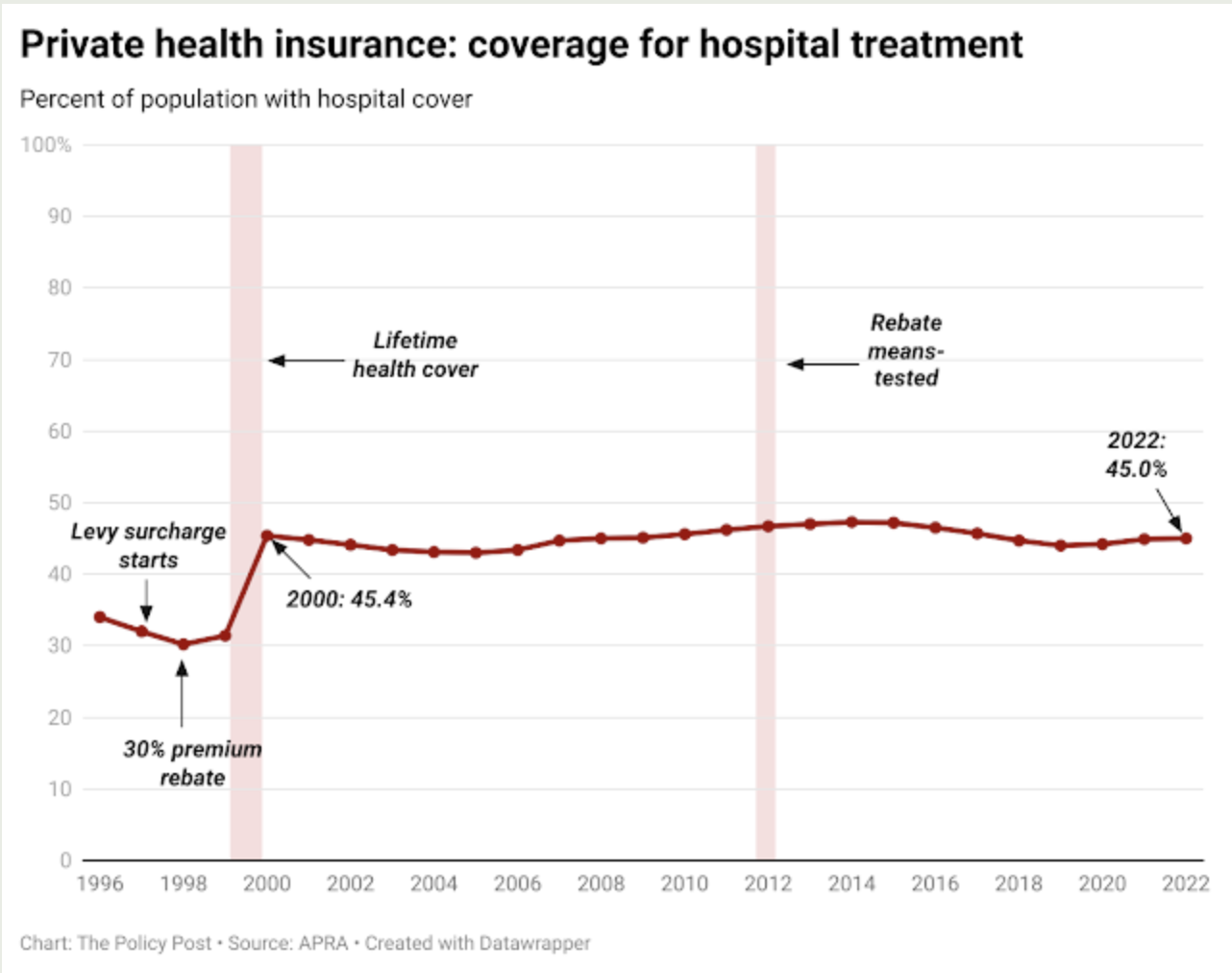

The Medicare Levy Surcharge was the first of three attempts by the Howard government and its health minister, Michael Wooldridge, to boost fund membership. Well get to that later, but it had no effect at all. Customers continued to drop out.

The second of these attempts the 30% subsidy for premiums now costs the federal government around $7 billion a year, about two-thirds of which goes to hospital policies. Though it has a questionable impact on fund membership it is understandably beloved by the insurance companies.

It was introduced in 1998 with almost no consultation outside the insurance industry. The government thought that if it paid 30% of everyones premiums, it would rescue private health insurance.

It didnt. Some decent research might have revealed that changes to premiums have relatively little effect on uptake: in economic language, health insurance is price inelastic. Despite committing their own and future governments to a large and growing outlay, that rebate made little difference. It wasnt until 2000 and the introduction of Lifetime Health Cover, which penalised people who didnt join up when they were young, that the decline was turned around.

Under this scheme, anyone taking up private health insurance would have to pay 2% more for every year they are aged over 30. So someone of 40 would pay 20% more, a 60-year-old would pay 40% more, and so on.

