How best to tackle inflation

March 7, 2023

After nine successive increases in the Reserve Bank’s cash rate, this article argues that it is time to pause. In addition, given the sources of increased inflation, more targeted measures are called for rather than the blunt instrument of further interest rate increases.

Over the course of 2022 consumer prices increased by 7.8 per cent, about three times as fast as the Reserve Bank’s target range of 2-3 per cent. In response the RBA has increased its cash rate of interest nine times since last May from 0.1 per cent to a current 3.35 per cent.

This monetary tightening is beginning to bite, and the rate of inflation may be starting to decelerate, with the monthly consumer price index showing a lower 7.4 per cent increase in the twelve months to January. Nevertheless, the RBA Board signalled after its last meeting that more interest rate increases (plural) can be expected.

The Bank worries that unless monetary policy continues to press down on the economy, wages will surge as employees seek to recover their recent loss of living standards. What they then fear most is the creation of a wage-price spiral and consequently, continuing and possibly increasing inflation.

To date, however, wage growth has been lagging prices, with wage rates increasing by only 3.3 per cent over the course of last year – less than half the rate of price increases. And while the rate of wage increase was picking up through the course of 2022, that still only represents a return to past norms.

Furthermore, now that monetary policy has been tightened so substantially already, the future of inflation mainly depends upon peoples’ expectations about the future rate of wage and price increases because these expectations can be self-fulfilling. So far, however, as the Governor of the RBA himself admits: “medium-term inflation expectations remain well anchored”.

Thus, as the Governor put it:

“In broad terms, the RBA and many other central banks are managing two risks. One is the risk of not doing enough, which would result in high inflation persisting and then later proving very costly to get down. The other is the risk that we move too fast, or too far, and that the economy slows by more than is necessary to bring inflation down in a timely way. The path here is a narrow one.”

Given this balance of risks, several analysts, including me, are starting to think that the RBA Board should pause before authorising any further interest rate increases. Such a pause would allow the Board to better assess how the economy is responding to the past increases. The risk is that if the RBA continues to raise interest rates that will diminish demand further and disrupt the economy leading to higher unemployment.

Already the latest National Accounts data for the recent December quarter show that the economy is starting to slow. GDP growth through 2022 was 2.7 per cent, representing some slowing compared to earlier in the year. Consumer demand was weak, increasing by only 0.3 per cent in the December quarter, and households are clearly drawing down on their savings, with the savings ratio of only 4.5 per cent – lower than the pre-Covid level. In addition, infrastructure expenditure is down and loans for housing are also starting to fall, impacting the construction industry which has been one for the fastest growing sectors. Not surprisingly, unemployment is starting to creep up.

This slowing economy is in itself a good reason for a pause in interest rate increases, but in addition the focus on wage increases is arguably misplaced.

In an important Pearls & Irritations article, by Jim Stanford from The Australia Institute. The lopsided distributional impacts of Australia’s profit-price inflation, showed that excess corporate profits accounted for 69 per cent of the additional inflation beyond the RBA’s target. Rising unit labour costs account for just 18 per cent of that inflation, and accordingly wages are not the problem.

Nevertheless, the RBA would probably respond that if the rate of return to either of the two factors of production is increasing too rapidly, then monetary tightening will help restore the previous rate of return. As interest rates act to reduce demand, they reduce the rate of return on capital in the same way as they can reduce the return to labour.

Interest rates are, however, a very blunt instrument for bringing down inflation. Before increasing them further we need to assess why the return to capital increased and how widespread was that increase in corporate profits.

