The lopsided distributional impacts of Australias profit-price inflation

February 28, 2023

With excess corporate profits accounting for 69% of additional inflation beyond the RBAs target, current anti-inflation policy blames the victims of inflation, while ignoring its perpetrators.

Workers in Australia have suffered considerable economic losses as a result of accelerating inflation since the onset of the COVID pandemic.

Reaching a year-over-year rate of 7.8% by end-2022, inflation has rapidly eroded the real purchasing power of workers incomes; average wages are currently growing at less than half the pace of prices. Now, severe monetary tightening by the Reserve Bank of Australia (through 9 consecutive interest rate increases) is imposing additional pain on millions of workers. Tens of billions of dollars of household disposable income are being diverted away from consumer spending, into extra interest payments made to banks and other lenders. Most ominously, signs of macroeconomic slowdown from higher interest rates portend job losses and even greater income losses in the month ahead.

The pain experienced by workers through this inflationary episode contrasts sharply with an unprecedented upsurge in business profitability at the same time. Additional profits resulted from businesses increasing prices for the goods and services they sell, above and beyond incremental expenses for their own purchases of inputs and supplies. This dramatic expansion of business profits (taking gross corporate profits to almost 30% of national GDP, the highest in history) has been mostly unremarked on by the RBA and other macroeconomic policy-makers. They have focused instead on the supposed risk of a wage-price spiral.

However, an analysis of national accounts data confirms the dominant role of business profits in driving higher prices in Australia not wages, which have lagged well behind inflation (both in scale and in timing). This suggests the focus of monetary policy on wage restraint is misplaced and unfair.

I used ABS national accounts data to disaggregate the composition of rising prices in Australia since the onset of the COVID pandemic using the December quarter of 2019 (the last pre-COVID quarter) as the starting point. This approach used the GDP deflator as a measure of economy-wide inflation; it is similar to the more commonly reported consumer price index, except that it considers prices of all Australian-produced goods and services (including government services, investment goods, and exports), not just those bought by private households. Since the deflator is constructed with the same methodology as ABSs national accounts measures of income distribution across the various factors of production, a consistent and complete decomposition of the sources of higher prices can be achieved.

Of course, one reason factor incomes may grow is because of increases in the real output of goods and services, and the analysis controls for that. Furthermore, a certain level of inflation in the economy is generally deemed beneficial (as represented by the RBAs 2.5% inflation target), so the analysis allows for increases in nominal unit costs associated with the various factors of production consistent with that target. What is left is the excess increases in factor costs (and hence in final prices of output) that have driven Australian inflation well above the 2.5% target since the pandemic.

By decomposing the sources of excess price inflation, we can confirm that wages and unit labor costs are definitely not the source of excess price pressures:

- As of the September quarter of 2022 (most recent data available), Australian businesses had increased prices by a total of $160 billion per year over and above their higher expenses for labour, taxes, and other inputs, and over and above new profits generated by growth in real economic output.

- Without these additional profits recorded by Australian businesses since the pandemic, inflation would have been much slower than was experienced in practice: an annual average of 2.7% per year, barely half of the 5.2% annual average actually recorded since end-2019.

- That pace of inflation would have fallen within the RBAs target inflation band (equal to its 2.5% target plus-or-minus 0.5%). Even within the RBAs own policy rule, therefore, current painful interest rate hikes would be unnecessary.

- Even if we allow for modest nominal inflation in unit profit margins, consistent with the RBAs 2.5% target, excess profits drove prices far higher than they needed to be once again, above and beyond the costs of other inputs (including labour and taxes) and the growth of profits due to expanded real output. Even allowing for inflation in profit margins equal to the RBA target, inflation would have averaged just 3.3% since the pandemic. That is only slightly above the target band, and current harsh interest rate changes would again have been unnecessary.

- Decomposition of the income flows associated with excess inflation since end-2019 confirms the dominance of corporate profits in the acceleration of inflation. Excess corporate profits account for 69% of additional inflation beyond the RBAs target. Rising unit labour costs account for just 18% of that inflation.

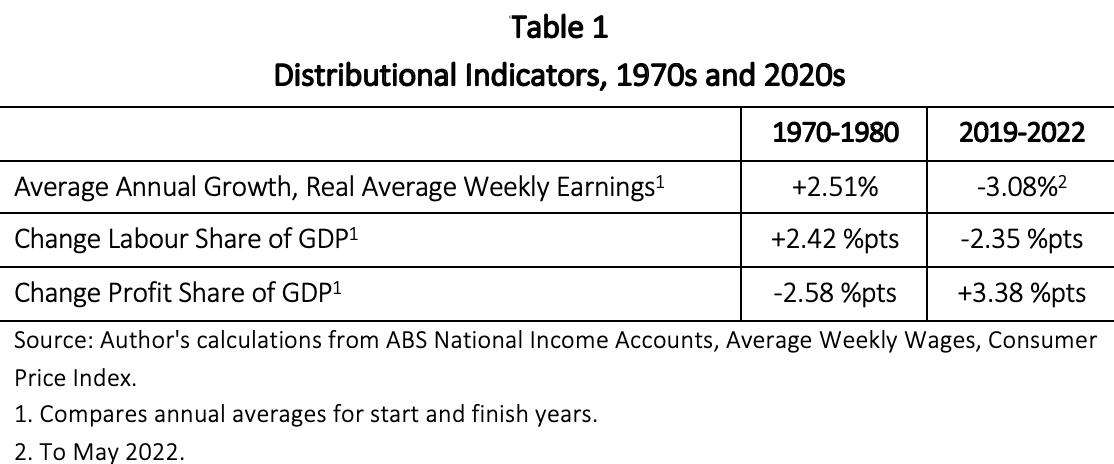

- The distributional dimensions of post-COVID inflation (falling real wages, falling labour share of GDP, and record corporate profits) are completely opposite from the experience of the 1970s (when real wages rose, the labour share of GDP increased, and corporate profit margins fell see Table 1). This historical comparison confirms that fears of a 1970s-style wage price spiral are not justified. Instead, inflation in Australia since the pandemic clearly reflects a profit-price dynamic.

It is irrefutable that the main beneficiary of the acceleration of inflation in Australia since the COVID pandemic has been the business sector. Corporations have increased their profits much faster than the nominal growth of Australias economy, and hence increased their share of GDP significantly. As Australia was traversing an unprecedented series of economic, social, and public health challenges (including lockdowns, supply chain disruptions, and accelerating inflation), corporations lifted prices far above and beyond the cost of their own input purchases. The excess expansion of profits per unit of production (that is, the amount of profit built into average unit prices for all goods and services produced in Australia) accounts for the lions share (69%) of the acceleration in inflation beyond the RBAs 2.5% target rate. Growth in labour compensation beyond what would normally be expected (given economic growth and target inflation) has played a small role.

Analogies drawn between the current inflationary episode and the experience of the 1970s are inappropriate. Wages have grown much more slowly than prices, workers real wages and their share of total GDP have declined rapidly, and profits have expanded to unprecedented highs: both in absolute terms and as a share of GDP. All of these trends are opposite to the experience of the 1970s. The focus in current anti-inflation policy on suppressing wage growth, enforcing a permanent reduction in real wages, while ignoring the role of record profits in driving post-pandemic inflation, reflects an ahistorical and ideological approach to macroeconomic management. It blames the victims of inflation, while ignoring its perpetrators, and will impose further needless harm in coming months through further real wage reductions, and quite likely an economic recession.