Enrolments rose sharply as people over 30 rushed to beat the deadline. But since then, there has been little change to overall membership, despite the growing cost of the failed but expensive rebate scheme.

But despite the punitive Lifetime Health Cover measure, there has been an unwanted and unexpected change to the overall age profile and therefore the risk profile of fund members. Right after the initial boost in 2000, young people started dropping out and older people started joining.

Another example of failure of Wooldridges policies is that when the Gillard government began means-testing the rebate in 2012, reducing the cost to the government from 30% to 25%, there was no discernible impact on membership.

A 2016 paper in the Australian and New Zealand Journal of Public Health explains why:

Price signals to patients are generally ineffective in addressing supplier-induced demand as they do not address the asymmetry of information between healthcare providers and patients, a fundamental feature which distinguishes healthcare from competitive markets with perfect information. Hence, patient price signals lead to under-servicing populations who cannot afford to maintain access while over-serving those who can.

Despite these failures, the insurers and their researchers continue to push it.

Removing the PHI rebate entirely would result in a worse overall outcome for the sustainability of Australias health system, says the Finity report on the subject

We estimate the short-term impact would be a 10% reduction in the number of people covered by PHI, and a reduction in hospital claims funded by PHI of $2.3bn-$3.1bn per year.

Given what the rebate costs, thats not much of an endorsement. The report then, without evidence, says this:

While this is lower than the annual PHI rebate of $4.8bn for hospital products, the longer-term impacts of removing the PHI rebate could be more significant, with the potential for a spiral of higher premiums followed by selective lapse and further premium increases, a scenario which is not consistent with a sustainable PHI industry.

Thats the health insurance industrys version of a doomsday scenario. But based on what?

There is no likelihood of any government getting rid of the rebate completely or in one big hit. And the report repeats another long-debunked claim:

The PHI rebate is small compared to the average hospital claims, which would need to be funded by the public health system if the individual decided not to insure.

But a mass of evidence from independent health economists refutes that. Astudy by the Centre for Health Economics Research and Evaluation at the University of Technology Sydney concluded:

While the insurance incentives substantially increased the proportion of the population with supplementary cover, the impact on use of the public system appears to be quite modest The insurance incentives appear to be an extremely costly way of reducing pressure on the public hospital system.

And the Melbourne Institute of Applied Economic and Social Research found the industry support policies the rebate and Lifetime Health Cover strongly favours the rich:

This paper finds significant evidence that the policy reform disproportionately favours high income earners. In particular, the 30% premium subsidy represents a windfall gain for households which would have purchased private health insurance even without the rebate. The amount of the gain is approximately $900 million per year, a large proportion of which would go to higher income households.

That calculation was made in 2006. In todays dollars, that windfall to people who would have bought insurance anyway amounts to $1.3 billion, or 20% of the annual cost of the scheme.

Nor have the various private insurance incentives made any significant difference to the workload of public hospitals. There are masses of studies showing the same thing, but one of the most recent again, from the Melbourne Institute showed that even a substantial increase in coverage makes a negligible difference to the pressure on public hospitals:

We found that increasing the average private health insurance take-up from 44% to 45% in Victoria would reduce waiting times in public hospitals by an average 0.34 days (or about eight hours).

This increase of one percentage point is equivalent to 65,000 more people in Victoria (based on 2018 population data) taking up (and using) private health insurance

There might be an argument for this public spending if the end result was to substantially take pressure off public hospitals and thereby reduce waiting times for treatment in public hospitals.

But the considerable effort it takes to encourage more people to sign up for private health insurance, coupled with the small effect on waiting lists weve shown, means this strategy is neither practical nor effective.