An analysis of the increase in corporate profits by industry

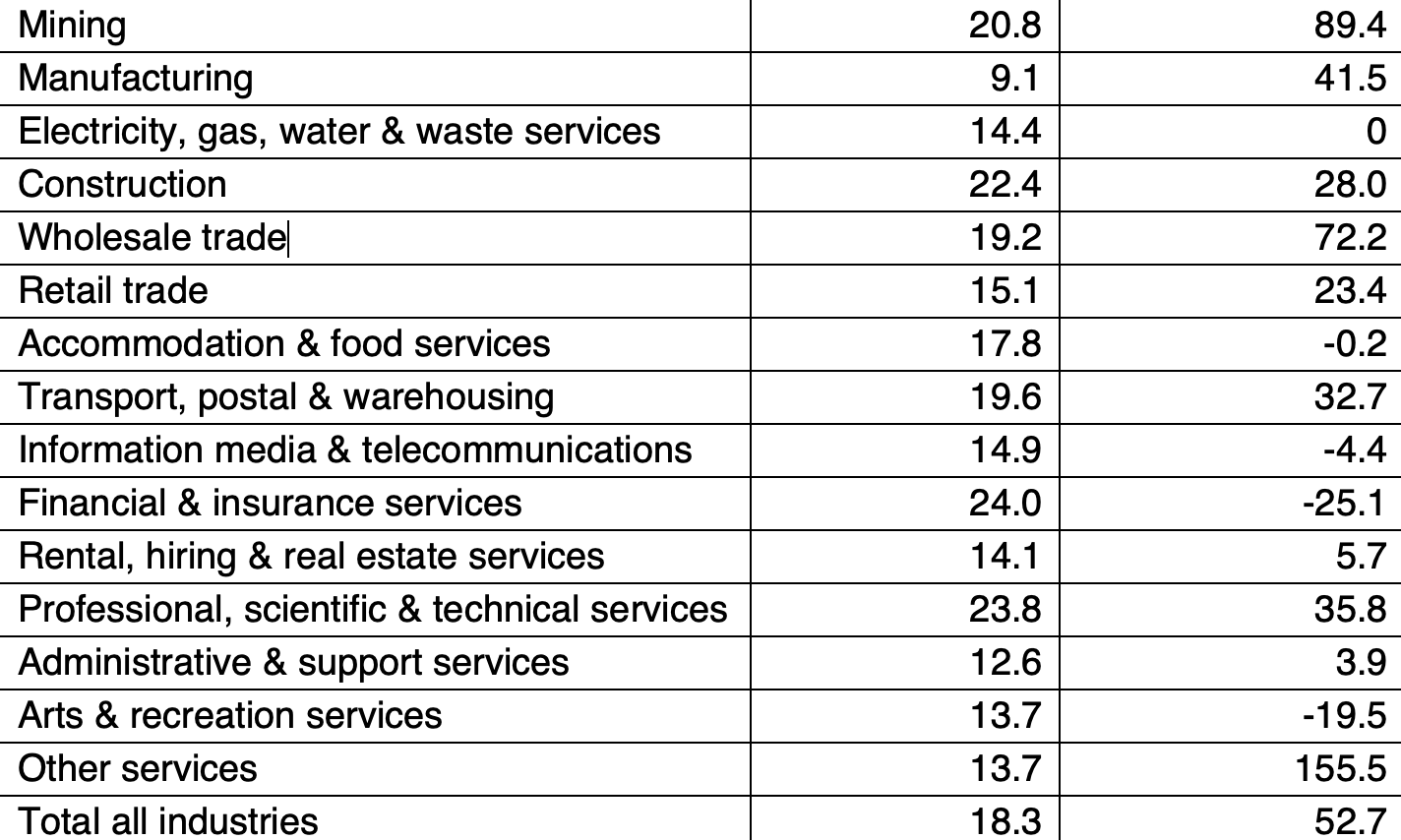

In Table 1 below, I show that while wages increased at much the same rate across all industries, the rate of increase in corporate profits varied widely between industries. In addition, the increase in corporate profits also varied significantly from one year to another. Thus, some industries that recorded a reduction in their profits in December 2022 compared to December 2019, nevertheless experienced an increase in 2021 compared to December 2019.

Table 1: Percentage Increase in wages and salaries and company gross operating profits by industry between December 2019 and December 2022

Source: ABS: Business Indicators, December 2022.

(Note: no profits data are available for agriculture, education, or health).

While the available data are not definitive, it seems highly likely that the increase in corporate profits has been driven by the international hike in commodity prices and other supply constraints impacting supply chains in manufacturing and wholesale trade. In particular, the increase in the profits in mining, no doubt reflecting the increase in international energy prices, meant that mining accounted for as much as 69.7 per cent of the total increase in corporate profits between December 2019 and December 2022.

In these circumstances, rather than relying on further interest rate increases to bring down inflation it would be better to rely on much more targeted measures. For example, the Government is on the right track in its insistence that energy producers must ensure adequate supplies for the Australian market at a reasonable price. The producers will still make a reasonable return, but these controls will limit the damage to the rest of the economy.

Other areas of the economy where companies have reported very big profit increases include, the retailers Coles and Woolworths, and the four big banks. In these cases, it seems likely that competition is not working as well as it should.

Research in the Treasury has found that employment has become more concentrated among a small number of large employers (like the major retailers and the banks), and the impact of this concentration may have lowered wages. But if this concentration can lower wages it can also increase profit margins.

Again, a more targeted approach to reducing inflation is called for. Instead of the RBA further increasing interest rates, it would be better to take action to improve competition.

Conclusion

After nine successive interest rate hikes, they may well now be achieving their objective of bringing inflation down. Therefore there should be a pause to better assess the effectiveness of this monetary tightening before deciding whether any more interest rate increases are necessary and how fast.

In addition, examination of the sources of the increase in inflation experienced indicates that more tightly targeted measures to reduce the excess profits in certain sectors would be more efficient than the blunt instrument of monetary policy.

Notes: Table 1 uses the ABS publication, Business Indicators, to compare the increase in seasonally adjusted wages and seasonally adjusted corporate gross operating surplus for most industries between December 2019 and December 2022.

Unfortunately, there are no data for agriculture, education, or health services. Also, no profits data are available before December quarter 2019, which means that it is not possible to compare the increase in profits for the whole of 2022 with the profits of each industry in 2019. As the profits data are very volatile, this means that the losses shown in Table 1 are especially misleading. In addition, in quite a few industries profits peaked in the second half of 2020 or sometime in 2021.

Another problem with Table 1 is that an increase in either wages or profits may reflect an increase in the volume of the relevant input. In the study by Jim Stanford, referred to in the main text above, the data were adjusted to remove any volume impacts on profits and wages, but here that was not possible. Unfortunately there is insufficient information to make similar estimates by industry.

Thus the Table 1 data are not directly comparable with the data in the Stanford study. Nevertheless, I am reasonably confident that these data do provide a useful indication of the industries where the profit rates increased most, even if the data do not allow an exact estimate of how much.

For more on this topic, P&I recommends: