The minimum wage decision, inflation and the low paid

June 16, 2022

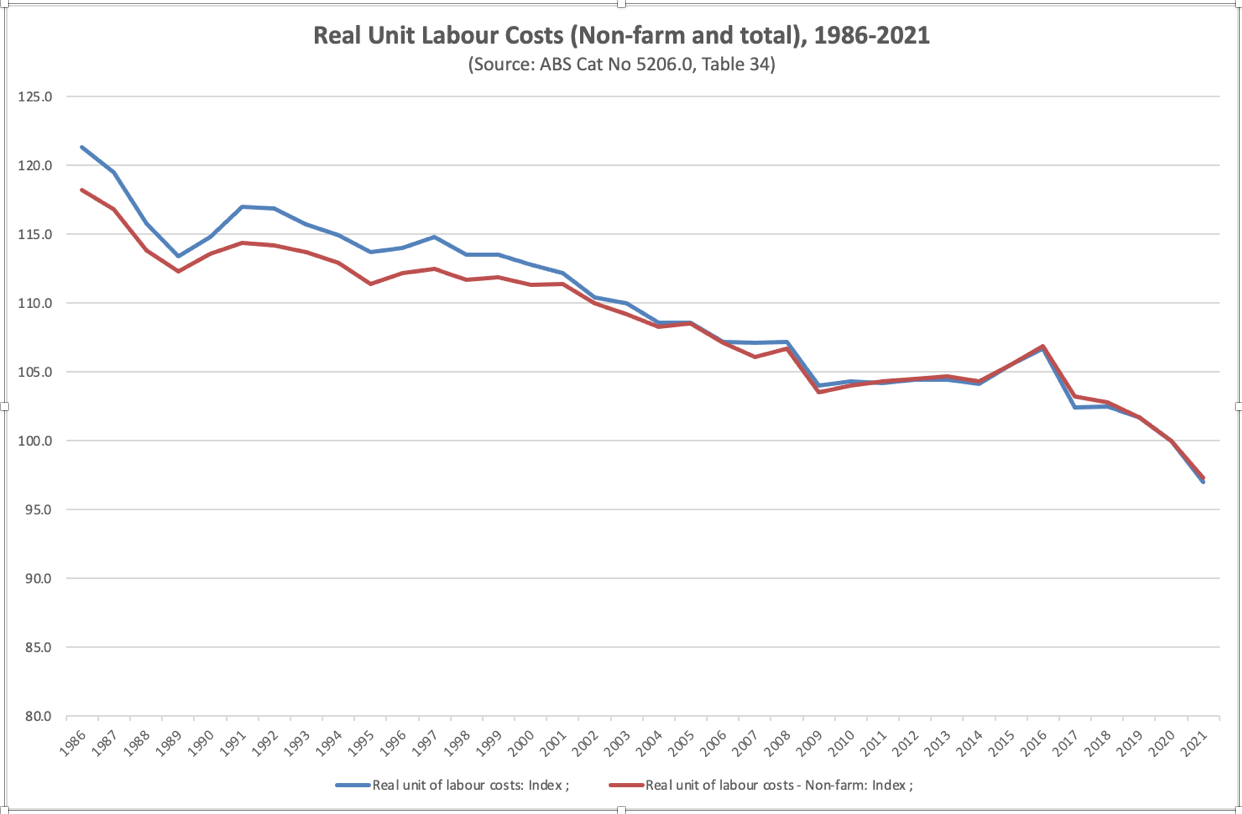

_The Real Unit Labour Cost is presently 20 per cent lower than it was__in 1986 meaning the growth in productivity gains to employers has been substantially higher than the growth in real wages.

_

This weeks $40 per weekThis minimum wage increase decision by the Fair Work Commission (FWC) equivalent to 5.2% for minimum wage workers has been reported as the largest in 16 years. The period is actually longer than that, because the 2006 decision (which provided for an increase of 5.7% at the lower end of the wage scale) covered a period of 18 months, and was more like an annual increase of 3.8%.

Take that into account, and this looks like the largest increase since annual reviews started in the early 1990s.