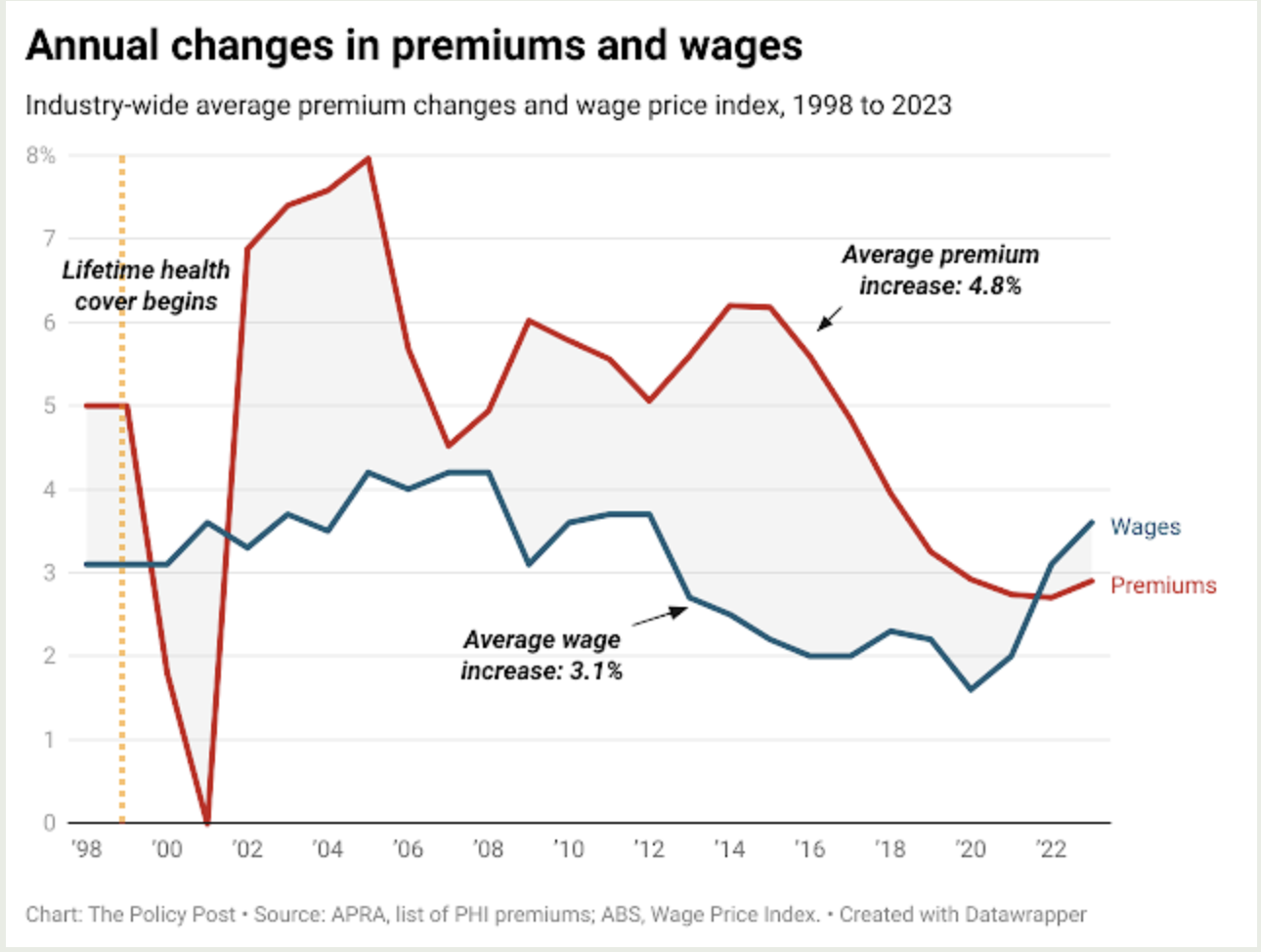

Despite the substantial government subsidies, the cost of premiums far outstrips wage growth. When the Lifetime Health Cover penalties were introduced, the Howard government promised that premium increases would come down. They did for a year. Then they went back up and stayed there.

Worsening affordability has two obvious effects: it favours those on higher incomes who can still afford those premiums; and it puts greater strain on the budgets of less-well-off households who dont believe they can rely on the ailing public system.

Meanwhile, the cost of the ineffective premium rebate continues to rise. According to the most recent federal budget, its now costing $7 billion a year and growing at around 4% a year.

That money would be enough to build half a dozen medium-sized public hospitals every year.

