Record highs: February market and economic review

February 7, 2024

Not only has the stock market shaken off its new year hangover but the All-Ords is now higher than after its Santa Rally in December 2023. Indeed, it has reached a record high.

Bears say don’t be fooled by the index’s present spike. The aggressive monetary tightening in 2022 and 2023 will wreak havoc on economies and corporate earnings, though with a delay.

Bulls insist the market’s breakout will continue given the propitious outlook for most economies which is propelled by looser financial conditions and the prospect of official rate cuts.

For now, my models show the bulls have the upper hand. Read on….

Market breakout

The December Santa rally ended abruptly on 2 January 2024 after the Boxing Day holiday. Thereafter the Australian All-Ords share index fell 3.7% to Tuesday 18 January but since then has rebounded by 4.7%

Market’s meander

After troughing on 30 October 2023, the index rose 14.4% to 2 January 2023. Over the course of calendar 2023 it was up 8.5% notwithstanding gyrating sideways much of the time.

In 2023 the All-Ords swung between pessimism (that inflation was sticky so rates would stay high and weigh down the economy and profits) and optimism (that inflation was beaten, rates would fall and there would be no hard economic and corporate landing).

In 2024 that debate has been resolved. Inflation has fallen dramatically so bond futures markets are pricing in official rate cuts earlier than central banks had planned.

Big picture

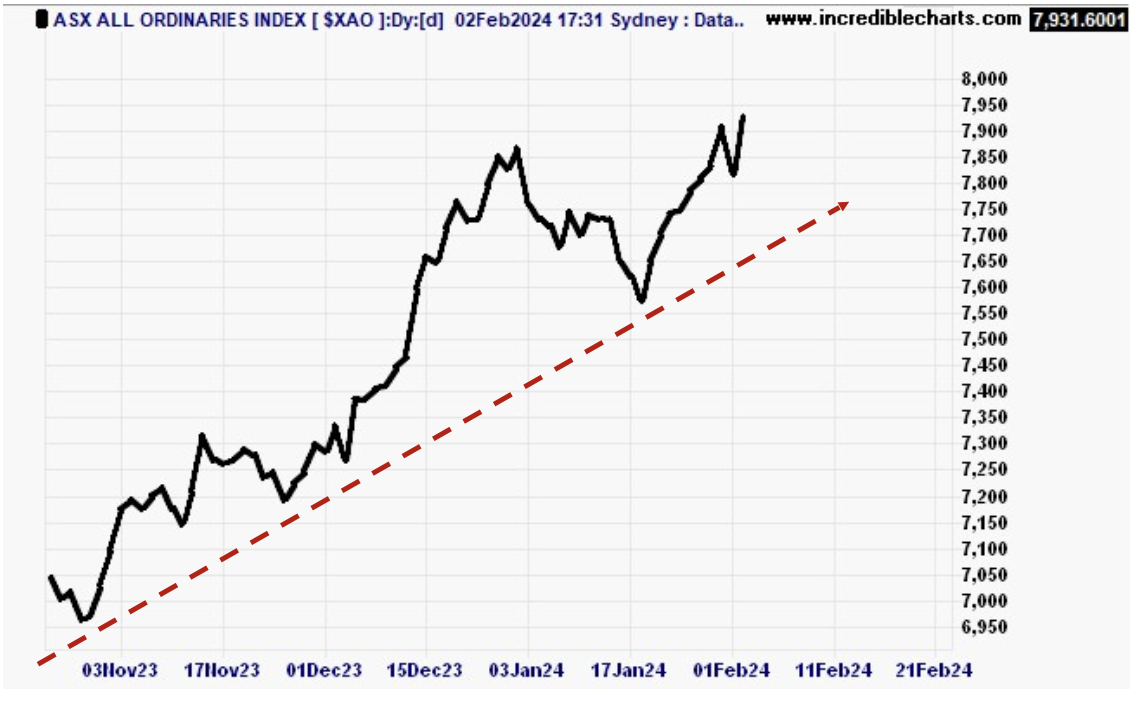

The All-Ords has been see-sawing sideways within a range of roundly 6,600 to 7,900 since April 2021. See next chart.

Last Friday 2 February 2024 the All-Ords reached a record high (7931.6) beating its previous high on the 4 January 2022 (7926.8). If the index keeps rising it will show it has broken out of its previous range bound yoyoing.

Lasting breakout or last hurrah?

Bears say that since August 2021 the All-Ords has not made any significant gain but instead undergone sharp corrections in June and September 2022. Bears say this confirms we are in a protracted bear market that will not end soon, so don’t be fooled by the index’s present spike. The aggressive monetary tightening in 2022 and 2023 will wreak havoc on economies and earnings, though with a delay.