So how big was it really? And was it appropriate in the circumstances?

For most workers, the lowest wage they can legally be paid (the award wage that applies to them) is above the minimum wage. As your award wage goes up, to a point at least, the percentage value of a $40 award minimum wage increase goes down. For most of those, the real value of the minimum wage that is, what its worth after 5.1% inflation is taken into account will have gone down, even after this decision, but not by much. So its not the largest increase in real wages by any means.

The lowest increase in any award wage under this decision will be 4.6%, compared to current inflation of 5.1%. That gap of 0.5% is equal to the increase in the amount of superannuation that employers are legally required to be paid from July this year. So, in a way, many award-wage workers are treading water.

And if you add in that superannuation rise (but ignore delayed implementation in three sectors), the real minimum wage itself will have increased. Though low income earners purchasing power probably has not genuinely increased, because low-income earners spend a high proportion of their pay on essentials, and the consumer price index of non-discretionary items went up by a full 6.6% over the past year.

Moreover, inflation is rising faster than the Fair Work Commission (FWC) can keep up. A month ago, the Reserve Bank of Australia (RBA) forecast inflation would be 5.9% by December 2022, but that it would go down after that. This week, the RBAs governor said that forecast was now 7%, though he still expected it to fall after that.

Even if it does go down then, there is a good chance that this time next year the inflation rate will still be above the current 5.1%, and the FWC will face the same problems in reconciling workers need to keep up with prices growth, alongside the need to keep inflation down.

One of those problems will be the compression of relativities that this decision has brought about, with wage increases being higher for the lowest paid than for those closer to the median. The Commission had stuck to uniform percentage increases for quite some time, to avoid such problems. Before that, it had issued several decisions that compressed relativities, and these reduced the incentive to train or progress, or the relevance of awards for many workers. Now the FWC is forced, as it sees it, to do this again, to balance the twin problems of protecting the lowest paid while minimising the impact of its decision on inflation.

There is little talk now of the minimum wage decision costing jobs, with unemployment so low and job vacancies so high. Instead, concern is mainly about its impact on inflation.

As a general principle in economics, if the increase in wages is less than the increase in prices plus the growth in national productivity (achieved through, for example, new technology at work), then the impact of wage increases on inflation will be neutral. As less than a quarter of workers are paid award wages, and the increase in award wages is mostly less than the increase in prices plus productivity growth, the decision would still ease inflationary pressures, by comparison with something that stabilised workers share in national income.

Indeed, for the past four decades, wages have in this sense been a downward influence on inflation. That is because real wages have consistently grown less than productivity. When that happens, the gains of productivity improvements accrue to capital rather than labour. If prices rise in those circumstances, then those rising prices are mostly boosting profits, not wages.

One of the most useful indicators of how much national income has gone to wages as opposed to profits is real unit labour costs (RULC) the level of real wages discounted by growth in productivity. In effect, it tells you the share of national income going to wages rather than profit, once government is set aside. RULC has been steadily declining since the current ABS series began in 1986 and is now at its lowest level.

RULC is presently 20 per cent lower than it was then, meaning the growth in productivity gains to employers has been substantially higher than the growth in real wages.

For much of this period, changes to the real minimum wage have also fallen behind growth in productivity.

The steady decline in RULC over that period reflects the steady decline in labours bargaining power over 36 years. It also means that wages have become a progressively smaller component of selling prices.

So there is little evidence of, or prospect for, cost-push inflation arising from a wage-price spiral such as during the experience of the 1970s. In one year at that time, real wages went up by 10 %. Any suggestion that this could happen now would be laughable.

You dont hear, however, about a profit-price spiral, even though it is profits that are growing faster than wages. People profiting from higher prices during supply shortages? Thats the market. A different moral standard is applied. None suggest that inflation should be reduced by compulsorily cutting profits. It could not be done, so it should not be done.

However, that most prices cannot be reduced forcibly by pushing down profits does not mean that the burden of adjusting to, and reducing, inflation should fall on workers, especially on the lowest paid.

In that context, it is hardly surprising that the Fair Work Commission should feel the need to live up to its legislative duty to the low paid.