Tax cuts for the wealthy

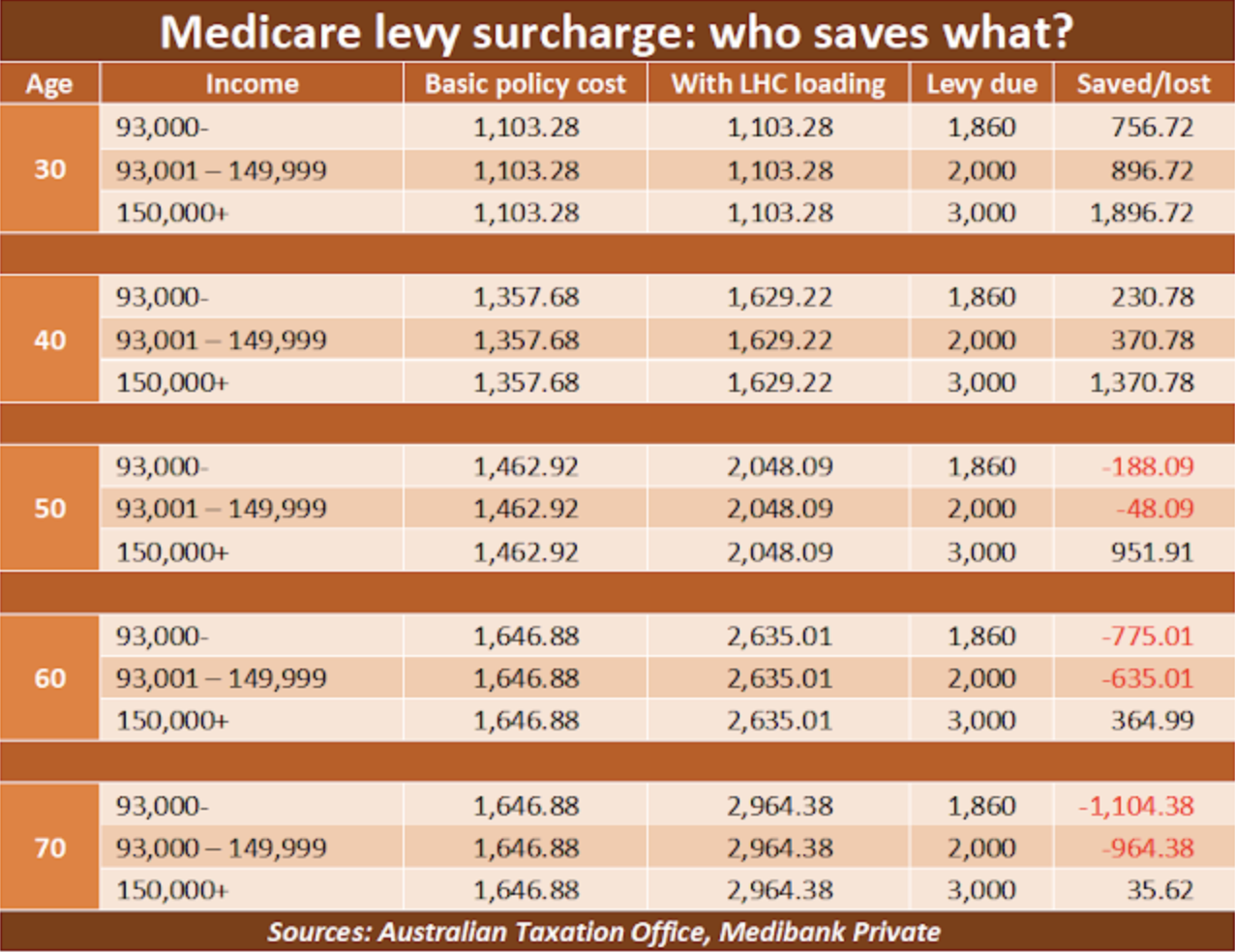

Another of Michael Wooldridges failed policies was the introduction of a new tax to force higher-income earners into buying health insurance. Effectively, it was a government subsidy.

This surcharge was the first of Wooldridges three efforts to boost fund membership. A new tax on high-income earners was introduced formally, a surcharge on top of the existing Medicare levy that would be waived if an approved private health insurance policy was bought.

In practice, its complicated. There are different outcomes according to age as well as income. But to explain, look in the table below at the figures for a 50-year-old individual. A typical basic policy (in this case from Medibank Private) would cost $1,462. But if theyre newly joining, the Lifetime Health Cover penalties mean that policy will cost them $2,048.09 instead. If that person earns over $150,000 a year, theyll be up for $3,000 in extra tax. But if they take out a basic policy, theyll save $951.91 a year.

If you look at the column on the far right, youll see that in every age group, this policy favours those on the highest incomes.

As weve seen, this measure had no discernible effect when it was introduced in 1997 but, like the subsidy for premiums, its still there. And still doing nothing partly because people on high incomes have probably got insurance anyway. The only effect of this measure is to give a windfall tax break to some of the richest people in Australia.

Greg Hunts Finity Consulting report swims against this tide of evidence. The levy surcharge works, they say. And it would work even better if it redirected some money from richer people to older people even though that would undermine Lifetime Health Cover, which makes premiums more expensive for older people. And it wants richer people to be required to buy more expensive policies to qualify for the exemption, making even more money for the insurers.

Right now, Australians and their national government pump over $27 billion a year into the private health insurance industry. Its worth asking where that money goes, and what value we get from it.

Give the job to Medicare

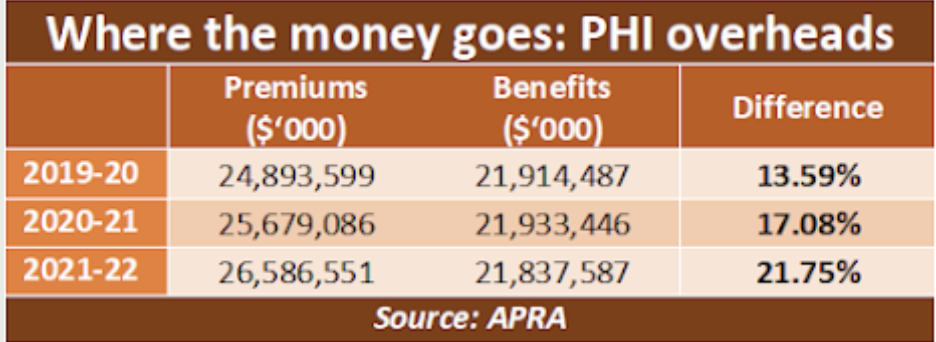

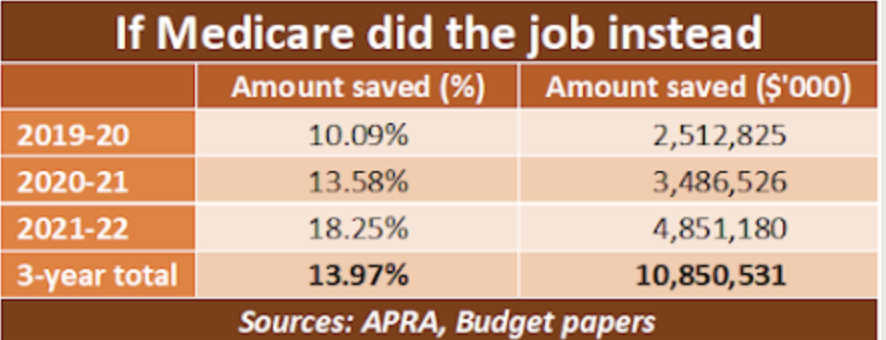

The main measure of the efficiency of any healthcare funding scheme is how much money goes to the actual delivery of care, and how much is lost to the ticket-clippers along the way. Medicare, the public insurer, provides a benchmark. In 2022-23, it got $28.25 billion from the government and paid out $27.32 billion in benefits. So administration costs took just 3.4% of its income.

With the commercial insurers, its a different story. The comparable figure was 13.59% in 2019-20, but this was boosted in the two following years by the pandemic. Fewer people were seeking care during the lockdowns but went on paying the premiums.

As corporations have evolved, their purpose has changed. The benefits of these big businesses have moved from customers and shareholders to managers and directors.

Increasing CEO pay is not actually linked to an increase in the value of CEOs work, found a report from the US-based Economic Policy Institute. Instead, it is more likely to reflect CEOs close ties with the corporate board members who set their pay.

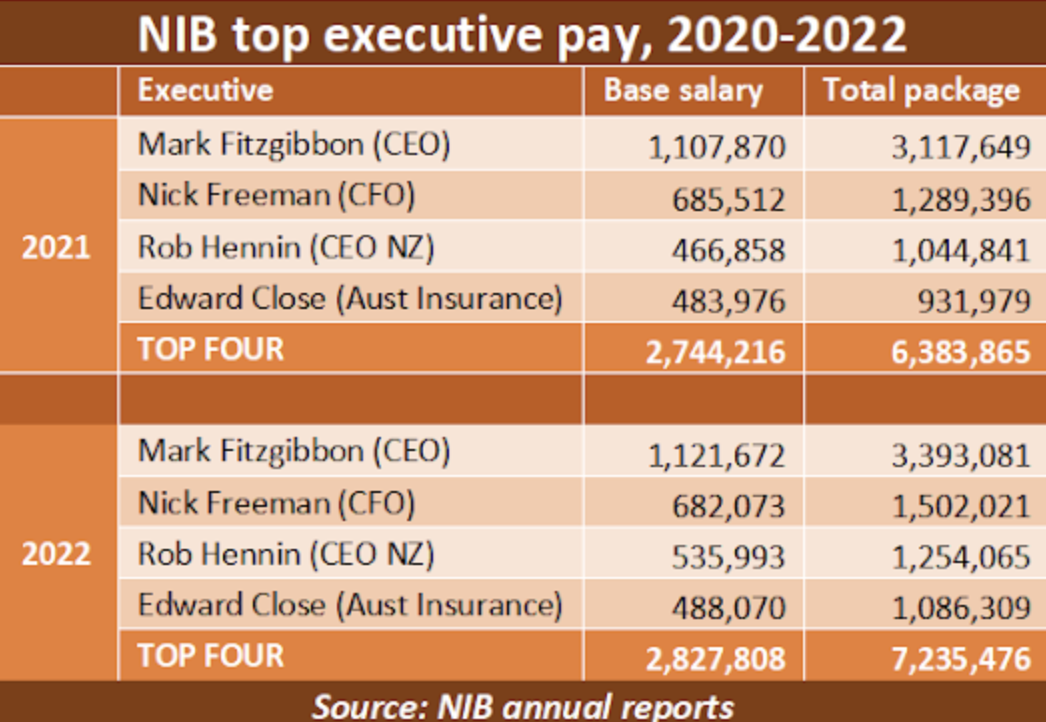

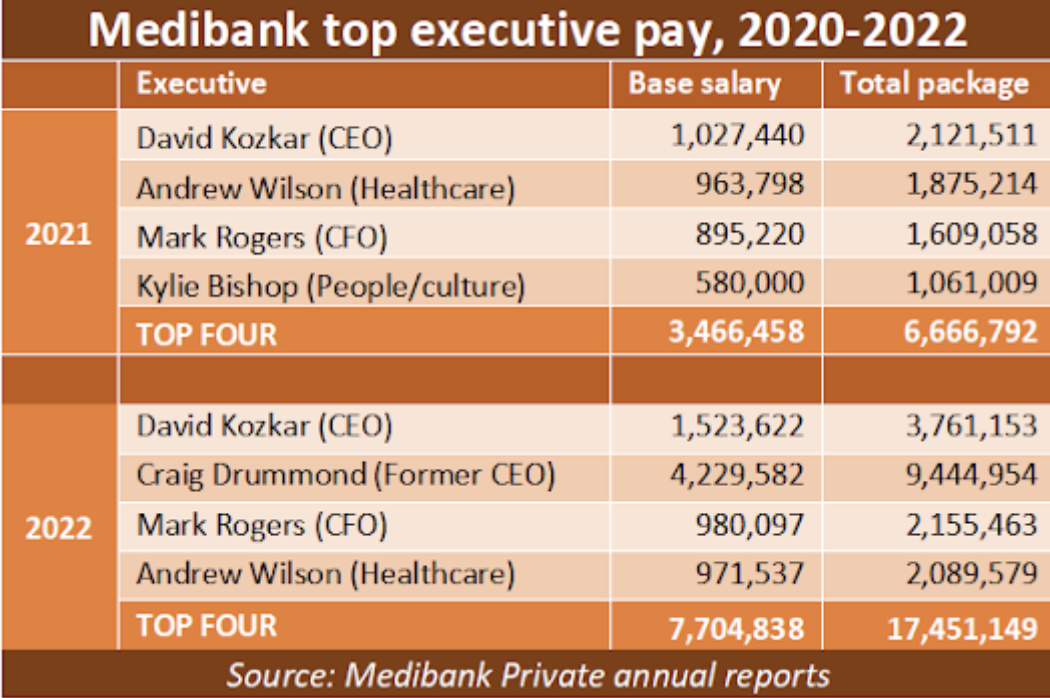

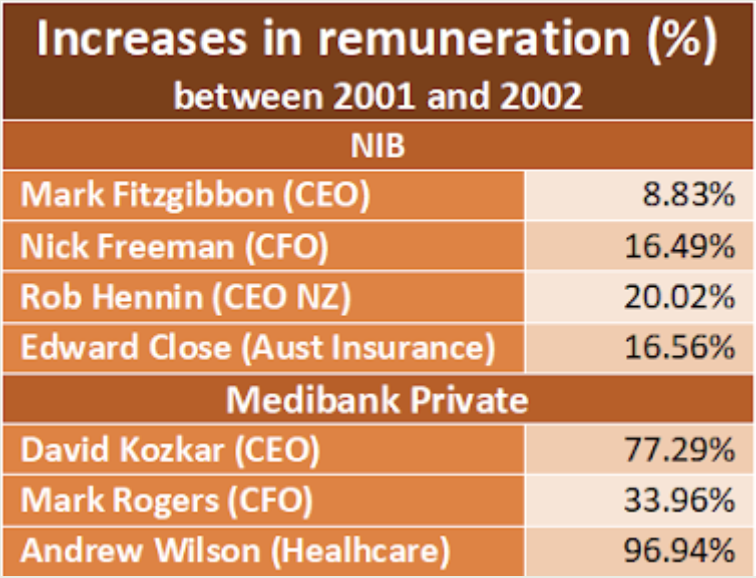

This global trend can be seen also in Australian private health insurance companies, such as NIB and Medibank Private. Top executives in these firms are earning well over $1 million a year each, and CEOs well over $3 million.