Bulls say that since September 2022 the index has been climbing a “wall of worry” which is typical of a new bull market. The November to December 2023 rally was briefly interrupted in January but has since resumed. Bulls insist the market’s breakout will continue given the propitious outlook for economies here and abroad which is being propelled by looser financial conditions and the prospect of rate cuts.

Australia’s Market

On short-to-medium-term trend analysis, the All-Ords index is bullish since its red 10-day trend line is well above its green 30-day one.

Its price momentum as measured by the MACD oscillator went positive last week after being negative for the previous three weeks.

On medium-to-long-term trend analysis, the All-Ords index is bullish. Its green 30-day trend line is above its blue 300-day one.

Unlike America, Australia’s stock market for most of last year swung sideways because it has few tech stocks promising new riches through AI (artificial intelligence). However, the All-Ords like the S&P 500 enjoyed a strong rally in November and December not just in hi-tech stocks but across the board.

The All-Ords dark green Coppock (COP) momentum indicator bottomed at the end of December 2022 and thereafter trended up into positive territory where it has wobbled, but still stayed modestly positive.

In the past whenever the Coppock turned up in negative territory it signalled the end of an Australian bear market. Only end of month readings are meaningful for the Coppock since it is a monthly signal.

Economic Outlook

The International Monetary Fund’s latest global economic outlook is less gloomy thanks to inflation falling faster and economies being more resilient to central bank rate hikes than previously expected.

Global real GDP growth is projected to fall from an estimated 3.5 percent in 2022 to 3.0 percent in both 2023 and 2024 due to central bank policy rate increases to combat inflation.

Global headline consumer price inflation is expected to decline from 8.7 percent in 2022 to 6.8 percent in 2023, 5.2 percent in 2024, and 4.4 percent in 2025. Underlying (core) inflation is projected to decline more gradually.

For Australia and America, the IMF forecasts are worse on growth, but better on inflation.

In Australia’s case the IMF projects growth of 1.2% and inflation of 4.0% in 2024. That compares with estimated growth of 1.5% and known inflation of 4.1% in 2023. The IMF’s forecast of 4.0% inflation in 2024 was made before the ABS announced that Australia had already got inflation down to almost that rate in 2023.

For the USA, the IMF forecasts 2.1 % growth and 2.5% inflation for 2024 versus 2.5% growth and 3.4% inflation recorded for 2023.

Financial Outlook

If there is a recession central banks are likely to cut rates regardless of what the inflation rate is. However, if there is no recession, central banks are more likely to hold off rate cuts until they are certain that inflation is beaten.

The present economic consensus is that not only the USA, but also most other developed countries including Australia will avoid a recession in 2024. Also, inflation will fall further allowing central banks to cut official (cash) interest rates.

That would be a Goldilocks’ result – an economy not too hot, not too cold, but just right. Others have described it as “immaculate disinflation”, meaning inflation will be tamed without breaking the economy and causing high unemployment.

The debate now is not whether official cash rates will be cut but when that will happen - in the first half of this year (as bond futures markets anticipate) or in the second half (as central bank governors imply)?

There is a view that the European Central Bank will cut rates before the US Federal Reserve Bank since the EU’s economy is spluttering. Also, that Australia’s Reserve Bank could be the last to cut its cash rate because our inflation was more obdurate than that of others.

However, the latest CPI data shows that Australia was in line with most other English-speaking countries (USA, UK, and Canada) in bringing down annual inflation to around 4% at the end of 2023. If Australia’s progress on reducing inflation continues, then it might not be the last to reduce rates.

By contrast Japan and China are more worried about deflation than excess inflation. The Bank of Japan’s discount (cash) rate is only 0.3% notwithstanding that its economy’s recent rebound has pushed inflation above the BoJ’s 2% target.

The Peoples Bank of China’s cash rate is 2.65%. Unlike the BoJ it vowed to refrain from “flooding” the market with liquidity even though China’s property sector has collapsed, and its annual inflation rate is negative (minus 0.3%). However, the PBoC recently cut its reserve requirement ratio (RRR) for banks allowing them to make approximately 1 trillion yuan (about A$210 billion) in new loans. Additionally, it lowered the interest rate on one-year medium-term lending facility loans and injected an extra 400 billion yuan (about A$84 billion) into non-bank lending markets.

