The Intergenerational Report: helpful, but so much less than it could be

July 1, 2021

Since the 2021 Intergenerational Report (IGR) was released the media has been bombarding us with its predictions and forecasts. Just take The Australian’s front-page headline ‘Economic snapshot warns of disaster if we dont act now’, with the first line reading, Australians average incomes will be $32,000 lower. Or think of Paul Kellys header, ‘Australia sleeping through its alarm’.

You could be forgiven for thinking that the Treasury was forecasting/predicting an economic and social decline. It isnt. It is simply projecting, not forecasting, the impact of maintaining current policy settings on the economy, expenditure, revenue and hence debt on the basis of plausible assumptions about population, participation and productivity. The IGRs projections are for 40 years.

It seems that Treasury is sanguine that all is well in hand we might grow more slowly as a population and economy than previously projected, our government debt might increase, but grow we will, both in aggregate terms and in our per-person income and wealth. The economy and the fiscal position are basically sound, it says, and Australia is well placed to address the challenges, implicitly acknowledging that policies will certainly change over time to respond.

The IGR is not a considered look at Australias possible futures nor our policy options. It is hobbled by its focus on the link between demography, the economy and the budget. Its usefulness is reduced by a rather mechanical projection of central tendency estimates of productivity, interest rates and migration. Yes, there is some sensitivity analysis of each of these allowing for minor variations, but there is no discussion of plausible shocks. Even so, small variations in assumptions and starting points projected over 40 years produce what looks like significant swings in 2061 outcomes. That is the law of compounding.

The problem is that the IGR is neither fish nor fowl. It is neither a focus solely on the implications of demography for the budget nor a full examination of the range of scenarios that could impact our fiscal position. Scenario planning could help us understand the uncertainties, risks and opportunities we face and their implications for the fiscal position much better. It could help us develop policies that are robust against a variety of circumstances and preserve valuable options. Of course, the selection and weighting of scenarios would be an intensely politically fraught process. It is probably much better done outside government, though fully resourced, than by a department of state.

But could our IGR be improved by more explicitly considering risk short of full scenario development?

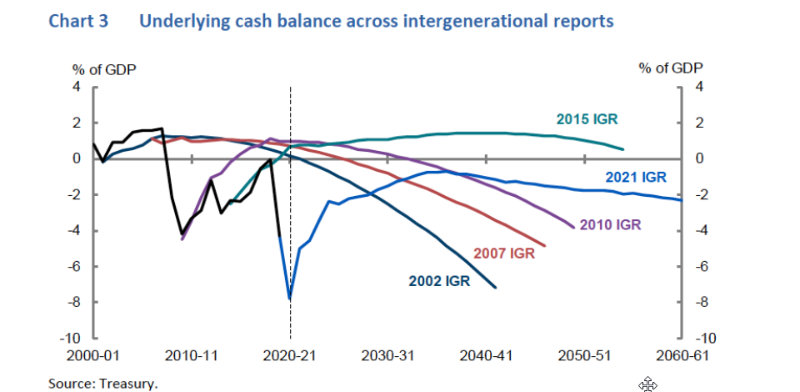

What strikes you about this chart?

In none of the 5 IGR reports from the first in 2002 did Treasury anticipate the multiple economic shocks we have had since the turn of the century. For that, they cannot be blamed. None of us did at least in terms of their timing or their precise source. But of course, Treasury knew that there would be shocks.

I recall sitting in a meeting with my Secretary colleagues in 2003 when the prospect of a financial crisis linked with the poor regulation of the US financial markets was discussed. It was at this point that Treasury said it was re-examining the appropriate response to a recession to see if we could do better than we did in the fiscal stimulus package developed to help pull us out of the 1990 recession we had to have. Instead of placing the emphasis on major infrastructure projects that took time to kick through in the economy, Treasury began to fashion the Go early, go hard, go households strategy.

Similarly, in the 2008 review of Australias national biosecurity plan ‘One Biosecurity’, concern about pandemic risks for humans arising from highly pathogenic zoonotic diseases was highlighted.

In 2013, when PwC issued ‘Protecting Prosperity’ which extended IGR analysis to look at the reasons for tax reform, it listed more than half a dozen possible shocks to the economy including, notably, geopolitical disruption in Asia as China flexed its increasing strength. That paper modelled a fiscal shock of the scale of the GFC and concluded that, if we wanted to preserve our options for bold stimulus action, there was no fiscal room for suggesting any reduction in the overall tax take. Instead, we argued for a change in the tax mix to boost productivity.

In short, we know that the world will not reflect the smooth business as usual assumptions that drive the IGR. How robust our fiscal position really is can only be discovered by stress testing it against a range of plausible shocks within the next ten to twenty years.

Chief among those would be a conflict involving our biggest trading partner China. As it is, the IGR blandly assumes Projections for non-demand driven programs such as defence grow in line with the economy and are assumed to remain a constant share of GDP in the long run. That assumed constant share is 2%. This does not seem consistent with the heightened defence rhetoric nor indeed the current levels of equipment orders, let alone plans.

It is more plausible to think in terms of 3-3.5% of GDP being devoted to defence broadly defined to include critical infrastructure. The IGR says nothing about the risks to revenue or the terms of trade from the possibility of a China conflict, even one in which we are not directly involved. Put simply, there is a significant possibility of circumstances that could see a negative swing equivalent to 1-2% of GDP (or indeed much more) in our net fiscal position.

It seems totally implausible that the current or successive governments will not lift support for aged care beyond the current interim response to the Aged Care Royal Commissions report or for the NDIS, bearing in mind the long-running Disability Royal Commission. It is not hard to imagine a further 1.5-2% of GDP going into each of these sectors over time to further lift the quality of care rather than just responding to the changing age structure of the population. The electorate will be ageing along with the population and it will hold the Commonwealth responsible to provide these funds.

Climate change is another potential threat to the Commonwealths fiscal position. Its revenue stream is highly sensitive to movements in commodity prices, particularly for our iron ore, energy and agricultural exports. Both reduction in global demand for carbon-intensive resources and the risk of carbon tariffs on those not judged to be acting fast enough, present real medium-term risks to revenue streams.

On the expenditure side of the budget, climate change will increase the probability of natural disasters, vastly add to infrastructure needs, challenge the agricultural sector and impose additional health costs. The governments failure to fully endorse the need for net-zero targets and play its part in driving global action, rather than pleading for yet more special deals, increases these risks. Equally, it is failing to provide adequate stimulus or price signals for risk-reducing green energy industries.

I am not suggesting that the Treasury should attempt to predict the timing, or the precise nature, of a shock on the revenue or expenditure side of the budget, but rather that it should provide sensitivity analysis reflecting a shock at least of the scale of the GFC within the next ten years.

I dont think that things on the fiscal front would look so rosy then. The constraint of 23.9% per cent of GDP on taxes will look a little foolish. And the stage 3 tax cuts just might look unsustainable.