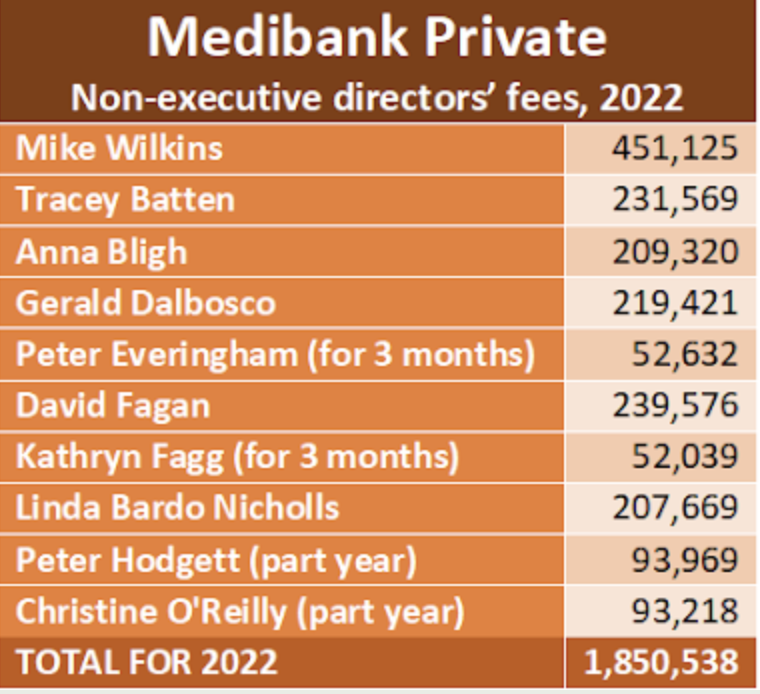

Much of their pay is linked to company profit and share price. During the pandemic, when premiums continued to be paid but when fewer people drew on their policies, profits soared. And though the executives did nothing to cause those windfalls, they benefited mightily. As this table shows, top executives at Medibank Private did particularly well.

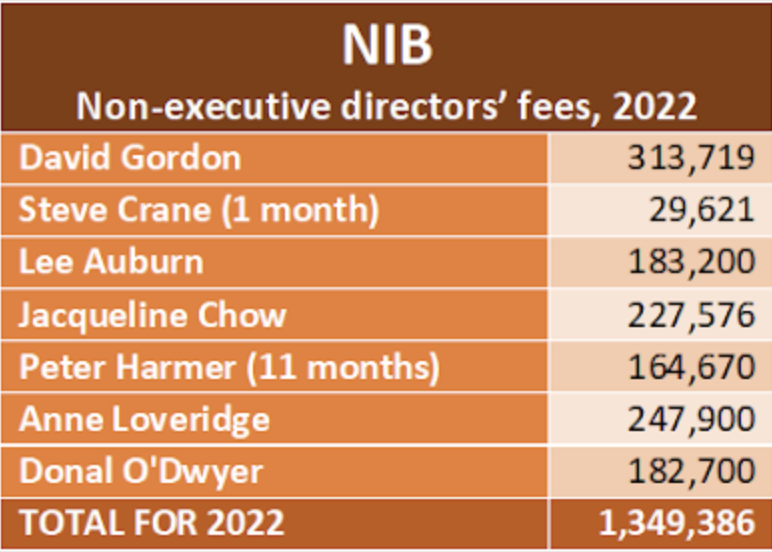

Directors also do well. Non-executive directors of these companies can expect to be paid between $150,00 and $200,000 a year for attending 12 to 15 board meetings and another half-dozen meetings of board committees.

Almost all of these professional directors have similar posts on two or three other major company boards where they are paid comparable amounts. Medibank Privates Anna Bligh is also the CEO of the Australian Bankers Association.

The Prime Minister earns $587,000, including loadings.

And heres another table. It shows how much money would be saved and redirected into healthcare if Medicares level of administrative efficiency applied to private insurance. Over the most recent three years for which figures are available, those savings would allow premiums to be reduced by 14% overall, or almost $11 billion.

What about the hospitals?