Loose credit conditions

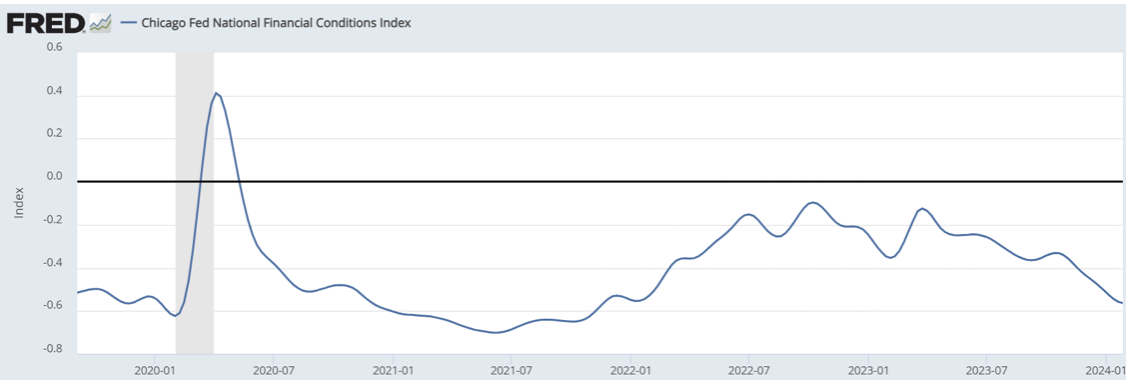

At this stage America appears impervious to recession because its financial conditions have significantly eased since the first quarter of 2023 and continue to do so. See chart below. Bulls say this augers well for economic activity, employment, wages and profits in 2024.

Chicago Fed’s National Financial Conditions Index (NFCI) for USA

Europe too has loose financial conditions, but they have sharply tightened since the end of the September quarter 2023. Bears say that if this continues it could trigger a recession and depress corporate earnings this year. See next chart.

European Commission – Financial Conditions Index for European Union

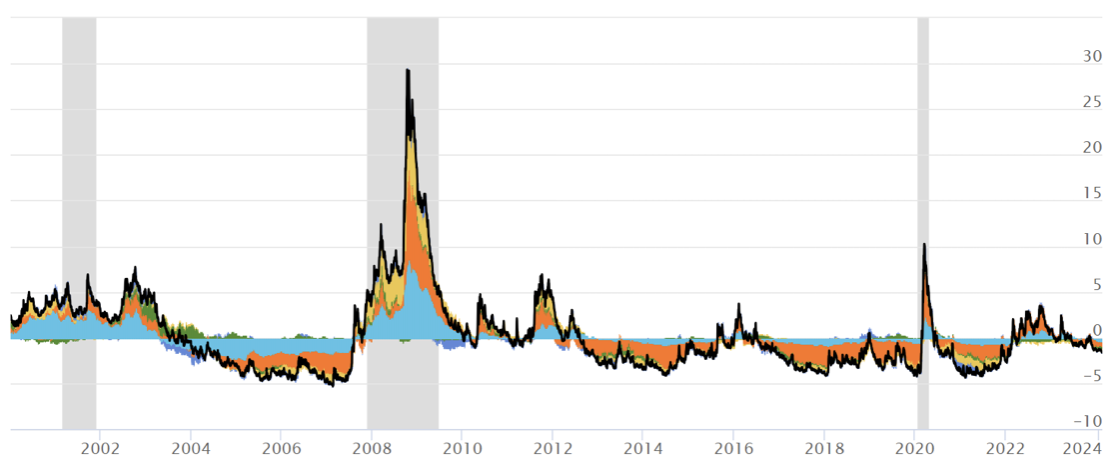

For the world, financial stress is gone following tight conditions in 2022 and early 2023. Bulls say this should make for strong share markets in 2024 while Bears say the lagged effects of earlier tighter conditions will bite in the first half of 2024. Also, China’s stock market has collapsed in the last two years signalling that its economy won’t rescue the world in 2024.

US Treasury Office of Financial Research – Global Financial Stress Index

Bulls versus Bears

Since the share market is a live barometer of investor sentiment it is also a pointer to economic conditions ahead.

Bulls say the market has boomed because inflation is down, bond yields have fallen, cash rates will be cut, and economic activity and employment remain sufficiently resilient to avoid a recession.

Bears say the fall in bond yields (and resultant rally in bond prices) since October last year reflects a slowdown in global economic growth that will end not only in a recession, but also price deflation. Moreover, central banks say they wont cut official rates until excess inflation is convincingly slayed and that could be a long way off.

Conclusion

I do not forecast markets because those who do so generally get it wrong. Instead, I gauge the market’s present trend and momentum to let Mr Market speak for himself. Then I try to rationalise the market’s behaviour on monetary, fiscal, economic, or political grounds.

My technical models show:

- On short-to-medium-term trend analysis both the Australian All-Ords index and the American S&P 500 are bullish.

- On medium-to-long-term trend analysis the Australian and US markets are also bullish.

- The Coppock momentum indicators of both markets are positive. They turned up in negative territory early last year signalling the previous bear market was over.