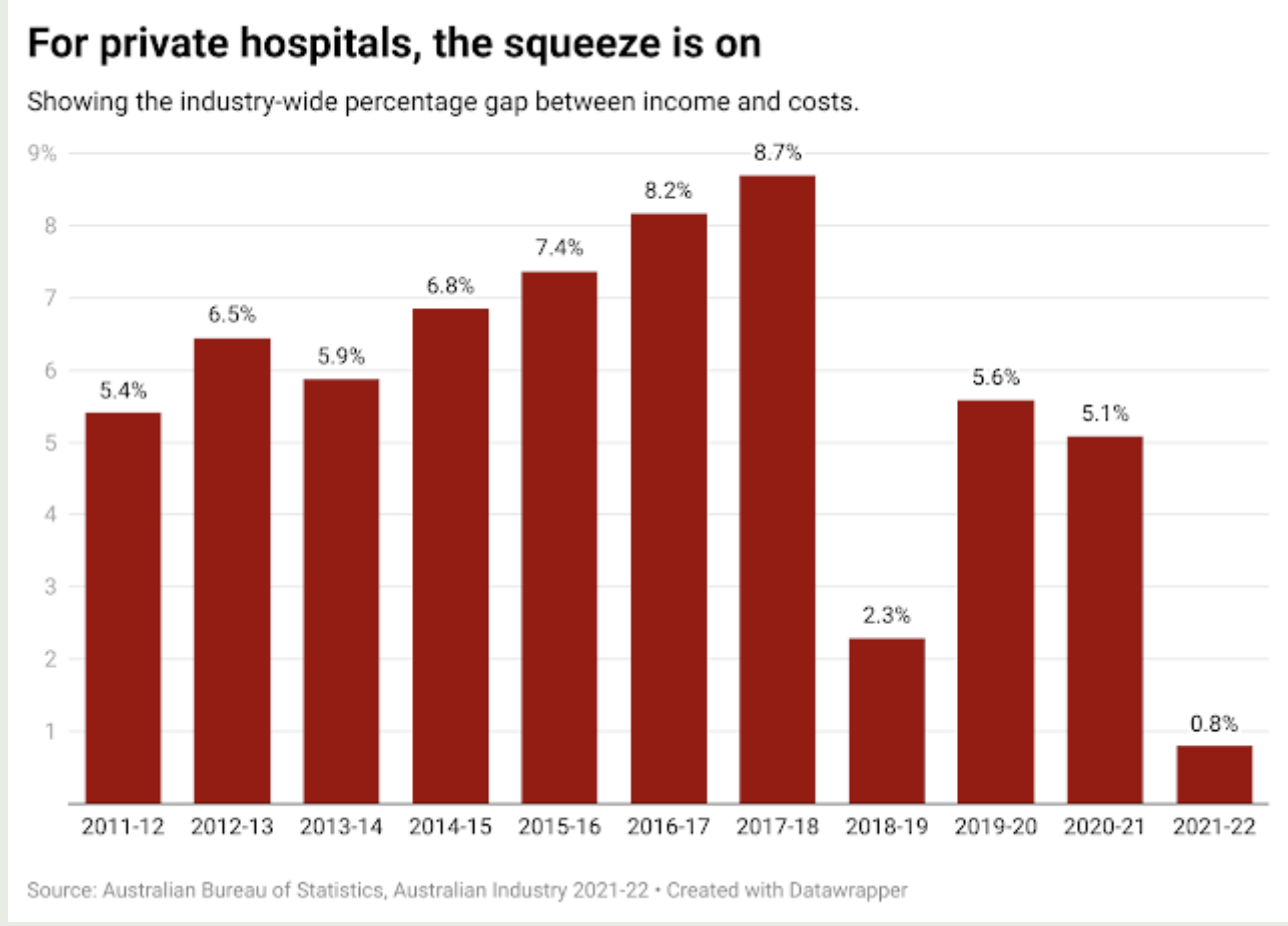

Private hospitals account for 36% of all the hospital beds in Australia. It is in the nations clear interest for those beds to remain available. But they are not being funded in a way that is either efficient or fair.

At the same time as the insurers were reaping large profits, hospitals were caught in a squeeze between rising costs and inadequate funding. According to the ABS, the gap between revenue and costs fell to 0.8% in 2021-22.

The Australian Private Hospitals Association, the industry lobby group, says the current situation is one of the worst in living memory.

The cost of food, power, medical supplies, and medical technology have increased by an estimated 10 to 15 percent in the last year, said the organisations CEO, Michael Roff. At the same time, health insurance companies are only offering hospitals increased payments in the order of 2 to 3 percent.

In the meantime, private health insurers are still sitting on about $700 million in deferred claims liability premiums that members paid during the COVID-19 pandemic when they couldnt use their health insurance.

That aggregate gross margin of 0.8% means any hospital with even slightly above-average costs is operating at a loss. If that situation has worsened since then, it means the majority of private hospitals in Australia are now losing money.

Faced with those losses, operators have to choose one of three options: to substantially increase out-of-pocket charges to patients; to cut back further on costs, inevitably impacting on standards of care; or to close.

In a rational world, the aim of private healthcare funding would be to give patients the best deal possible, while ensuring the viability of efficient hospitals. The present system does neither. Instead, it has created a featherbedded, inefficient class of middlemen at the expense of those who deliver health services and those who need them.

It doesnt have to be like this. But it needs a federal government thats willing to make big changes. It involves funding the hospitals directly from government, giving the administration to Medicare, and opening private hospitals to all patients, not just those who can afford to pay for their own treatment.

We would have a single, integrated hospital system with public and private components.

In the lead-up to the 2004 election the one Mark Latham lost the shadow health minister, Julia Gillard, promised to initiate a version of that. A Labor government, Gillard said, would ensure public funding for the complete care of everyone over the age of 75, whether they were treated in public or private hospitals.

When the election was lost, the whole idea of direct funding disappeared. Perhaps its time to have another look.

It would not require at least at the beginning a crippling cost to the federal budget. But a substantial amount should be set aside to purchase, in collaboration with the states, service packages from private hospital operators.

Hospitals … caught in a funding squeeze The hospitals would be required to take full responsibility for providing the contracted services, which would mean surgeons and anaesthetists would no longer bill patients directly but would have to deal with the hospital instead. Under the present system, senior surgeons in the private sector can earn several million dollars a year because individual patients have no pricing power. Hospital operators do. The bigger the pool of money, the more effective the system would be. If the government eventually became the dominant funder, as it should, the shift in market forces would be profound and massively beneficial.

Taxes would have to be increased but far fewer people would need to buy insurance. Overall, the nation would get a hospital system that delivered far better value for money. Overall, we would pay less and get more.

And it would be fairer. The basic principle of universal healthcare that you should be treated according to your need, not to how much money youve got has been a core Labor value. All we need now is a Labor government that shares those values.

Republished from The Policy Post . Original article published on 12 September, 2023.